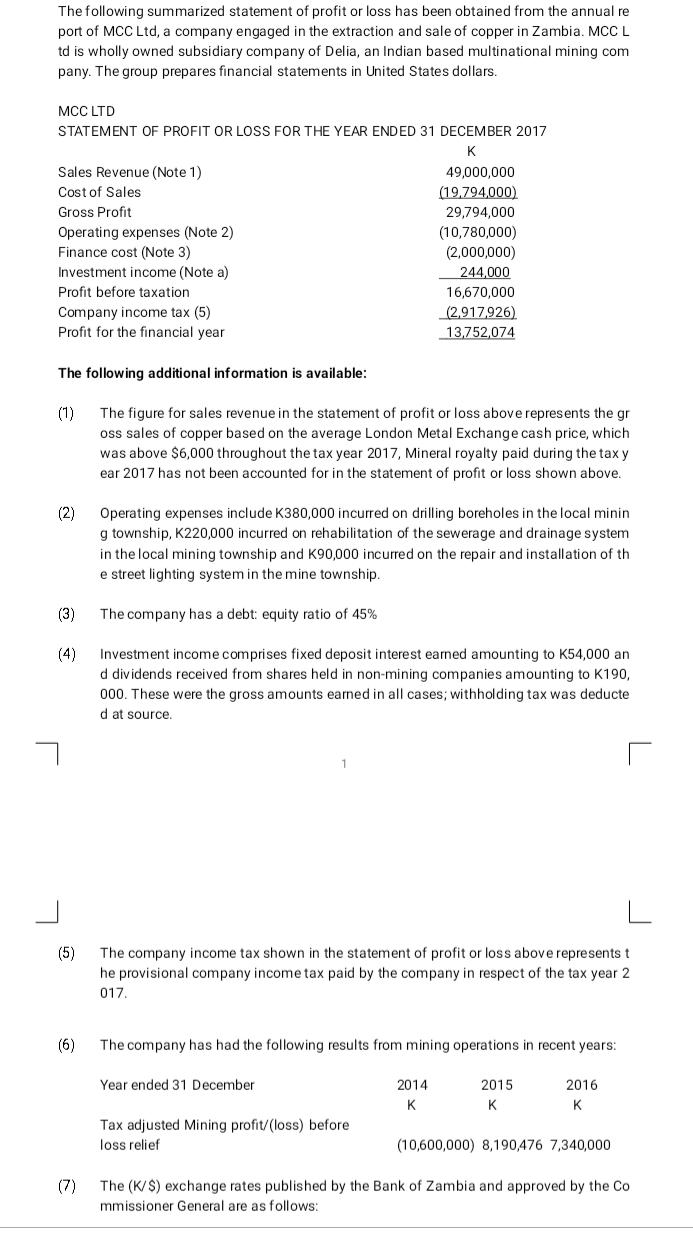

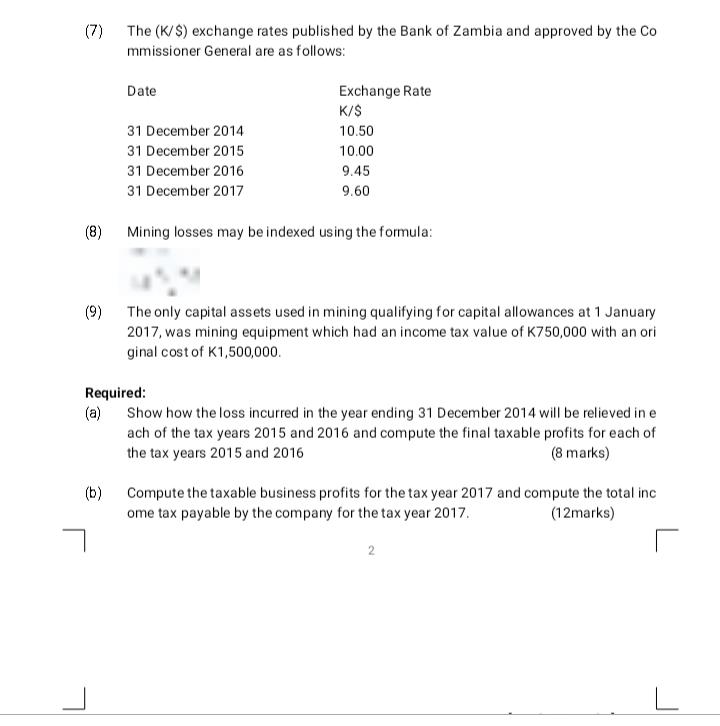

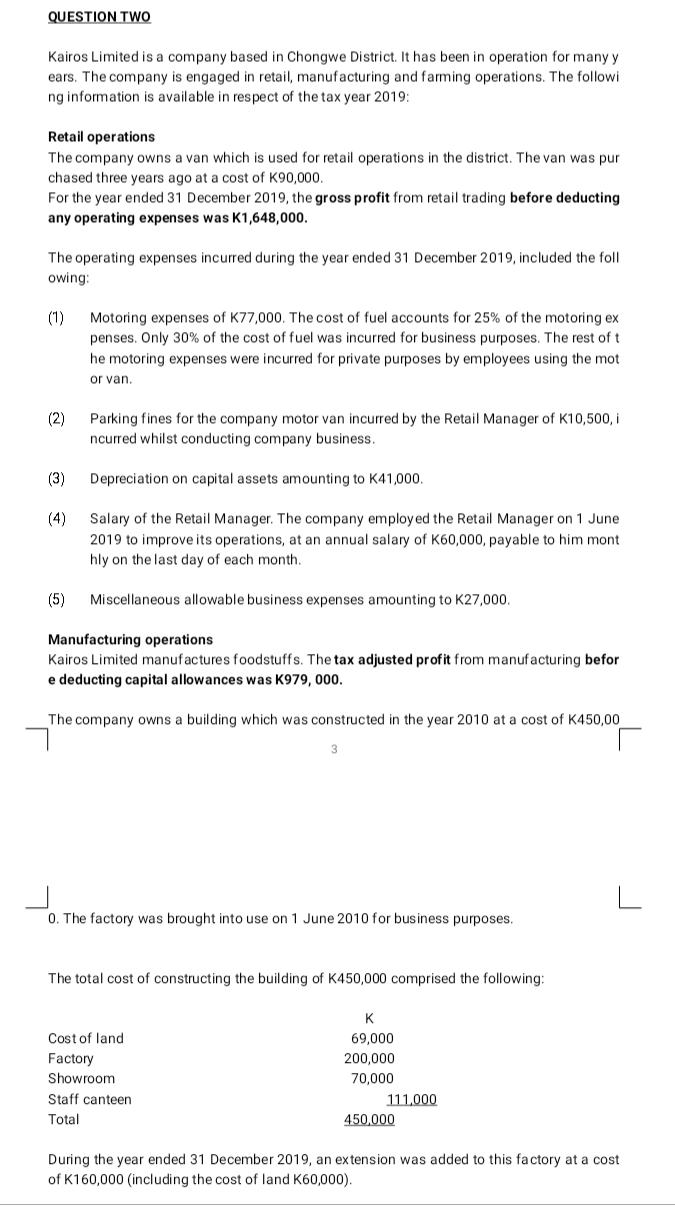

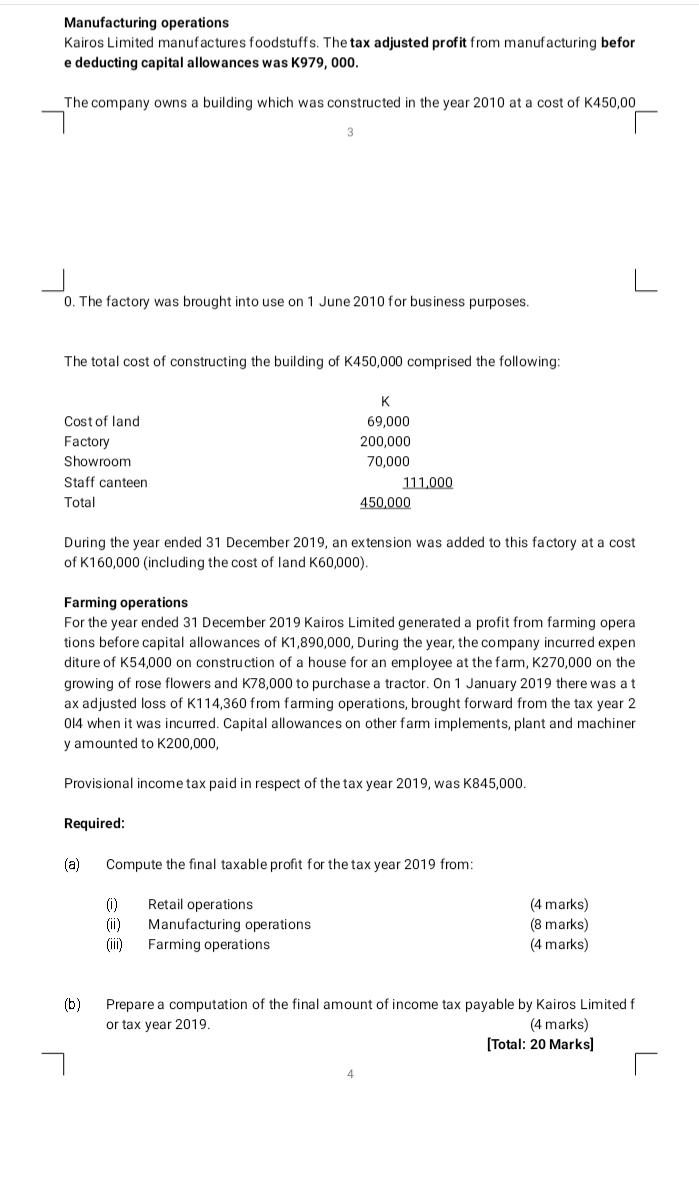

The following summarized statement of profit or loss has been obtained from the annual re port...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

The following summarized statement of profit or loss has been obtained from the annual re port of MCC Ltd, a company engaged in the extraction and sale of copper in Zambia. MCC L td is wholly owned subsidiary company of Delia, an Indian based multinational mining com pany. The group prepares financial statements in United States dollars. MCC LTD STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED 31 DECEMBER 2017 K Sales Revenue (Note 1) Cost of Sales Gross Profit Operating expenses (Note 2) Finance cost (Note 3) Investment income (Note a) Profit before taxation (1) (2) Company income tax (5) Profit for the financial year The following additional information is available: The figure for sales revenue in the statement of profit or loss above represents the gr oss sales of copper based on the average London Metal Exchange cash price, which. was above $6,000 throughout the tax year 2017, Mineral royalty paid during the tax y ear 2017 has not been accounted for in the statement of profit or loss shown above. (3) (4) (5) (6) (7) The company has a debt: equity ratio of 45% Operating expenses include K380,000 incurred on drilling boreholes in the local minin g township, K220,000 incurred on rehabilitation of the sewerage and drainage system in the local mining township and K90,000 incurred on the repair and installation of th e street lighting system in the mine township. 49,000,000 (19,794,000) 29,794,000 1 (10,780,000) (2,000,000) 244,000 Investment income comprises fixed deposit interest earned amounting to K54,000 an d dividends received from shares held in non-mining companies amounting to K190, 000. These were the gross amounts earned in all cases; withholding tax was deducte d at source. Year ended 31 December 16,670,000 (2,917,926) 13,752,074 The company income tax shown in the statement of profit or loss above represents t he provisional company income tax paid by the company in respect of the tax year 2 017. The company has had the following results from mining operations in recent years: 2015 K 2014 K Tax adjusted Mining profit/(loss) before. loss relief 2016 K (10,600,000) 8,190,476 7,340,000 The (K/S) exchange rates published by the Bank of Zambia and approved by the Co. mmissioner General are as follows: (7) (8) The (K/$) exchange rates published by the Bank of Zambia and approved by the Co mmissioner General are as follows: Date (b) Exchange Rate K/$ 10.50 31 December 2014 31 December 2015 31 December 2016 31 December 2017 Mining losses may be indexed using the formula: 10.00 9.45 9.60 (9) The only capital assets used in mining qualifying for capital allowances at 1 January 2017, was mining equipment which had an income tax value of K750,000 with an ori ginal cost of K1,500,000. Required: (a) Show how the loss incurred in the year ending 31 December 2014 will be relieved in e ach of the tax years 2015 and 2016 and compute the final taxable profits for each of the tax years 2015 and 2016 (8 marks) Compute the taxable business profits for the tax year 2017 and compute the total inc ome tax payable by the company for the tax year 2017. (12marks) 2 QUESTION TWO Kairos Limited is a company based in Chongwe District. It has been in operation for many y ears. The company is engaged in retail, manufacturing and farming operations. The followi ng information is available in respect of the tax year 2019: Retail operations The company owns a van which is used for retail operations in the district. The van was pur chased three years ago at a cost of K90,000. For the year ended 31 December 2019, the gross profit from retail trading before deducting any operating expenses was K1,648,000. The operating expenses incurred during the year ended 31 December 2019, included the foll owing: (1) (2) (3) Motoring expenses of K77,000. The cost of fuel accounts for 25% of the motoring ex penses. Only 30% of the cost of fuel was incurred for business purposes. The rest of t he motoring expenses were incurred for private purposes by employees using the mot or van. Parking fines for the company motor van incurred by the Retail Manager of K10,500, i ncurred whilst conducting company business. Depreciation on capital assets amounting to K41,000. Salary of the Retail Manager. The company employed the Retail Manager on 1 June 2019 to improve its operations, at an annual salary of K60,000, payable to him mont hly on the last day of each month.. (5) Miscellaneous allowable business expenses amounting to K27,000. Manufacturing operations Kairos Limited manufactures foodstuffs. The tax adjusted profit from manufacturing befor e deducting capital allowances was K979, 000. The company owns a building which was constructed in the year 2010 at a cost of K450,00 0. The factory was brought into use on 1 June 2010 for business purposes. The total cost of constructing the building of K450,000 comprised the following: Cost of land Factory Showroom. Staff canteen Total K 69,000 200,000 70,000 111,000 450,000 During the year ended 31 December 2019, an extension was added to this factory at a cost of K160,000 (including the cost of land K60,000). Manufacturing operations Kairos Limited manufactures foodstuffs. The tax adjusted profit from manufacturing befor e deducting capital allowances was K979, 000. The company owns a building which was constructed in the year 2010 at a cost of K450,00 0. The factory was brought into use on 1 June 2010 for business purposes. The total cost of constructing the building of K450,000 comprised the following: Cost of land Factory Showroom Staff canteen Total During the year ended 31 December 2019, an extension was added to this factory at a cost of K160,000 (including the cost of land K60,000). Required: Farming operations. For the year ended 31 December 2019 Kairos Limited generated a profit from farming opera tions before capital allowances of K1,890,000, During the year, the company incurred expen diture of K54,000 on construction of a house for an employee at the farm, K270,000 on the growing of rose flowers and K78,000 to purchase a tractor. On 1 January 2019 there was at ax adjusted loss of K114,360 from farming operations, brought forward from the tax year 2 014 when it was incurred. Capital allowances on other farm implements, plant and machiner y amounted to K200,000, (a) K 69,000 200,000 70,000 Provisional income tax paid in respect of the tax year 2019, was K845,000. (b) 111,000 450,000 (0) (ii) (III) Compute the final taxable profit for the tax year 2019 from: Retail operations Manufacturing operations Farming operations 4 (4 marks) (8 marks) (4 marks) Prepare a computation of the final amount of income tax payable by Kairos Limited f or tax year 2019. (4 marks) [Total: 20 Marks] QUESTION THREE You are employed in a firm of Chartered Accountants. Your firm is dealing with the tax affair s of Matimba Ltd, a VAT registered trading company. You are helping the company in prepar ing the VAT return for the month of May 2019. The directors have heard that a business can account for VAT using the Cash Accounting Scheme and are keen to know Whether Matimb a Ltd can register to account for VAT under the cash accounting scheme. You have been provided with the following information relating to the month of May 2019. (1) Sales invoices totaling K2,750,000 were issued to customers out of which exempt sal es were K550,000 and zero rated sales were K320,000 with the remainder of the sales being standard rated. (2) (3) (4) (5) (6) (7) Out of the standard rated sales, goods with a value of K350,000 were sold on sale or return basis. These goods were dispatched to the customer on 30 May 2019, however the customer only paid for the goods on 2 June 2019, although he adopted the sale when he received goods. Total Sales returns for the month were K280,000 comprising returns on standard rate d sales of K170,000, returns on exempt sales of K30,000 and returns on zero rated sa les of K80,000. The company received an advance deposit of K85,000 in respect of a standard rated contract that is due for completion in July 2019. The contract has a total value of K1 50,000. Standard rated purchases were K980,000 and the purchase returns on these purchas e amounted to K83,000. Standard rated expenses amounted to K179,800 (VAT inclusive) broken down as follows: Entertaining customers Staff meals and refreshments Petrol for company cars Diesel for motor vans Telephone bills 5 Pool motor car Delivery van Air conditioners K 34,800 37,120 40,600 20,880 179,800 The company wrote off a bad debt amounting to K26,000 during the month of May 2 019, in respect of a debt which was due for payment on 31 October 2018. The company bought the following capital assets at the following VAT inclusive cost S: K 174,000 139,200 69,600 8. 9. 10. On 1 January 2020, SMC Plc held the following assets qualifying for capital allowan ces. All of the assets were acquired locally from Zambian suppliers: Old mining equipment Haulage Trucks Toyota Fortuner (3000cc) Toyota Prado car (2600cc) Bought office building at Sold old mining equipment for Bought new mining equipment Income Tax Value: at 1 January 2020 K 480,000 2,360,000 240,000 270,000 During the year ended 31 December 2020, the company entered into the following cal pital transactions: 8 13.80 14.40 Cost/(proceeds) K 5,000,000 (780,000) 4,000,000 Original Cost The Toyota Fortuner car and Toyota Prado car are used by the Chief Executive Officer The following are the Bank of Zambia average mid-rates: Year ZMW/US$1 2019 2020 K 2,400,000 4,720,000 600,000 450,000 and Operations Director respectively on personal-to-holder basis. The private usage in the motor cars is estimated to be 45% by each individual. The following indexation formula may be used where applicable: Required: (a) Compute the taxable mining profits for SMC plc for the year 2020. (16 marks) (b) Calculate the amount of company income tax payable by SMC Plc for the tax ye ar 2020. (4 marks) [Total: 20 Marks] QUESTION FIVE You are employed in the Tax department of a firm of Chartered Accountants. The tax manag er has presented you with the following information that has been extracted from the files o f the following clients of your firm: Brian Ntebeka Ntebeka, a sole trader, imported a second-hand panel van with a gross vehicle weight (GVW) of 2.5 tonnes, for exclusive use in his business in February 2020. The van was manufacture d in Japan in January 2010. The cost of the van was $3,700 (free on board). He incurred ins urance costs of $400, transportation costs of $900 in transit up to the port of Dar es salaam where clearing and forwarding costs of $200 were incurred. He incurred further incidental co sts of transporting the vehicle from Nakonde border post to Kapiri Mposhi amounting to $1, 200. In Kapiri vehicle registration fees were K1500, whilst motor car insurance costs were K 3,500. The exchange rate provided by the Commissioner General at the time of importation of the v ehicle was K14.50 per US$; however the exchange rates quoted in a local Bureau De Change was K14.80 Per US$ Cactus Ltd Cactus Ltd, is a VAT registered company making zero rated, standard rated and exempt sup plies. During the month of February 2020, the company made zero rated sales ofK630,000 which represented 15% of the total sales made in the month, standard rated sales represent ed 65% of the total sales made in the month and the remainder of the sales were exempt su pplies. The following expenditure was incurred during the month of February 2020: · Total purchases were K2,088,000 comprising standard rated purchases of K1,670,40 0 (VAT inclusive) and exempt purchases of K417,600. • Purchase of office furniture at a cost of K40,600 (VA inclusive) · Purchase of a pool car for K150,800 (VAT inclusive) 9 Other Information: • Purchase of a personal to holder motor car (with 50% private use by the Managing Di rector) at a cost of K162,400 (VAT inclusive) • Overheads of K165,418 (VAT inclusive). These comprised petrol for the personal to h older motor car of K18,560, petrol for pool cars of K20,880, diesel for the company's v ehicles of K34,800, entertainment expenses for employees of K5,338, electricity bills f or the managing director's accommodation of K4,640 and other general business ove rheads of K81,200. (1) The input VAT on the overheads cannot be attributed directly to neither taxable nor ex empt supplies. (2) Unless stated otherwise all of the above figures are exclusive of VAT. Required: (a) (b) Calculate the customs value of the panel van and the total import taxes paid by Nteb eka on the importation of the van. (8 marks) Compute the value added tax payable by Cactus Ltd for the month of February 2020. (1) (2) The input VAT on the overheads cannot be attributed directly to neither taxable nor ex empt supplies. Unless stated otherwise all of the above figures are exclusive of VAT. Required: (a) (b) Calculate the customs value of the panel van and the total import taxes paid by Nteb eka on the importation of the van. (8 marks) Compute the value added tax payable by Cactus Ltd for the month of February 2020. You should clearly indicate in your computation, by the use of a Zero (0), any items o n which VAT is not chargeable or not recoverable. (12 marks) [Totals: 20 Marks] 10 QUESTION SIX MNC Mining Corporation is a mining company operating an underground mine in Zambia. The company is engaged in the extraction of copper. The company made the following expo rts of copper in the following months of the charge year 2019: March 2019 June 2019 October 2019 December 2019 The Zambian kwacha per US$1 exchange rate approved by the Commissioner General from January 2019 to 31 December 2019 should be taken to be K11.50/ US$1. The average London Metal Exchange (LME) cash prices per metric tonne were as follows: US$6,300 March June October December (1) (1) (iii) US$5,900 US$7,600 US$4,400 Required: (a) Explain the meaning of the following terms in the context of the taxation of mining oper ations: 700 tonnes of Copper 1,000 tonnes of Copper 1,200 tonnes of Copper 500 tonnes of Copper Norm value Gross value Mineral Royalty (0) (ii) (b) Calculate the mineral royalty tax paid by the company, for each export, stating the due d ate for each payment. (8 marks) (c) Explain the consequences of the following: Paying mineral royalty late. (3 marks) (2 marks) (3 marks) Submitting the mineral royalty tax return late. (2 marks) (2 marks) [Total 20 Marks] The following summarized statement of profit or loss has been obtained from the annual re port of MCC Ltd, a company engaged in the extraction and sale of copper in Zambia. MCC L td is wholly owned subsidiary company of Delia, an Indian based multinational mining com pany. The group prepares financial statements in United States dollars. MCC LTD STATEMENT OF PROFIT OR LOSS FOR THE YEAR ENDED 31 DECEMBER 2017 K Sales Revenue (Note 1) Cost of Sales Gross Profit Operating expenses (Note 2) Finance cost (Note 3) Investment income (Note a) Profit before taxation (1) (2) Company income tax (5) Profit for the financial year The following additional information is available: The figure for sales revenue in the statement of profit or loss above represents the gr oss sales of copper based on the average London Metal Exchange cash price, which. was above $6,000 throughout the tax year 2017, Mineral royalty paid during the tax y ear 2017 has not been accounted for in the statement of profit or loss shown above. (3) (4) (5) (6) (7) The company has a debt: equity ratio of 45% Operating expenses include K380,000 incurred on drilling boreholes in the local minin g township, K220,000 incurred on rehabilitation of the sewerage and drainage system in the local mining township and K90,000 incurred on the repair and installation of th e street lighting system in the mine township. 49,000,000 (19,794,000) 29,794,000 1 (10,780,000) (2,000,000) 244,000 Investment income comprises fixed deposit interest earned amounting to K54,000 an d dividends received from shares held in non-mining companies amounting to K190, 000. These were the gross amounts earned in all cases; withholding tax was deducte d at source. Year ended 31 December 16,670,000 (2,917,926) 13,752,074 The company income tax shown in the statement of profit or loss above represents t he provisional company income tax paid by the company in respect of the tax year 2 017. The company has had the following results from mining operations in recent years: 2015 K 2014 K Tax adjusted Mining profit/(loss) before. loss relief 2016 K (10,600,000) 8,190,476 7,340,000 The (K/S) exchange rates published by the Bank of Zambia and approved by the Co. mmissioner General are as follows: (7) (8) The (K/$) exchange rates published by the Bank of Zambia and approved by the Co mmissioner General are as follows: Date (b) Exchange Rate K/$ 10.50 31 December 2014 31 December 2015 31 December 2016 31 December 2017 Mining losses may be indexed using the formula: 10.00 9.45 9.60 (9) The only capital assets used in mining qualifying for capital allowances at 1 January 2017, was mining equipment which had an income tax value of K750,000 with an ori ginal cost of K1,500,000. Required: (a) Show how the loss incurred in the year ending 31 December 2014 will be relieved in e ach of the tax years 2015 and 2016 and compute the final taxable profits for each of the tax years 2015 and 2016 (8 marks) Compute the taxable business profits for the tax year 2017 and compute the total inc ome tax payable by the company for the tax year 2017. (12marks) 2 QUESTION TWO Kairos Limited is a company based in Chongwe District. It has been in operation for many y ears. The company is engaged in retail, manufacturing and farming operations. The followi ng information is available in respect of the tax year 2019: Retail operations The company owns a van which is used for retail operations in the district. The van was pur chased three years ago at a cost of K90,000. For the year ended 31 December 2019, the gross profit from retail trading before deducting any operating expenses was K1,648,000. The operating expenses incurred during the year ended 31 December 2019, included the foll owing: (1) (2) (3) Motoring expenses of K77,000. The cost of fuel accounts for 25% of the motoring ex penses. Only 30% of the cost of fuel was incurred for business purposes. The rest of t he motoring expenses were incurred for private purposes by employees using the mot or van. Parking fines for the company motor van incurred by the Retail Manager of K10,500, i ncurred whilst conducting company business. Depreciation on capital assets amounting to K41,000. Salary of the Retail Manager. The company employed the Retail Manager on 1 June 2019 to improve its operations, at an annual salary of K60,000, payable to him mont hly on the last day of each month.. (5) Miscellaneous allowable business expenses amounting to K27,000. Manufacturing operations Kairos Limited manufactures foodstuffs. The tax adjusted profit from manufacturing befor e deducting capital allowances was K979, 000. The company owns a building which was constructed in the year 2010 at a cost of K450,00 0. The factory was brought into use on 1 June 2010 for business purposes. The total cost of constructing the building of K450,000 comprised the following: Cost of land Factory Showroom. Staff canteen Total K 69,000 200,000 70,000 111,000 450,000 During the year ended 31 December 2019, an extension was added to this factory at a cost of K160,000 (including the cost of land K60,000). Manufacturing operations Kairos Limited manufactures foodstuffs. The tax adjusted profit from manufacturing befor e deducting capital allowances was K979, 000. The company owns a building which was constructed in the year 2010 at a cost of K450,00 0. The factory was brought into use on 1 June 2010 for business purposes. The total cost of constructing the building of K450,000 comprised the following: Cost of land Factory Showroom Staff canteen Total During the year ended 31 December 2019, an extension was added to this factory at a cost of K160,000 (including the cost of land K60,000). Required: Farming operations. For the year ended 31 December 2019 Kairos Limited generated a profit from farming opera tions before capital allowances of K1,890,000, During the year, the company incurred expen diture of K54,000 on construction of a house for an employee at the farm, K270,000 on the growing of rose flowers and K78,000 to purchase a tractor. On 1 January 2019 there was at ax adjusted loss of K114,360 from farming operations, brought forward from the tax year 2 014 when it was incurred. Capital allowances on other farm implements, plant and machiner y amounted to K200,000, (a) K 69,000 200,000 70,000 Provisional income tax paid in respect of the tax year 2019, was K845,000. (b) 111,000 450,000 (0) (ii) (III) Compute the final taxable profit for the tax year 2019 from: Retail operations Manufacturing operations Farming operations 4 (4 marks) (8 marks) (4 marks) Prepare a computation of the final amount of income tax payable by Kairos Limited f or tax year 2019. (4 marks) [Total: 20 Marks] QUESTION THREE You are employed in a firm of Chartered Accountants. Your firm is dealing with the tax affair s of Matimba Ltd, a VAT registered trading company. You are helping the company in prepar ing the VAT return for the month of May 2019. The directors have heard that a business can account for VAT using the Cash Accounting Scheme and are keen to know Whether Matimb a Ltd can register to account for VAT under the cash accounting scheme. You have been provided with the following information relating to the month of May 2019. (1) Sales invoices totaling K2,750,000 were issued to customers out of which exempt sal es were K550,000 and zero rated sales were K320,000 with the remainder of the sales being standard rated. (2) (3) (4) (5) (6) (7) Out of the standard rated sales, goods with a value of K350,000 were sold on sale or return basis. These goods were dispatched to the customer on 30 May 2019, however the customer only paid for the goods on 2 June 2019, although he adopted the sale when he received goods. Total Sales returns for the month were K280,000 comprising returns on standard rate d sales of K170,000, returns on exempt sales of K30,000 and returns on zero rated sa les of K80,000. The company received an advance deposit of K85,000 in respect of a standard rated contract that is due for completion in July 2019. The contract has a total value of K1 50,000. Standard rated purchases were K980,000 and the purchase returns on these purchas e amounted to K83,000. Standard rated expenses amounted to K179,800 (VAT inclusive) broken down as follows: Entertaining customers Staff meals and refreshments Petrol for company cars Diesel for motor vans Telephone bills 5 Pool motor car Delivery van Air conditioners K 34,800 37,120 40,600 20,880 179,800 The company wrote off a bad debt amounting to K26,000 during the month of May 2 019, in respect of a debt which was due for payment on 31 October 2018. The company bought the following capital assets at the following VAT inclusive cost S: K 174,000 139,200 69,600 8. 9. 10. On 1 January 2020, SMC Plc held the following assets qualifying for capital allowan ces. All of the assets were acquired locally from Zambian suppliers: Old mining equipment Haulage Trucks Toyota Fortuner (3000cc) Toyota Prado car (2600cc) Bought office building at Sold old mining equipment for Bought new mining equipment Income Tax Value: at 1 January 2020 K 480,000 2,360,000 240,000 270,000 During the year ended 31 December 2020, the company entered into the following cal pital transactions: 8 13.80 14.40 Cost/(proceeds) K 5,000,000 (780,000) 4,000,000 Original Cost The Toyota Fortuner car and Toyota Prado car are used by the Chief Executive Officer The following are the Bank of Zambia average mid-rates: Year ZMW/US$1 2019 2020 K 2,400,000 4,720,000 600,000 450,000 and Operations Director respectively on personal-to-holder basis. The private usage in the motor cars is estimated to be 45% by each individual. The following indexation formula may be used where applicable: Required: (a) Compute the taxable mining profits for SMC plc for the year 2020. (16 marks) (b) Calculate the amount of company income tax payable by SMC Plc for the tax ye ar 2020. (4 marks) [Total: 20 Marks] QUESTION FIVE You are employed in the Tax department of a firm of Chartered Accountants. The tax manag er has presented you with the following information that has been extracted from the files o f the following clients of your firm: Brian Ntebeka Ntebeka, a sole trader, imported a second-hand panel van with a gross vehicle weight (GVW) of 2.5 tonnes, for exclusive use in his business in February 2020. The van was manufacture d in Japan in January 2010. The cost of the van was $3,700 (free on board). He incurred ins urance costs of $400, transportation costs of $900 in transit up to the port of Dar es salaam where clearing and forwarding costs of $200 were incurred. He incurred further incidental co sts of transporting the vehicle from Nakonde border post to Kapiri Mposhi amounting to $1, 200. In Kapiri vehicle registration fees were K1500, whilst motor car insurance costs were K 3,500. The exchange rate provided by the Commissioner General at the time of importation of the v ehicle was K14.50 per US$; however the exchange rates quoted in a local Bureau De Change was K14.80 Per US$ Cactus Ltd Cactus Ltd, is a VAT registered company making zero rated, standard rated and exempt sup plies. During the month of February 2020, the company made zero rated sales ofK630,000 which represented 15% of the total sales made in the month, standard rated sales represent ed 65% of the total sales made in the month and the remainder of the sales were exempt su pplies. The following expenditure was incurred during the month of February 2020: · Total purchases were K2,088,000 comprising standard rated purchases of K1,670,40 0 (VAT inclusive) and exempt purchases of K417,600. • Purchase of office furniture at a cost of K40,600 (VA inclusive) · Purchase of a pool car for K150,800 (VAT inclusive) 9 Other Information: • Purchase of a personal to holder motor car (with 50% private use by the Managing Di rector) at a cost of K162,400 (VAT inclusive) • Overheads of K165,418 (VAT inclusive). These comprised petrol for the personal to h older motor car of K18,560, petrol for pool cars of K20,880, diesel for the company's v ehicles of K34,800, entertainment expenses for employees of K5,338, electricity bills f or the managing director's accommodation of K4,640 and other general business ove rheads of K81,200. (1) The input VAT on the overheads cannot be attributed directly to neither taxable nor ex empt supplies. (2) Unless stated otherwise all of the above figures are exclusive of VAT. Required: (a) (b) Calculate the customs value of the panel van and the total import taxes paid by Nteb eka on the importation of the van. (8 marks) Compute the value added tax payable by Cactus Ltd for the month of February 2020. (1) (2) The input VAT on the overheads cannot be attributed directly to neither taxable nor ex empt supplies. Unless stated otherwise all of the above figures are exclusive of VAT. Required: (a) (b) Calculate the customs value of the panel van and the total import taxes paid by Nteb eka on the importation of the van. (8 marks) Compute the value added tax payable by Cactus Ltd for the month of February 2020. You should clearly indicate in your computation, by the use of a Zero (0), any items o n which VAT is not chargeable or not recoverable. (12 marks) [Totals: 20 Marks] 10 QUESTION SIX MNC Mining Corporation is a mining company operating an underground mine in Zambia. The company is engaged in the extraction of copper. The company made the following expo rts of copper in the following months of the charge year 2019: March 2019 June 2019 October 2019 December 2019 The Zambian kwacha per US$1 exchange rate approved by the Commissioner General from January 2019 to 31 December 2019 should be taken to be K11.50/ US$1. The average London Metal Exchange (LME) cash prices per metric tonne were as follows: US$6,300 March June October December (1) (1) (iii) US$5,900 US$7,600 US$4,400 Required: (a) Explain the meaning of the following terms in the context of the taxation of mining oper ations: 700 tonnes of Copper 1,000 tonnes of Copper 1,200 tonnes of Copper 500 tonnes of Copper Norm value Gross value Mineral Royalty (0) (ii) (b) Calculate the mineral royalty tax paid by the company, for each export, stating the due d ate for each payment. (8 marks) (c) Explain the consequences of the following: Paying mineral royalty late. (3 marks) (2 marks) (3 marks) Submitting the mineral royalty tax return late. (2 marks) (2 marks) [Total 20 Marks]

Expert Answer:

Answer rating: 100% (QA)

The answer provided below has been developed in a clear step by step mannerStep 1 My answer Answer T... View the full answer

Related Book For

Financial Accounting and Reporting

ISBN: 978-1292162409

18th edition

Authors: Barry Elliott, Jamie Elliott

Posted Date:

Students also viewed these economics questions

-

The following budgeted statement of profit or loss has been prepared for West Company for the four months January to April 2019 January February March April Sales $ 60,000 $50,000 $70,000 $ 60,000...

-

The summarized statements for the year ended 31 December 2007 for Mat, Rug and P entities are as follows: Statements of comprehensive income for the year ended 31 December 2007 The following...

-

The following summarized statement of profit or loss has been extracted from the financial statements of Gwembe Mining Corporation, a Zambian resident company which engaged in open cast mining...

-

Write a program that finds a contiguous subarray of length at most \(m\) in an array of \(n\) long integers that has the highest average value among all such subarrays, by trying all subarrays. Use...

-

Why is the relationship between the buyer and seller increasingly important to successful B2B marketing practices?

-

The password was CANARY; the employee entered CAANARY. Which control will detect this error?

-

A large nuclear power plant has a rated capacity of \(1 \mathrm{GW}\) electric. Its actual output is estimated to average about \(80 \%\) of capacity due to the need for maintenance and imperfect...

-

The Protek Company is a large manufacturer and distributor of electronic components. Because of some successful new products marketed to manufacturers of personal computers, the firm has recently...

-

3.Taxpayer, who is in the highest federal tax bracket in the current year, has a $5,000 gain from a collectible and a $5,000 gain from stock, both held long-term. (a) What is Taxpayer's net capital...

-

Jurassic Jumpers Co. (JJ Co.) offers bungee jumping for those looking for an extreme outing. JJ Co. prepares annual financial statements and has a December 31, 2023 yearend. a. On April 1, 2023, JJ...

-

Is rail capital cost the most large value of traffic to justify the expense? Justify this.

-

Perform the following arithmetic operations in their given bases. Explain or show the carries or borrows used whenever necessary. Also specify if you are switching the operands whenever necessary....

-

Write a program to display the following 1,5,13,25,41 The number needs to be generated automatically.

-

(i) Explain the suitable web architecture for the VTOP student portal. (ii) Write a JavaScript function to count total number of alphabets, digits and special characters in a string. Iput the string:...

-

By applying the Divide and Conquer strategy, sort the numbers 165, 23, 151, 5, 81, 72, 144, 128, 62, 56, 18, 29 and 801 by using (i) (ii) Quick Sort Algorithm Merge Sort Algorithm Provide the time...

-

What is the output of the following code, In visual basic Function SubStr( St As String) As String Sum=1 for x=1 to 8 if x mod 20 then S=Mid(St, x, x*2) S=Mid(St, x, x+2) Else End if Next x SubStr=S...

-

Identify why marketers might prefer narrowcasting over broadcasting to reach audiences associated with narrowcasting from the perspective of a consumer.

-

Why do bars offer free peanuts?

-

The approach in IAS 39 to the impairment of financial assets was flawed because it did not allow financial institutions to recognize the true losses they expected on loans at the time they had made...

-

International Financial Reporting Standards (IFRS) support the use of fair values when reporting the values of assets wherever practical. This involves periodic re-measurements of assets and the...

-

Rumpus plc is a public listed manufacturing company. Its summarized consolidated financial statements for the year ended 31 March 2014 (and 2013 comparatives where relevant) are as follows: Rumpus...

-

Consider an experiment that selects a cell phone camera and records the recycle time of a flash (the time taken to ready the camera for another flash). The possible values for this time depend on the...

-

Suppose that the recycle times of two cameras are recorded. The extension of the positive real line \(R\) is to take the sample space to be the positive quadrant of the plane \[ S=R^{+} \times R^{+}...

-

Each message in a digital communication system is classified as to whether it is received within the time specified by the system design. If three messages are classified, use a tree diagram to...

Study smarter with the SolutionInn App