Question: The premium on a call option is primarly a function of the difference in spot price S relative to the strike price X, the length

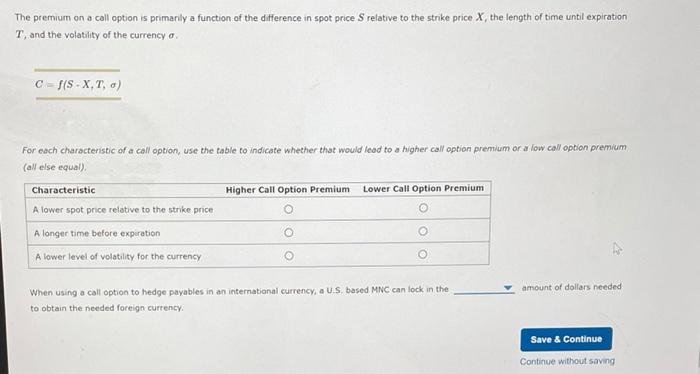

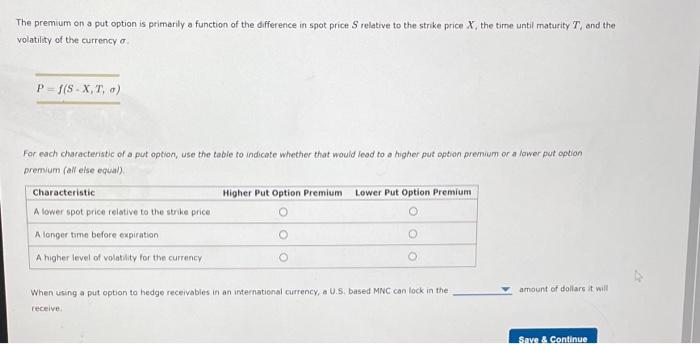

The premium on a call option is primarly a function of the difference in spot price S relative to the strike price X, the length of time until expiration T, and the volatility of the currency . C=f(SX,T,) For each characteristic of a call option, use the table to indicate whether that would lead to a higher call option premium or a low call option premium (all else equal) When using a call option to hedge payables in an internatianal currency, a U.S. based MNC can lock in the amount of dollars needed to obtain the needed foreign currency. The premium on a put option is primarily a function of the difference in spot price S relative to the strike price X, the time until maturity T, and the volatility of the currency P=f(SX,T,) For each characteristic of a put option, use the table to indicate whether that would lead to a higher put option premium or a lower put aotion premium (an eise equal) When using a put option to hedge receivables in an international currency, a U.S. based MNC can lock in the amount of dollars it will receive

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts