Question: Use the data in Table 2 below. Correlations and volatilities are updated using a GARCH (1,1) model. Estimates of the model's parameters are a-0.04 and

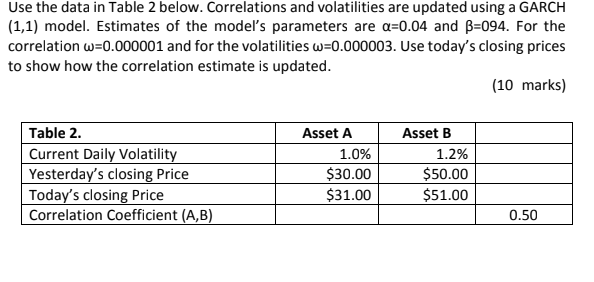

Use the data in Table 2 below. Correlations and volatilities are updated using a GARCH (1,1) model. Estimates of the model's parameters are a-0.04 and B 094. For the correlation uu-.000001 and for the volatilities u)-.000003. Use today's closing prices to show how the correlation estimate is updated. (10 marks) Table 2 Current Daily Volatility Yesterday's closing Price Today's closing Price Correlation Coefficient (A,B) Asset A Asset B 1.0% $30.00 $31.00 1.2% $50.00 $51.00 0.50 Use the data in Table 2 below. Correlations and volatilities are updated using a GARCH (1,1) model. Estimates of the model's parameters are a-0.04 and B 094. For the correlation uu-.000001 and for the volatilities u)-.000003. Use today's closing prices to show how the correlation estimate is updated. (10 marks) Table 2 Current Daily Volatility Yesterday's closing Price Today's closing Price Correlation Coefficient (A,B) Asset A Asset B 1.0% $30.00 $31.00 1.2% $50.00 $51.00 0.50

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts