Question: True or False questions Exatan Name TRUE/FALSE. Write 'T' if the statement is true and 'F if the statement is false. 1) If the misstatement

True or False questions

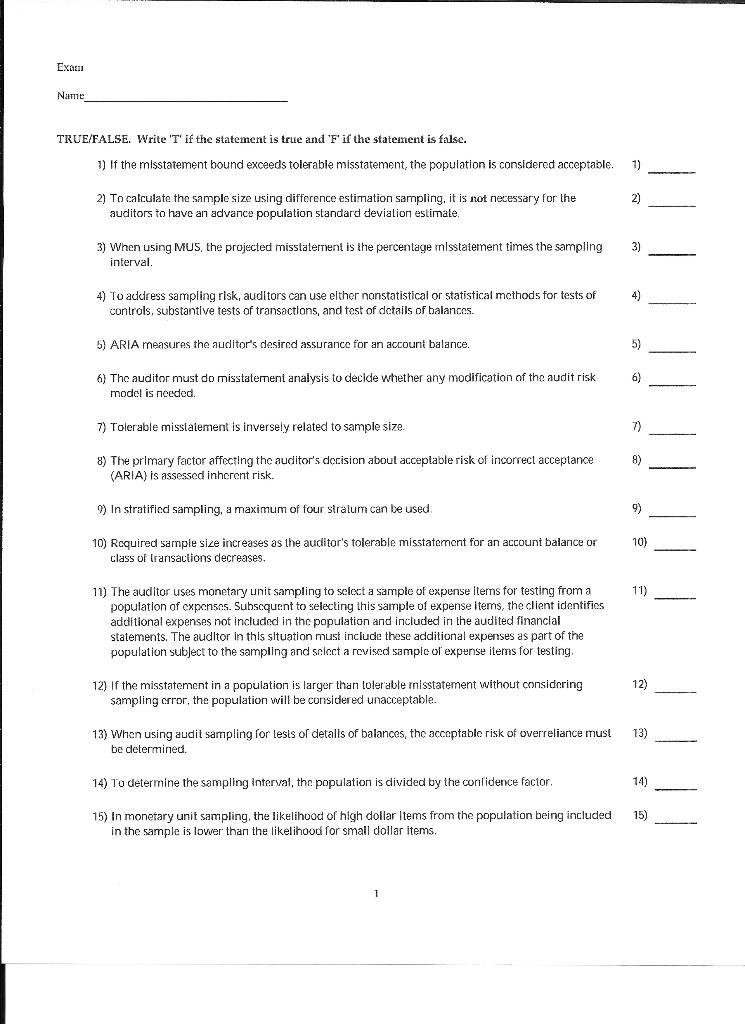

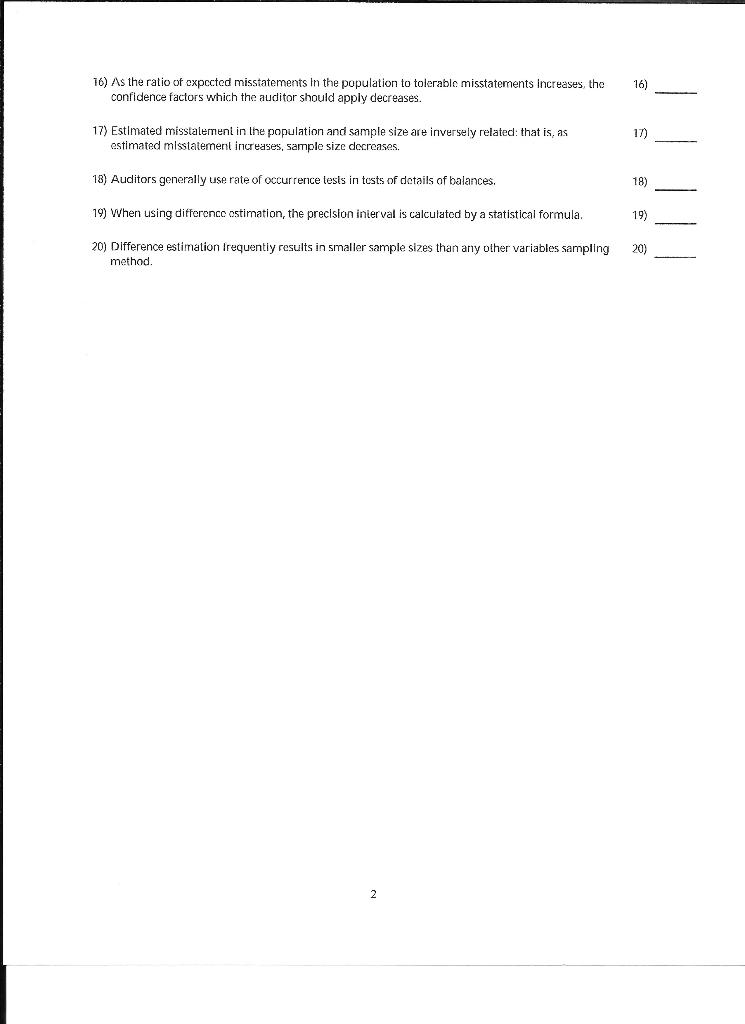

Exatan Name TRUE/FALSE. Write 'T' if the statement is true and 'F if the statement is false. 1) If the misstatement bound exceeds tolerable misstatement, the population considered acceptable. 1). 2) 2) To calculate the sample size using difference estimation sampling, it is not necessary for the auditors to have an advance population standard deviation estimale. 3) 3) When using MUS, the projected misstatement is the percentage misstaternent times the sampling interval 4) 4) To address sampling risk, auditors can use elther nonstatistical or statistical methods for tests of controls, substantive tests of transactions, and test of details of balances 5) ARIA measures the auditor's desired assurance for an account balance. 5) 6) 6) The auditor must do misstatement analysis to decide whether any modification of the audit risk model is needed 7) Tolerable misstatement is inversely related to sample size. 7) 8) 8) The primary factor affecting the auditor's decision about acceplable risk of incorrect acceptance (ARIA) is assessed inherent risk. 9) In stratified sampling, a maximum of four stratum can be used 10) 10) Rcquired sample size increases as the auditor's tolerable misstatement for an account balance or class of transactions decreases. 11) 11) The auditor uses monetary unit sampling to select a sample of expense items for testing from a population of expenses. Subscquent to selecting this sample of expense items, the client identifics additional expenses not included in the population and included in the audited financial statements. The auditor in this situation must include these additional expenses as part of the population subject to the sampling and select a revised sample of expense items for testing, 12) 12) If the misstatement in a population is larger than tolerable misstatement without considering sampling crror, the population will be considered unacceptable. 13) 13) When using audit sampling for lesis of details of balances, the acceptable risk of overreliance must be determined 14) To determine the sampling interval, the population is divided by the conlidence factor 14) 15) 15) In monetary unit sampling, the likelihood of high dollar Items from the population being included in the sample is lower than the likelihood for small dollar items. 16) As the ratio of expected misstatements in the population to tolerable misstatements Increases the confidence factors which the auditor should apply decreases. 16) 17) Estimated misstalement in the population and sample size are inversely related that is, as estimated misstatement increases, sample size decreases. 17) 18) Auditors generally use rate of occurrence tests in tests of details of balances, 18) 19) When using difference ostimation, the precision interval is calculated by a statistical formula 19) 20) Difference estimation frequently results in smaller sample sizes than any other variables sampling method. 20) 2

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts