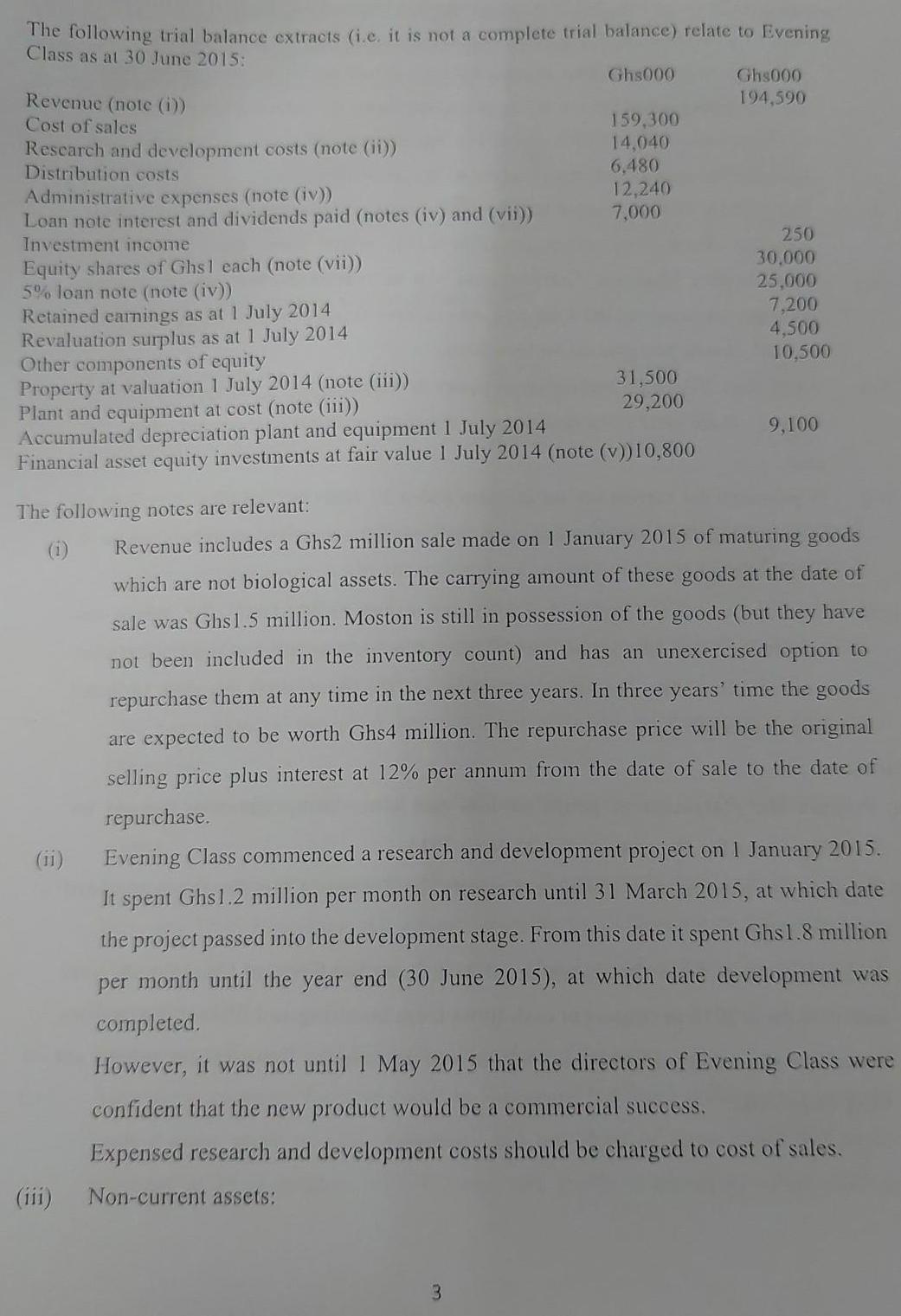

The following trial balance extracts (i.e. it is not a complete trial balance) relate to Evening...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

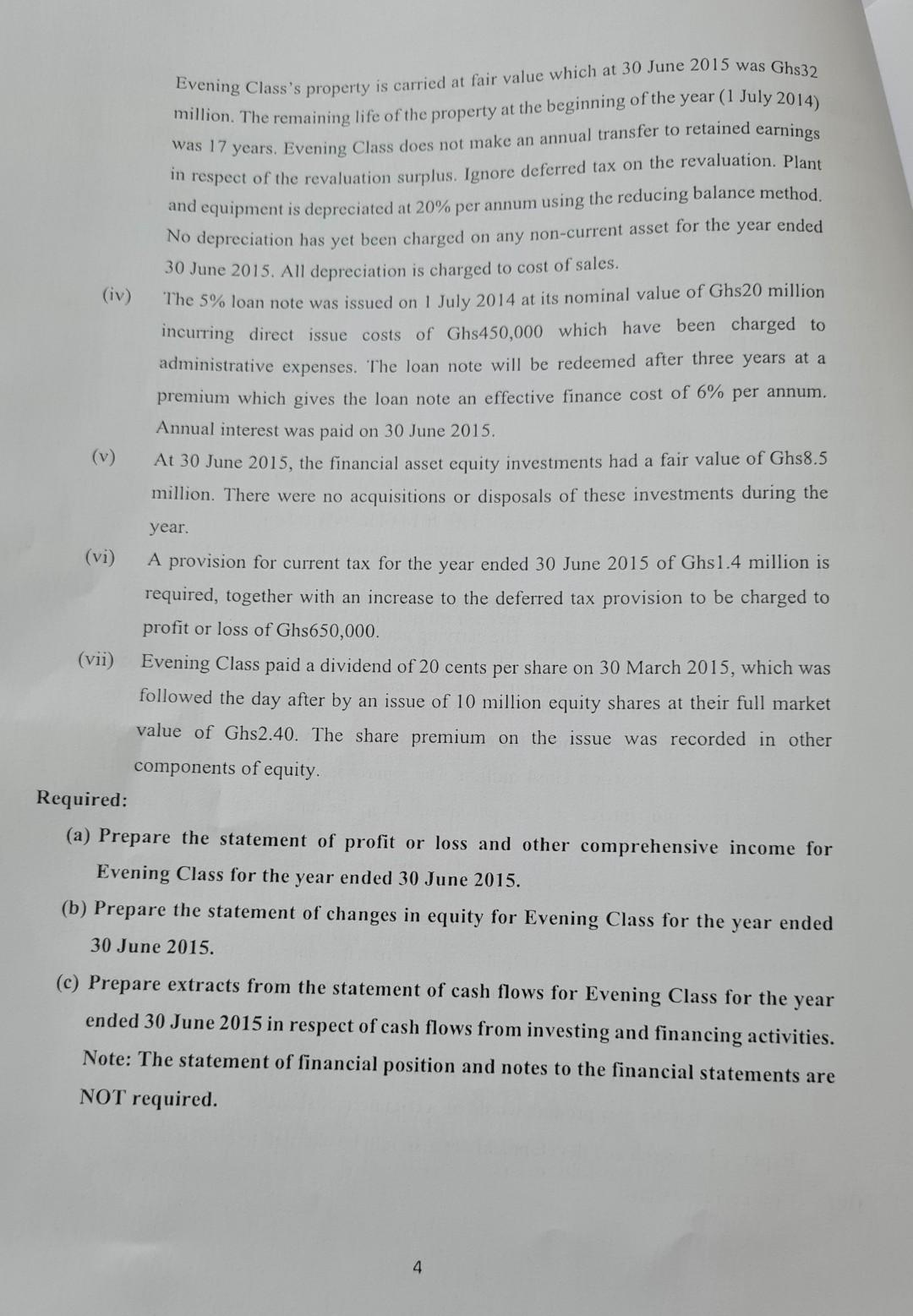

The following trial balance extracts (i.e. it is not a complete trial balance) relate to Evening Class as at 30 June 2015: Ghs000 Revenue (note (i)) Cost of sales Research and development costs (note (ii)) Distribution costs Administrative expenses (note (iv)) Loan note interest and dividends paid (notes (iv) and (vii)) Investment income Equity shares of Ghs1 each (note (vii)) 5% loan note (note (iv)) Retained earnings as at 1 July 2014 Revaluation surplus as at 1 July 2014 Other components of equity Property at valuation 1 July 2014 (note (iii)) Plant and equipment at cost (note (iii)) The following notes are relevant: Accumulated depreciation plant and equipment 1 July 2014 Financial asset equity investments at fair value 1 July 2014 (note (v))10,800 (ii) (iii) 159,300 14,040 6,480 12,240 7,000 31,500 29,200 3 Ghs000 194,590 250 30,000 25,000 7,200 4,500 10,500 9,100 Revenue includes a Ghs2 million sale made on 1 January 2015 of maturing goods which are not biological assets. The carrying amount of these goods at the date of sale was Ghs 1.5 million. Moston is still in possession of the goods (but they have not been included in the inventory count) and has an unexercised option to repurchase them at any time in the next three years. In three years' time the goods are expected to be worth Ghs4 million. The repurchase price will be the original selling price plus interest at 12% per annum from the date of sale to the date of repurchase. Evening Class commenced a research and development project on 1 January 2015. It spent Ghs 1.2 million per month on research until 31 March 2015, at which date the project passed into the development stage. From this date it spent Ghs1.8 million per month until the year end (30 June 2015), at which date development was completed. However, it was not until 1 May 2015 that the directors of Evening Class were confident that the new product would be a commercial success. Expensed research and development costs should be charged to cost of sales. Non-current assets: (iv) (v) (vi) (vii) Evening Class's property is carried at fair value which at 30 June 2015 was Ghs32 million. The remaining life of the property at the beginning of the year (1 July 2014) was 17 years. Evening Class does not make an annual transfer to retained earnings in respect of the revaluation surplus. Ignore deferred tax on the revaluation. Plant and equipment is depreciated at 20% per annum using the reducing balance method. No depreciation has yet been charged on any non-current asset for the year ended 30 June 2015. All depreciation is charged to cost of sales. The 5% loan note was issued on 1 July 2014 at its nominal value of Ghs20 million incurring direct issue costs of Ghs450,000 which have been charged to administrative expenses. The loan note will be redeemed after three years at a premium which gives the loan note an effective finance cost of 6% per annum. Annual interest was paid on 30 June 2015. At 30 June 2015, the financial asset equity investments had a fair value of Ghs8.5 million. There were no acquisitions or disposals of these investments during the year. A provision for current tax for the year ended 30 June 2015 of Ghs1.4 million is required, together with an increase to the deferred tax provision to be charged to profit or loss of Ghs650,000. Evening Class paid a dividend of 20 cents per share on 30 March 2015, which was followed the day after by an issue of 10 million equity shares at their full market value of Ghs2.40. The share premium on the issue was recorded in other components of equity. Required: (a) Prepare the statement of profit or loss and other comprehensive income for Evening Class for the year ended 30 June 2015. (b) Prepare the statement of changes in equity for Evening Class for the year ended 30 June 2015. (c) Prepare extracts from the statement of cash flows for Evening Class for the year ended 30 June 2015 in respect of cash flows from investing and financing activities. Note: The statement of financial position and notes to the financial statements are NOT required. 4 The following trial balance extracts (i.e. it is not a complete trial balance) relate to Evening Class as at 30 June 2015: Ghs000 Revenue (note (i)) Cost of sales Research and development costs (note (ii)) Distribution costs Administrative expenses (note (iv)) Loan note interest and dividends paid (notes (iv) and (vii)) Investment income Equity shares of Ghs1 each (note (vii)) 5% loan note (note (iv)) Retained earnings as at 1 July 2014 Revaluation surplus as at 1 July 2014 Other components of equity Property at valuation 1 July 2014 (note (iii)) Plant and equipment at cost (note (iii)) The following notes are relevant: Accumulated depreciation plant and equipment 1 July 2014 Financial asset equity investments at fair value 1 July 2014 (note (v))10,800 (ii) (iii) 159,300 14,040 6,480 12,240 7,000 31,500 29,200 3 Ghs000 194,590 250 30,000 25,000 7,200 4,500 10,500 9,100 Revenue includes a Ghs2 million sale made on 1 January 2015 of maturing goods which are not biological assets. The carrying amount of these goods at the date of sale was Ghs 1.5 million. Moston is still in possession of the goods (but they have not been included in the inventory count) and has an unexercised option to repurchase them at any time in the next three years. In three years' time the goods are expected to be worth Ghs4 million. The repurchase price will be the original selling price plus interest at 12% per annum from the date of sale to the date of repurchase. Evening Class commenced a research and development project on 1 January 2015. It spent Ghs 1.2 million per month on research until 31 March 2015, at which date the project passed into the development stage. From this date it spent Ghs1.8 million per month until the year end (30 June 2015), at which date development was completed. However, it was not until 1 May 2015 that the directors of Evening Class were confident that the new product would be a commercial success. Expensed research and development costs should be charged to cost of sales. Non-current assets: (iv) (v) (vi) (vii) Evening Class's property is carried at fair value which at 30 June 2015 was Ghs32 million. The remaining life of the property at the beginning of the year (1 July 2014) was 17 years. Evening Class does not make an annual transfer to retained earnings in respect of the revaluation surplus. Ignore deferred tax on the revaluation. Plant and equipment is depreciated at 20% per annum using the reducing balance method. No depreciation has yet been charged on any non-current asset for the year ended 30 June 2015. All depreciation is charged to cost of sales. The 5% loan note was issued on 1 July 2014 at its nominal value of Ghs20 million incurring direct issue costs of Ghs450,000 which have been charged to administrative expenses. The loan note will be redeemed after three years at a premium which gives the loan note an effective finance cost of 6% per annum. Annual interest was paid on 30 June 2015. At 30 June 2015, the financial asset equity investments had a fair value of Ghs8.5 million. There were no acquisitions or disposals of these investments during the year. A provision for current tax for the year ended 30 June 2015 of Ghs1.4 million is required, together with an increase to the deferred tax provision to be charged to profit or loss of Ghs650,000. Evening Class paid a dividend of 20 cents per share on 30 March 2015, which was followed the day after by an issue of 10 million equity shares at their full market value of Ghs2.40. The share premium on the issue was recorded in other components of equity. Required: (a) Prepare the statement of profit or loss and other comprehensive income for Evening Class for the year ended 30 June 2015. (b) Prepare the statement of changes in equity for Evening Class for the year ended 30 June 2015. (c) Prepare extracts from the statement of cash flows for Evening Class for the year ended 30 June 2015 in respect of cash flows from investing and financing activities. Note: The statement of financial position and notes to the financial statements are NOT required. 4

Expert Answer:

Answer rating: 100% (QA)

a Prepare statent of Prof it or loss and the Compre ... View the full answer

Related Book For

Financial Accounting and Reporting

ISBN: 978-1292162409

18th edition

Authors: Barry Elliott, Jamie Elliott

Posted Date:

Students also viewed these accounting questions

-

The trial balance for Eureka Ltd as at 30 June 2012 (before calculation of income tax) is as follows: Note: this is the first year of operation of Eureka Ltd. DR CR $000 $000 Sales Revenue 1235 Cost...

-

The annual research and development costs for Frontier Biotech for years 2002 through 2006 are shown here ($ millions): Required: a. Comment on the manner in which research and development costs...

-

The Holly Company incurred research and development costs in Year 1 as follows: Equipment acquired for use in various R& D projects $400,000 Depreciation on the above equipment . 60,000 Materials...

-

Discuss the seven contemporary communication issues facing managers.

-

What is a testamentary trust?

-

Determine whether each function is one-to-one. If it is, find the inverse. {(1, 5.8), (2, 8.8), (3, 8.5)}

-

Determine the vertical displacement of point \(C\). The frame is made using A-36 steel W250 \(\times 45\) members. Consider only the effect of bending. 15 kN D 15 kN/m 5 m A B C -2.5 m- -2.5 m-

-

Patty Bayan is a single taxpayer living at 543 Space Drive, Houston, TX 77099. Her Social Security number is 466-33-1234. For 2014, Patty has no dependents, and her W-2 from her job at a local...

-

Two agents meet to trade two goods. Agent 1 has preferences representable by utility func- tion u (x()) = x() (x()), while agent 2's preferences are representable by utility function u (x(2)) (x(2))...

-

TipTop Flight School offers flying lessons at a small municipal airport. The school's owner and manager has been attempting to evaluate performance and control costs using a variance report that...

-

Assume that you are working in a company and you believe that your supervisor gave you a pay raise that is unfair and less than you deserve based on your performance. This is not the first time this...

-

MargeSimpson Inc. is considering the two capital budeting projects with the following cash flows that have a WACC of 10%. How 'Bout A Pretzel Year What a Falafel -150,000 -150,000 1 30,000 90,000 2...

-

As employees health changes, they may miss work due to illness or injury increasing healthcare cost for employees and employers. Furthermore, employees may be less productive while at work due to...

-

Jones Company reports the following financial information for the current year: Net Sales $ 30,000 Cost of Goods Sold 9,000 Gross Profit 21,000 Operating Expenses 6,000 Operating Income 15,000...

-

Moerdyk & Co. is considering Projects S and L, whose cash flows are shown below. These projects are mutually exclusive, equally risky, and not repeatable. If the decision is made by choosing the...

-

Assume I have a stack of integer elements called st. What is going to be printed after I run the following statements? st.push(2); st.push(5); st.pop(); st.push(1); st.peek(); st.push(12);...

-

Francois sets aside about $100 per month to purchase scratch-off lottery tickets and cigars. The price of each lottery ticket is given my P. The price of each cigar is given by Pe. His marginal...

-

KD Insurance Company specializes in term life insurance contracts. Cash collection experience shows that 20 percent of billed premiums are collected in the month before they are due, 60 percent are...

-

James Bright has just taken up the position of managing director following the unsatisfactory achievements of the previous incumbent. James arrives as the accounts for the previous year are being...

-

Scott Ross, CFO of Ryan Industries PLC, is discussing the publication of the annual report with his managing director Nathan Davison. Graydon says: 'The law requires us to comply with accounting...

-

The following are the summarized financial statements of two companies, Peel and Caval, for the financial year ended 31 October 2011. Income Statements for the year ended 31 October 2011 Statements...

-

The bar is subjected to a moment M = 40 Nm of Determine the smallest radius r of the fillets so that an allowable bending stress of allow = 124MPa is not exceeded. M 20 mm 80 mm 7 mm M

-

The bar is subjected to a moment of M = 17.5 N m. If r=5mm determine the maximum bending stress in the material. M 80 mm 7 mm 20 mm M

-

The simply supported notched bar is subjected to the two loads, each having a magnitude of P = 100 lb. Determine the maximum bending stress developed in the bar, and sketch the bending-stress...

Study smarter with the SolutionInn App