Question: The question is attached as below: (The question is comprehensive, no missing data or diagram about this question) Consider the following generalized autoregressive conditional heteroskedasticity

The question is attached as below:

(The question is comprehensive, no missing data or diagram about this question)

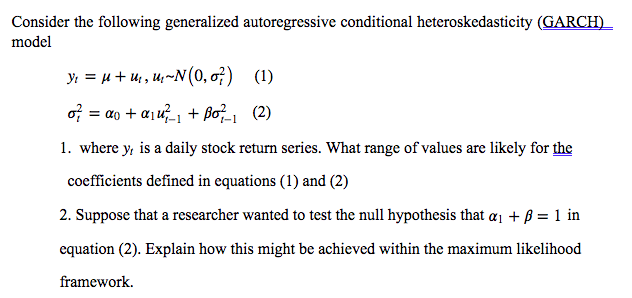

Consider the following generalized autoregressive conditional heteroskedasticity (GARCH) model y = N+ u, u,-N(0, o? ) (1) o? = do + alu_ + Bo? (2) 1. where y, is a daily stock return series. What range of values are likely for the coefficients defined in equations (1) and (2) 2. Suppose that a researcher wanted to test the null hypothesis that an + p = 1 in equation (2). Explain how this might be achieved within the maximum likelihood framework

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock