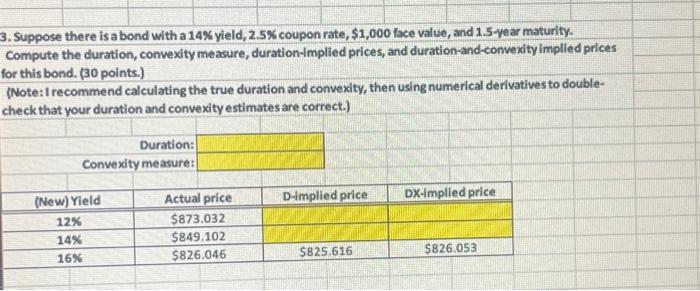

Question: . Suppose there is a bond with a 14% yield, 2.5% coupon rate, $1,000 face value, and 1.5 year maturity. Compute the duration, convexity measure,

. Suppose there is a bond with a 14% yield, 2.5% coupon rate, $1,000 face value, and 1.5 year maturity. Compute the duration, convexity measure, duration-implied prices, and duration-and-convexity implied prices or this bond. (30 points.) (Note: I recommend calculating the true duration and convexity, then using numerical derivatives to doublecheck that your duration and convexity estimates are correct.)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock