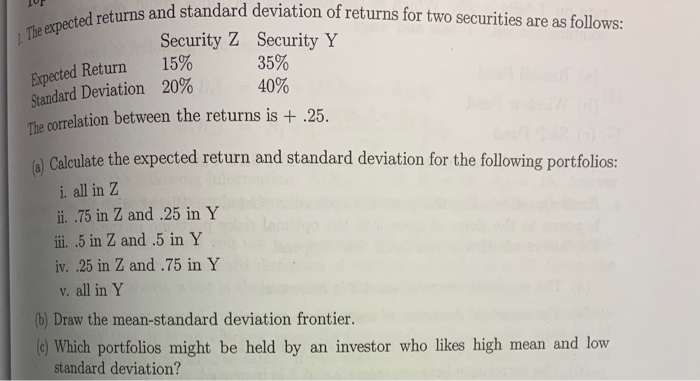

Question: TUT The expected returns and star os and standard deviation of returns for two securities are as follows: Security Z Security Y 35% Standard Deviation

TUT The expected returns and star os and standard deviation of returns for two securities are as follows: Security Z Security Y 35% Standard Deviation 20% 40% The correlation between the returns is + .25. 15% Expected Return Calculate the expected return and standard deviation for the following portfolios: i all in Z ii. .75 in Z and .25 in Y iii. .5 in Z and .5 in Y iv. 25 in Z and .75 in Y v. all in Y (b) Draw the mean-standard deviation frontier. (C) Which portfolios might be held by an investor who likes high mean and low standard deviation

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock