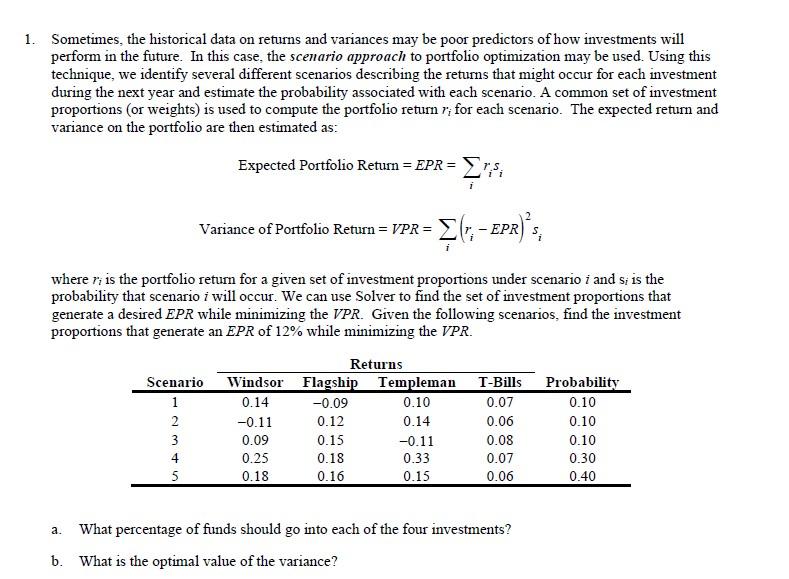

Question: Sometimes, the historical data on returns and variances may be poor predictors of how investments will perform in the future. In this case, the scenario

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock