Question: On April 13, 2017, Splish Ltd. purchased a small apartment building with eight suites. The building qualified as an investment property under IAS 40. At

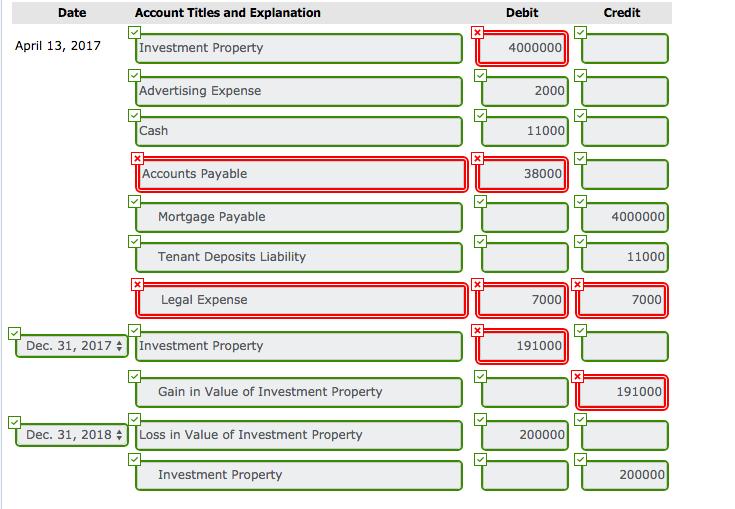

On April 13, 2017, Splish Ltd. purchased a small apartment building with eight suites. The building qualified as an investment property under IAS 40. At the time of purchase, six out of the eight suites were rented. Splish paid the following items at the time of its acquisition of the apartment building (all items were paid in cash except for the building itself, for which Splish took out a mortgage):

| Purchase price of building | $4,000,000 |

| Legal fees | 7,000 |

| Property transfer fees | 24,000 |

| Painting of empty apartments | 5,000 |

| Advertising for empty apartments | 2,000 |

In addition, the previous owner of the apartment building paid Splish $11,000 for damage deposits from the existing tenants.

On December 31, 2017, the apartment building had a fair value of $4,191,000. On December 31, 2018, it was determined that the apartment building had a fair value of $3,991,000.

Assuming that Splish follows IFRS, prepare the journal entries required to record the above events. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts. Record entries in the order presented in the problem.)

Date Account Titles and Explanation Debit Credit April 13, 2017 Investment Property 4000000 Advertising Expense 2000 Cash 11000 Accounts Payable 38000 Mortgage Payable 4000000 Tenant Deposits Liability 11000 Legal Expense 7000 7000 Dec. 31, 2017 +|Investment Property 191000 Gain in Value of Investment Property 191000 Dec. 31, 2018 +| Loss in Value of Investment Property 200000 Investment Property 200000

Step by Step Solution

3.59 Rating (167 Votes )

There are 3 Steps involved in it

Date Account Titles and Explanation Debit Credit April 13 ... View full answer

Get step-by-step solutions from verified subject matter experts