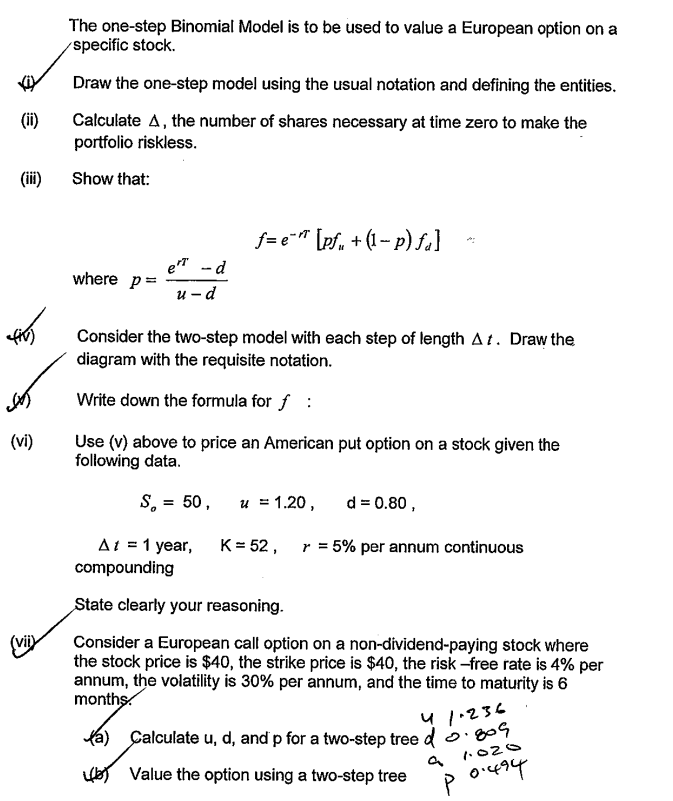

Question: The one-step Binomial Model is to be used to value a European option on a specific stock. Draw the one-step model using the usual

The one-step Binomial Model is to be used to value a European option on a specific stock. Draw the one-step model using the usual notation and defining the entities. (ii) Calculate A, the number of shares necessary at time zero to make the portfolio riskless. (!!!) Show that: fiv (vi) (vii) where p = e' -d u-d f=e [p + (1 - p) fa] Consider the two-step model with each step of length At. Draw the diagram with the requisite notation. Write down the formula for f : Use (v) above to price an American put option on a stock given the following data. S = 50, u = 1.20, d = 0.80, At = 1 year, K = 52, r = 5% per annum continuous compounding State clearly your reasoning. Consider a European call option on a non-dividend-paying stock where the stock price is $40, the strike price is $40, the risk-free rate is 4% per annum, the volatility is 30% per annum, and the time to maturity is 6 months 41.236 (a) Calculate u, d, and p for a two-step tree d 0.809 (b) Value the option using a two-step tree a 1.020 P0.494

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts