Question: The second interview is with Mr Isabelo, the quantitative expert. The purpose of this interview is to assess your risk measurement skills. Assume an investment

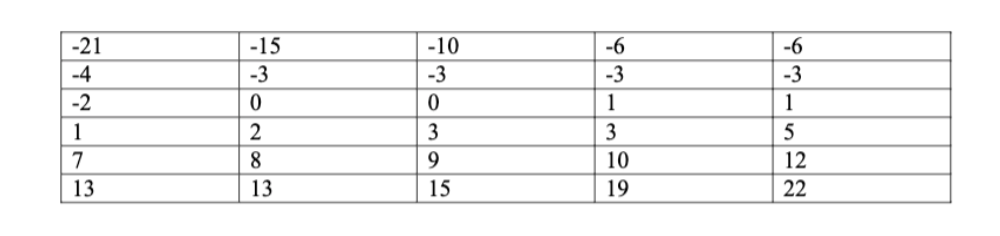

The second interview is with Mr Isabelo, the quantitative expert. The purpose of this interview is to assess your risk measurement skills. Assume an investment firm holds an equity stock with a unit price of $75. The policy of the firm sets its risk limit to 90% VaR (Value at Risk) and ES (expected shortfall) for any individual security. Risk measures are based on a set of 30 historical return data points, as provided in the table below. The returns are ordered and provided in percentage (%) terms.

(e) Interpret the results of 90% VaR and ES and compare them with the 95% results. Explain their significance for the investment firm.

(5 marks)

-21 -4 -2 1 7 13 -15 -3 0 2 8 13 -10 -3 0 3 9 15 -6 -3 1 3 10 19 -6 -3 1 5 12 22 -21 -4 -2 1 7 13 -15 -3 0 2 8 13 -10 -3 0 3 9 15 -6 -3 1 3 10 19 -6 -3 1 5 12 22

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts