Question: SOLVE FOR PART B PLEASE Note: You can right-click the image then open in a new tab to better see the problem Exercise 7-3 Pearson

SOLVE FOR PART B PLEASE

Note: You can right-click the image then open in a new tab to better see the problem

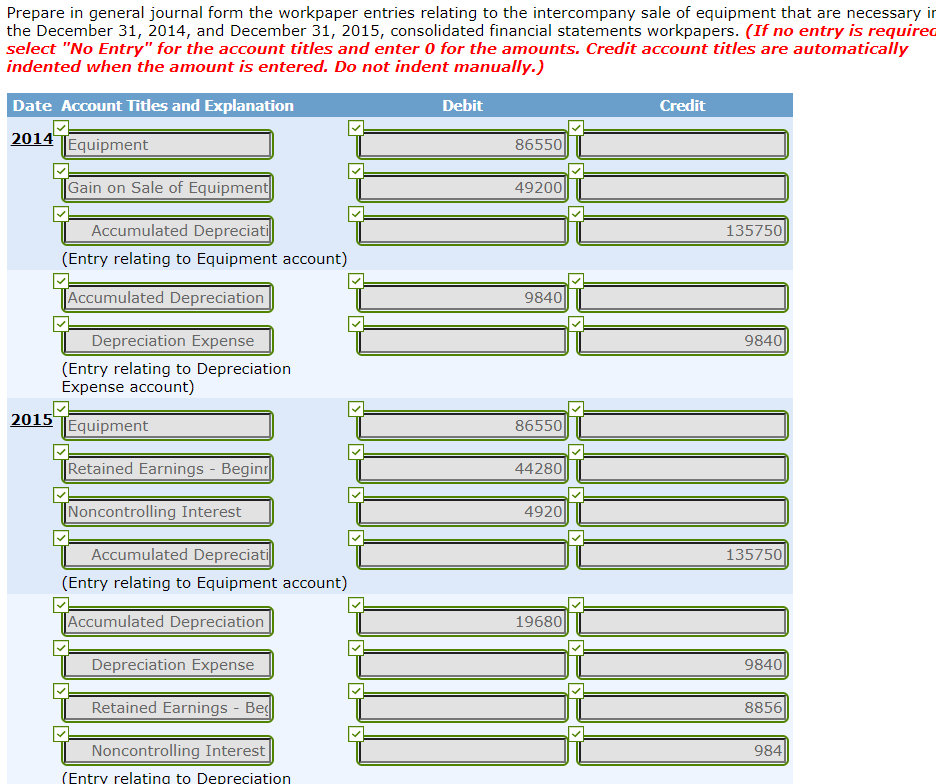

Exercise 7-3 Pearson Company owns 90% of the outstanding common stock of Spring Company. On January 1, 2014, Spring Company sold equipment to Pearson Company for $184,950. Spring Company had purchased the equipment for $271,500 on January 1, 2009, and had depreciated it using a 10% straight-line rate. The management of Pearson Company estimated that the equipment had a remaining useful life of five years on January 1, 2014. In 2015, Pearson Company reported $139,900 and Spring Company reported $105,000 in net income from their independent operations (including sales to affiliates). Prepare in general journal form the workpaper entries relating to the intercompany sale of equipment that are necessary in the December 31, 2014, and December 31, 2015, consolidated financial statements workpapers. (If no entry is required select "No Entry" for the account titles and enter 0 for the amounts. Credit account titles are automatically indented when the amount is entered. Do not indent manually.) Date Account Titles and Explanation Debit Credit 2014 TEquipment 86550 Gain on Sale of Equipment 49200 135750 Accumulated Depreciati (Entry relating to Equipment account) Accumulated Depreciation 9840 9840 Depreciation Expense (Entry relating to Depreciation Expense account) 2015 Equipment 86550 Retained Earnings - Beginr 442801 Noncontrolling Interest 4920 135750 Accumulated Depreciati (Entry relating to Equipment account) Accumulated Depreciation 19680 Depreciation Expense 9840 Retained Earnings - Beg 8856 984 Noncontrolling Interest (Entry relating to Depreciation (b) Calculate controlling interest in consolidated income for 2015. 2015 Controlling Interest in Consolidated Net Income $

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts