Question: Some information is provided below about five different investment funds, each investing in a different portfolio of assets. The funds are based in the United

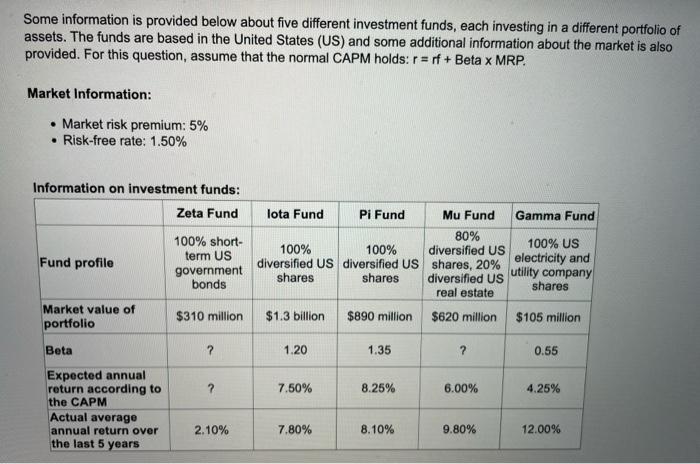

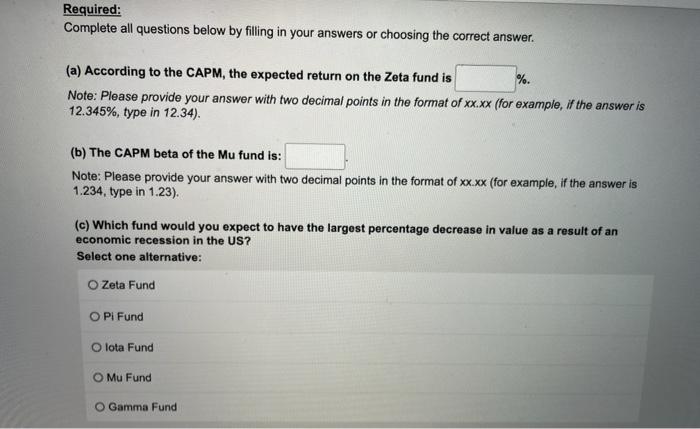

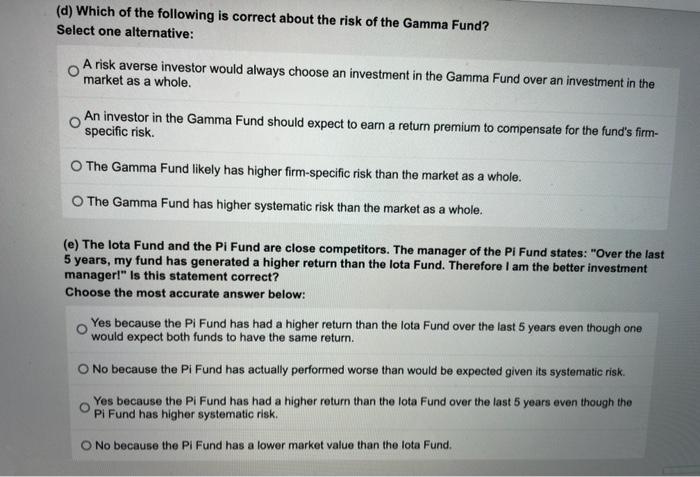

Some information is provided below about five different investment funds, each investing in a different portfolio of assets. The funds are based in the United States (US) and some additional information about the market is also provided. For this question, assume that the normal CAPM holds: r = rf + Beta x MRP. Market Information: Market risk premium: 5% Risk-free rate: 1.50% Information on investment funds: Zeta Fund Fund profile 100% short- term US government bonds lota Fund Pi Fund Mu Fund Gamma Fund 80% 100% 100% diversified US 100% US diversified US diversified US shares, 20% electricity and shares shares diversified us utility company shares real estate $1.3 billion $890 million $620 million $105 million Market value of portfolio $310 million Beta ? 1.20 1.35 ? 0.55 ? 7.50% 8.25% 6.00% 4.25% Expected annual return according to the CAPM Actual average annual return over the last 5 years 2.10% 7.80% 8.10% 9.80% 12.00% Required: Complete all questions below by filling in your answers or choosing the correct answer. (a) According to the CAPM, the expected return on the Zeta fund is %. Note: Please provide your answer with two decimal points in the format of xx.xx (for example, if the answer is 12.345%, type in 12.34). (b) The CAPM beta of the Mu fund is: Note: Please provide your answer with two decimal points in the format of xx.xx (for example, if the answer is 1.234, type in 1.23). an (c) Which fund would you expect to have the largest percentage decrease in value as a result economic recession in the US? Select one alternative: Zeta Fund OPI Fund Olota Fund O Mu Fund O Gamma Fund (d) Which of the following is correct about the risk of the Gamma Fund? Select one alternative: A risk averse investor would always choose an investment in the Gamma Fund over an investment in the market as a whole. An investor in the Gamma Fund should expect to earn a return premium to compensate for the fund's firm- specific risk. The Gamma Fund likely has higher firm-specific risk than the market as a whole. The Gamma Fund has higher systematic risk than the market as a whole. (e) The lota Fund and the Pi Fund are close competitors. The manager of the PI Fund states: "Over the last 5 years, my fund has generated a higher return than the lota Fund. Therefore I am the better investment manager!" Is this statement correct? Choose the most accurate answer below: Yes because the Pi Fund has had a higher return than the lota Fund over the last 5 years even though one would expect both funds to have the same return. No because the Pi Fund has actually performed worse than would be expected given its systematic risk. Yes because the PI Fund has had a higher return than the lota Fund over the last 5 years even though the Pi Fund has higher systematic risk. O No because the Pi Fund has a lower market value than the lota Fund

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts