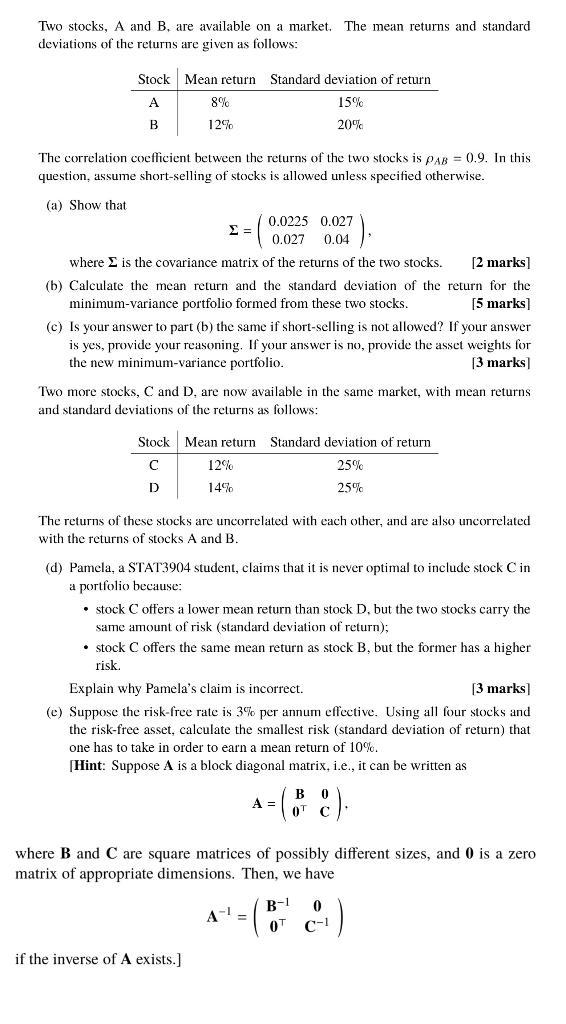

Two stocks, A and B. are available on a market. The mean returns and standard deviations...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a The covari ance matrix of the returns of the two stocks can be calculated as follows C ov A B PA BC ov A B 0 9 x 0 15 x 0 20 0 027 The covari ance m... View the full answer

Related Book For

Posted Date: