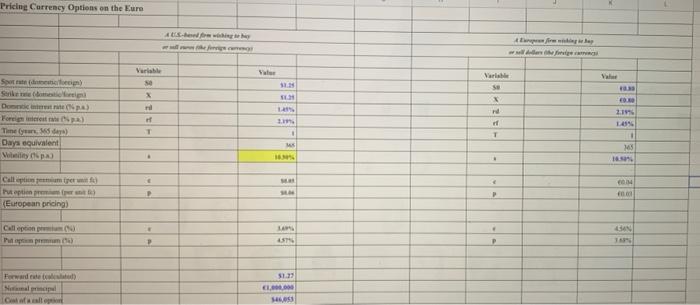

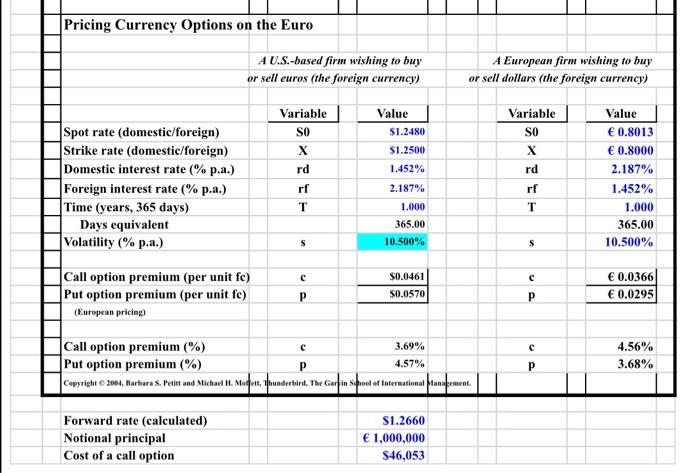

Question: U.S. Dollar/Euro. The table below indicates that a 1-year call option on euros at a strike rate of $1.25/ will cost the buyer $0.0632/, or

U.S. Dollar/Euro. The table below indicates that a 1-year call option on euros at a strike rate of $1.25/ will cost the buyer $0.0632/, or 4.99%. But that assumed a volatility of 12.000% when the spot rate was $1.2674/. What would that same call option cost if the volatility was reduced to 10.500% when the spot rate fell to $1.2480/? Pricing Currency Options on the Euro fra Variable Se Spre deo) Variable SB 1 f LAS Denta) Forest) The de Daya equivalent Vyp T 1 ws 3 CON P P Peti prema European pricing) . GAN Popman 45 P Erwarde te 51.17 EL Case Pricing Currency Options on the Euro A U.S.-based firm wishing to buy or sell euros (the foreign currency) A European firm wishing to buy or sell dollars (the foreign currency) Value $1.2480 Variable SO X Spot rate (domestic/foreign) Strike rate (domestic/foreign) Domestic interest rate (%p.a.) Foreign interest rate (% p.a.) Time (years, 365 days) Days equivalent Volatility (% p.a.) Variable SO X rd rf T $1.2500 1.452% 2.187% 1.000 365.00 10.500% rd rf T Value 0.8013 0.8000 2.187% 1.452% 1.000 365.00 10.500% S S c Call option premium (per unit fe) Put option premium (per unit fe) (European pricing) 30.0461 $0.0570 0.0366 0.0295 P C Call option premium (%) 3.69% Put option premium (%) P 4.57% Copyright 2006, Barbara S. Petitt and Michael H. Met Thunderbird, The Garf in school of International tanagement 4.56% 3.68% Forward rate (calculated) Notional principal Cost of a call option $1.2660 1,000,000 $46,053 U.S. Dollar/Euro. The table below indicates that a 1-year call option on euros at a strike rate of $1.25/ will cost the buyer $0.0632/, or 4.99%. But that assumed a volatility of 12.000% when the spot rate was $1.2674/. What would that same call option cost if the volatility was reduced to 10.500% when the spot rate fell to $1.2480/? Pricing Currency Options on the Euro fra Variable Se Spre deo) Variable SB 1 f LAS Denta) Forest) The de Daya equivalent Vyp T 1 ws 3 CON P P Peti prema European pricing) . GAN Popman 45 P Erwarde te 51.17 EL Case Pricing Currency Options on the Euro A U.S.-based firm wishing to buy or sell euros (the foreign currency) A European firm wishing to buy or sell dollars (the foreign currency) Value $1.2480 Variable SO X Spot rate (domestic/foreign) Strike rate (domestic/foreign) Domestic interest rate (%p.a.) Foreign interest rate (% p.a.) Time (years, 365 days) Days equivalent Volatility (% p.a.) Variable SO X rd rf T $1.2500 1.452% 2.187% 1.000 365.00 10.500% rd rf T Value 0.8013 0.8000 2.187% 1.452% 1.000 365.00 10.500% S S c Call option premium (per unit fe) Put option premium (per unit fe) (European pricing) 30.0461 $0.0570 0.0366 0.0295 P C Call option premium (%) 3.69% Put option premium (%) P 4.57% Copyright 2006, Barbara S. Petitt and Michael H. Met Thunderbird, The Garf in school of International tanagement 4.56% 3.68% Forward rate (calculated) Notional principal Cost of a call option $1.2660 1,000,000 $46,053

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts