Question: urgent .. please help Given there are two assets making up a portfolio where each asset has the following characteristics: Asset Risk (standard deviation) Expected

urgent .. please help

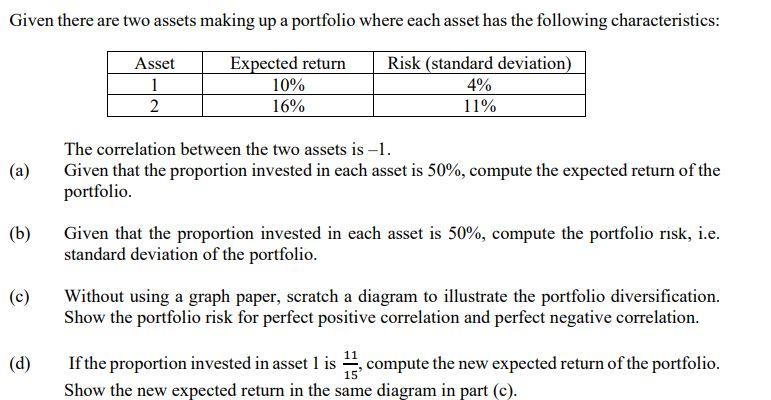

Given there are two assets making up a portfolio where each asset has the following characteristics: Asset Risk (standard deviation) Expected return 10% 1 4% 2 16% 11% The correlation between the two assets is -1. (a) Given that the proportion invested in each asset is 50%, compute the expected return of the portfolio. (b) Given that the proportion invested in each asset is 50%, compute the portfolio risk, i.e. standard deviation of the portfolio. (c) Without using a graph paper, scratch a diagram to illustrate the portfolio diversification. Show the portfolio risk for perfect positive correlation and perfect negative correlation. (d) If the proportion invested in asset 1 is , compute the new expected return of the portfolio. Show the new expected return in the same diagram in part (c)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts