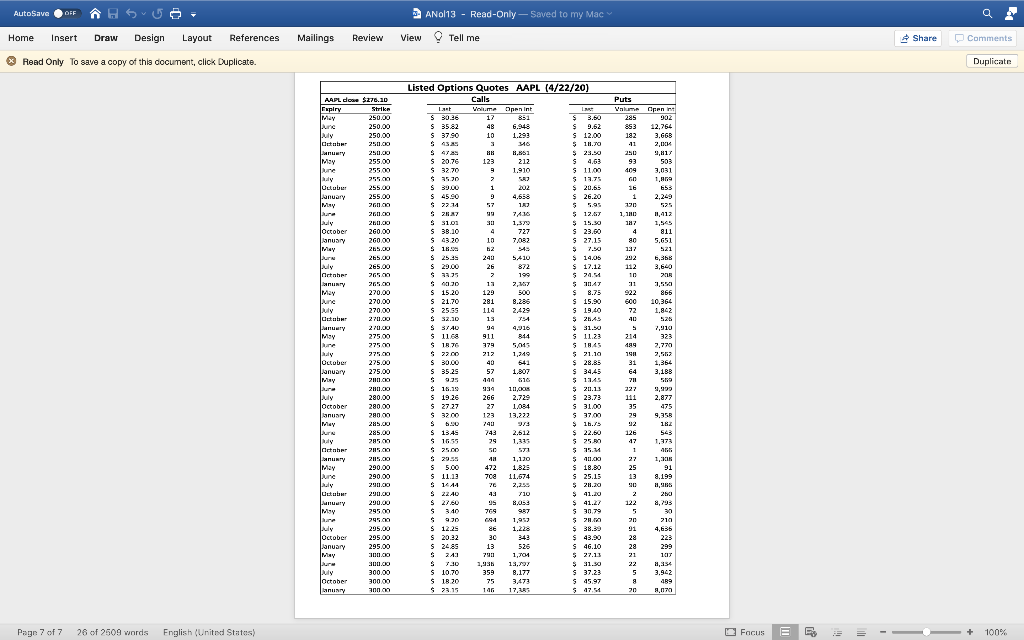

Question: Suppose in April we construct a vertical bull spread on AAPL calls, by writing 10 October 280 contracts and buying 10 October 270 contracts. Solve

-

Suppose in April we construct a vertical bull spread on AAPL calls, by writing 10 October 280 contracts and buying 10 October 270 contracts.

Suppose in April we construct a vertical bull spread on AAPL calls, by writing 10 October 280 contracts and buying 10 October 270 contracts. - Solve for the investors profit for the following AAPL stock prices at expiration: $242.00, $258.00, $274.00, $290.00, $306.00.

- At what price on AAPL shares does the investor break even?

- The same spread on puts may be a more profitable strategy. Answer questions a) and b) again assuming we use October puts.

- Which strategy would you prefer and why?

* AutoSave A Svo ANO 13 - Read-Only - Saved to my Mac Home Insert Draw Design Layout References Mailings Review View Tell me Read Only To save a copy of this document, click Duplicate. Listed Options Quotes AAPL (4/22/20) APL do $270.00 Duplicate Puts SES ESS 0. 18 .. Paar 7 of 7 26 of 2509 words English (United States) P

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock