Question: There are two risky assets, D and E . ?The expected returns of D and E are 8% and 12%, respectively. ?The standard deviation of

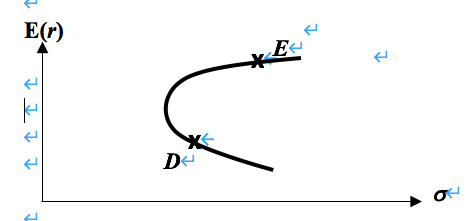

There are two risky assets, D and E . ?The expected returns of D and E are 8% and 12%, respectively. ?The standard deviation of D and E are 10% and 25%, respectively. The correlation between the assets is positive and less than 1.

(a) Suppose an investor is indifferent between holding 100% in D and holding 100% in E . ?What is his risk aversion A ?

(b) From the different combinations of D and E , you can identify the portfolio that gives you the lowest standard deviation, which is the minimum variance portfolio, A . Can A , D , and E lie on the same utility indifference curve for the investor in part (a)? ?Briefly explain. ?

E(r) tttt De E Of

Step by Step Solution

3.39 Rating (143 Votes )

There are 3 Steps involved in it

To address the questions well consider key concepts in portfolio theory a Risk Aversion A When an in... View full answer

Get step-by-step solutions from verified subject matter experts