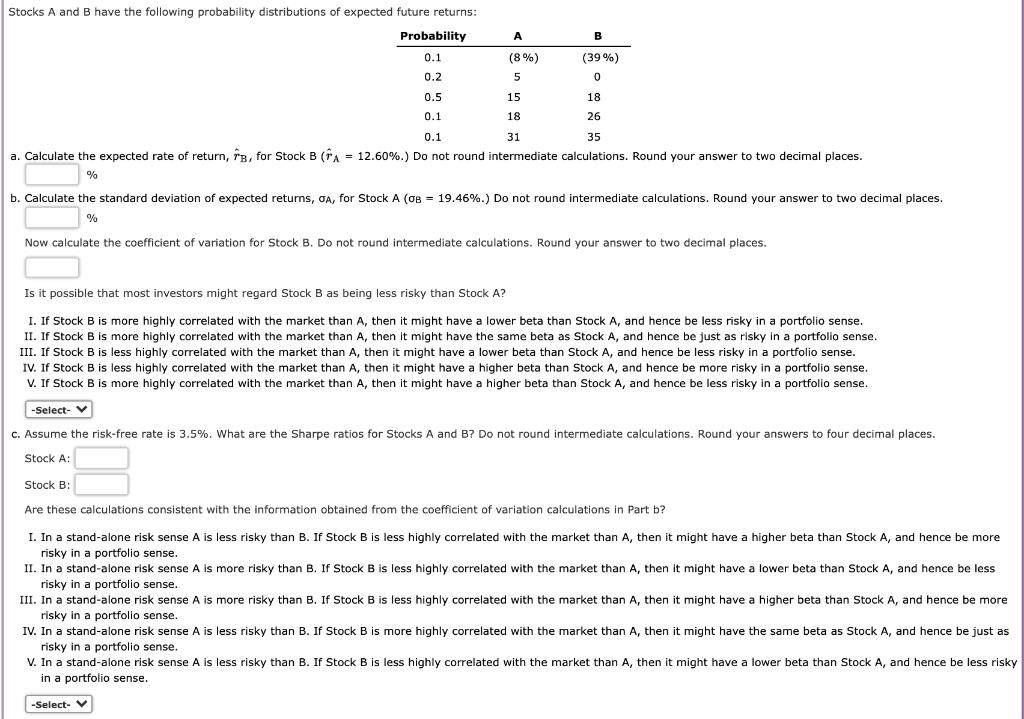

Stocks A and B have the following probability distributions of expected future returns: Probability A B...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Stock Risk and Return Analysis a Expected Return for Stock B B Return Probability Return Probability 26 01 26 35 02 70 Weighted Average 10 B Return Pr... View the full answer

Related Book For

Fundamentals of Financial Management

ISBN: 978-1337395250

15th edition

Authors: Eugene F. Brigham, Joel F. Houston

Posted Date: