Question: solve both no need to solve only one. if you will solve both then u will get thumbs pls do as soon as possible Question

solve both no need to solve only one. if you will solve both then u will get thumbs pls do as soon as possible

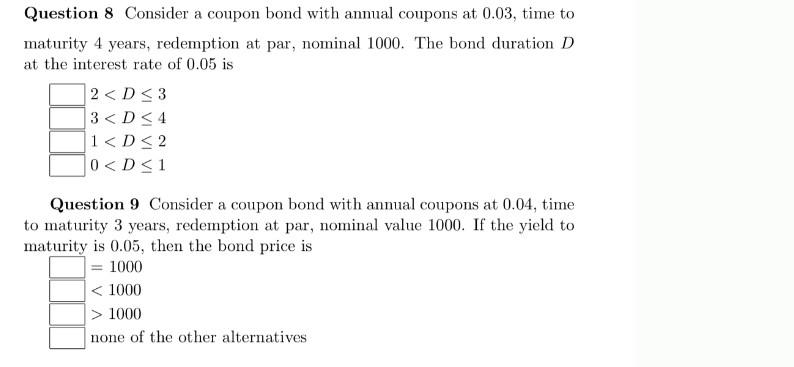

Question 8 Consider a coupon bond with annual coupons at 0.03, time to maturity 4 years, redemption at par, nominal 1000. The bond duration D at the interest rate of 0.05 is 2

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock