Question: The problem below presents the output from a linear regression model, and one implication of the regression output is that the bid-ask spread for NASDAQ-listed

The problem below presents the output from a linear regression model, and one implication of the regression output is that the bid-ask spread for NASDAQ-listed stocks declines by nearly one-half cent per share if the trading volume increases by 10%. Does it make sense that there should be a negative relationship between the bid-ask spread and trading volume? Does the magnitude of this estimated relationship (i.e., -$0.005 per share given a 10% increase in volume) seem reasonable to you? If not, would you expect the magnitude to be larger or smaller? Please explain your responses.

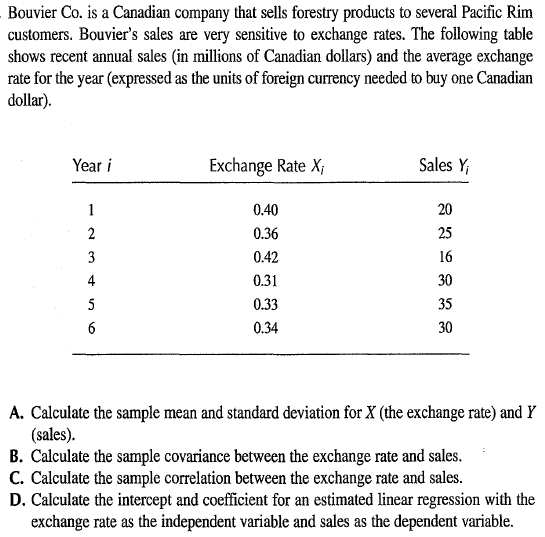

Bouvier Co. is a Canadian company that sells forestry products to several Pacific Rim customers. Bouvier's sales are very sensitive to exchange rates. The following table shows recent annual sales (in millions of Canadian dollars) and the average exchange rate for the year (expressed as the units of foreign currency needed to buy one Canadian dollar). Year i Exchange Rate X; Sales y 1 2 3 4 0.40 0.36 0.42 0.31 0.33 0.34 20 25 16 30 35 30 5 6 A. Calculate the sample mean and standard deviation for X (the exchange rate) and Y (sales). B. Calculate the sample covariance between the exchange rate and sales. C. Calculate the sample correlation between the exchange rate and sales. D. Calculate the intercept and coefficient for an estimated linear regression with the exchange rate as the independent variable and sales as the dependent variable

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts