The file OIL.GDP.xls contains annual time series data for country Z in Africa. The variables in this

Question:

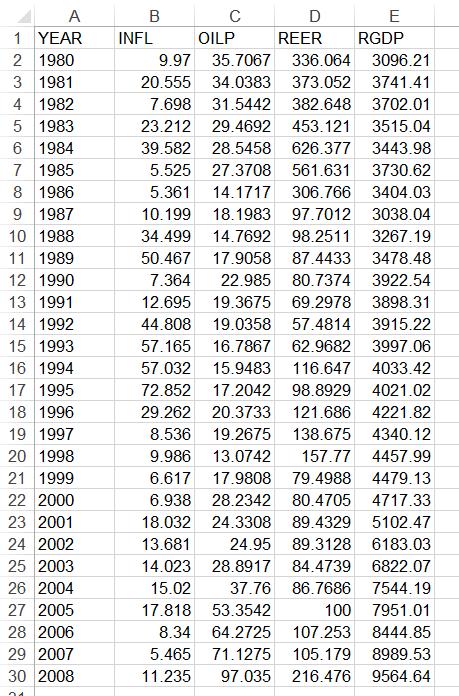

The file OIL.GDP.xls contains annual time series data for country Z in Africa. The variables in this data set are: Inflation (INFL) measured as a percentage, oil price (OILP) measured in dollars per barrel, percapita GDP (RGDP), measured in US dollars, and the real effective exchange rate (REER), measured as an index (increases by a unit). As an oil analyst, you suggest that the only way to study the impact of crude oil prices on macroeconomic activity in country Z is to regress the log of RGDP on a constant, log of OILP, log of INFL and log of REER.

(a) Estimate the above relationship using ordinary least squares and write the fitted regression equation.

(b) Interpret the estimated coefficients excluding the constant.

(c) Interpret the R-squared value of the model and briefly comment on the significance of each independent variable.

(d) Conduct and interpret the Durbin Watson test for autocorrelation. Alpha is given as 0.05.

(e) Test for the presence of heteroskedasticity in the model estimated in part (a). State the null and alternative hypotheses.

(f) What are the consequences of heteroskedasticity if it exists in a regression model?

(g) Conduct the general F-test on the model coefficients in part (c) using α = 5%

h) Using economic theory and the estimated model results in part (a), state whether country Z is a net importer or exporter of crude oil. Give evidence to support your answer.

I) If above estimation in part (a) has parameters instability then please rectify this problem and estimate the correct regression and note down the values involved for each of the classical assumptions and other tests.

Expert Answer:

a To estimate the relationship using ordinary least squares we regress the log of RGDP on a constant log of OILP log of INFL and log of REER Let Y be the log of RGDP 1X1 be the log of OILP 2X2 be the ... View the full answer

Data Analysis and Decision Making

ISBN: 978-0538476126

4th edition

Authors: Christian Albright, Wayne Winston, Christopher Zappe