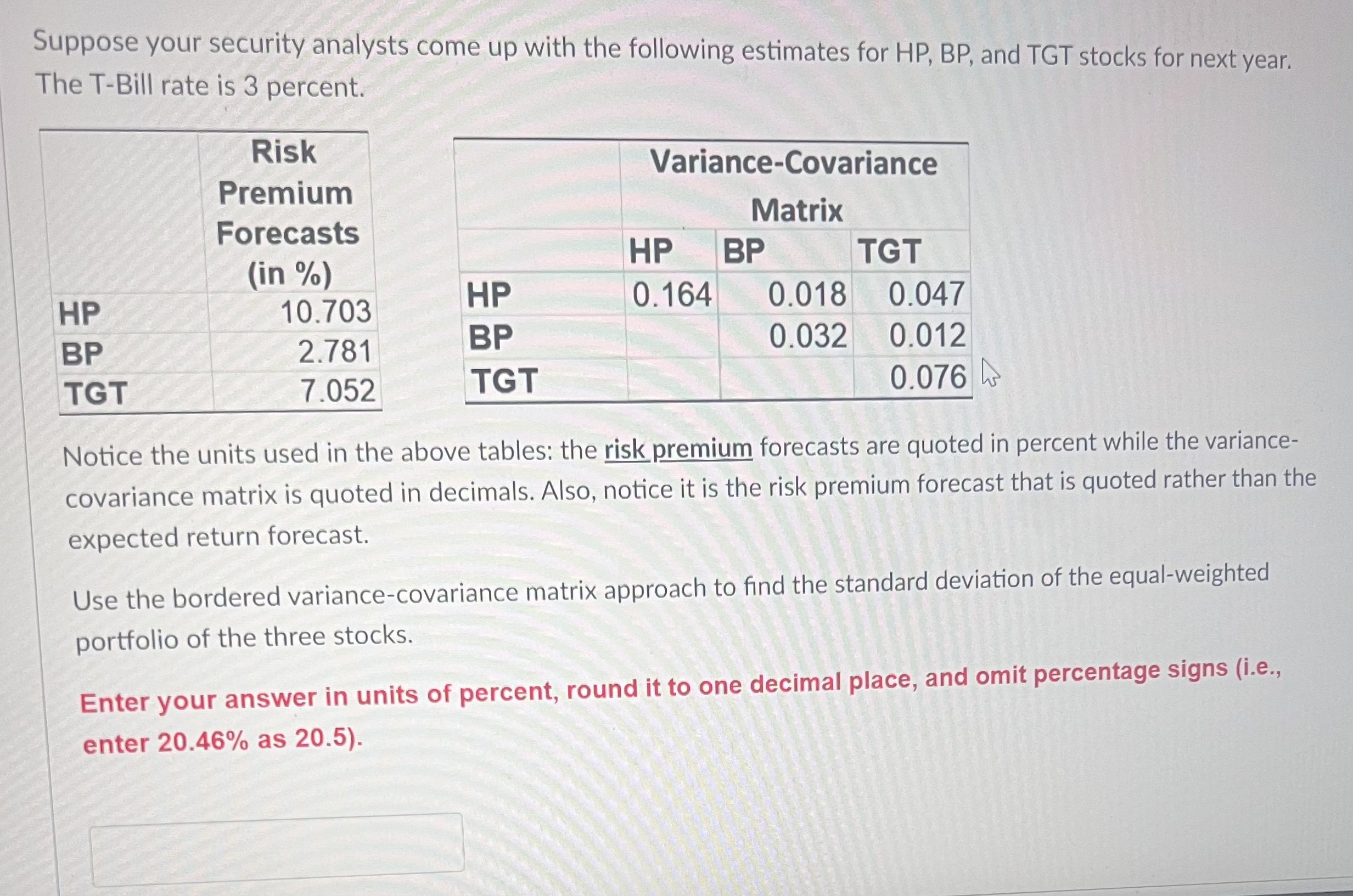

Question: Suppose your security analysts come up with the following estimates for HP, BP, and TGT stocks for next year. The T-Bill rate is 3 percent.

Suppose your security analysts come up with the following estimates for HP, BP, and TGT stocks for next year. The T-Bill rate is 3 percent. Notice the units used in the above tables: the risk premium forecasts are quoted in percent while the variancecovariance matrix is quoted in decimals. Also, notice it is the risk premium forecast that is quoted rather than the expected return forecast. Use the bordered variance-covariance matrix approach to find the standard deviation of the equal-weighted portfolio of the three stocks. Enter your answer in units of percent, round it to one decimal place, and omit percentage signs (i.e., enter 20.46% as 20.5 )

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts