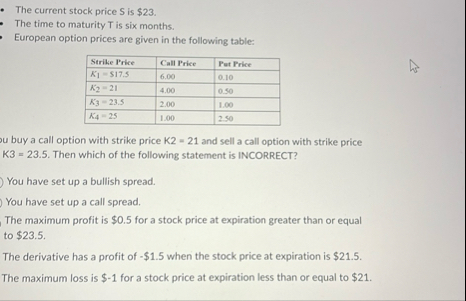

Question: The current stock price S is $ 2 3 . The time to maturity T is six months. European option prices are given in the

The current stock price S is $

The time to maturity T is six months.

European option prices are given in the following table:

tableStrike Price,Call Price,Put Price$

u buy a call option with strike price and sell a call option with strike price Then which of the following statement is INCORRECT?

You have set up a bullish spread.

You have set up a call spread.

The maximum profit is $ for a stock price at expiration greater than or equal to $

The derivative has a profit of $ when the stock price at expiration is $

The maximum loss is $ for a stock price at expiration less than or equal to $

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock