Use the dividend discount model to value a share of Toyotas stock (ticker symbol: TM) as of

Question:

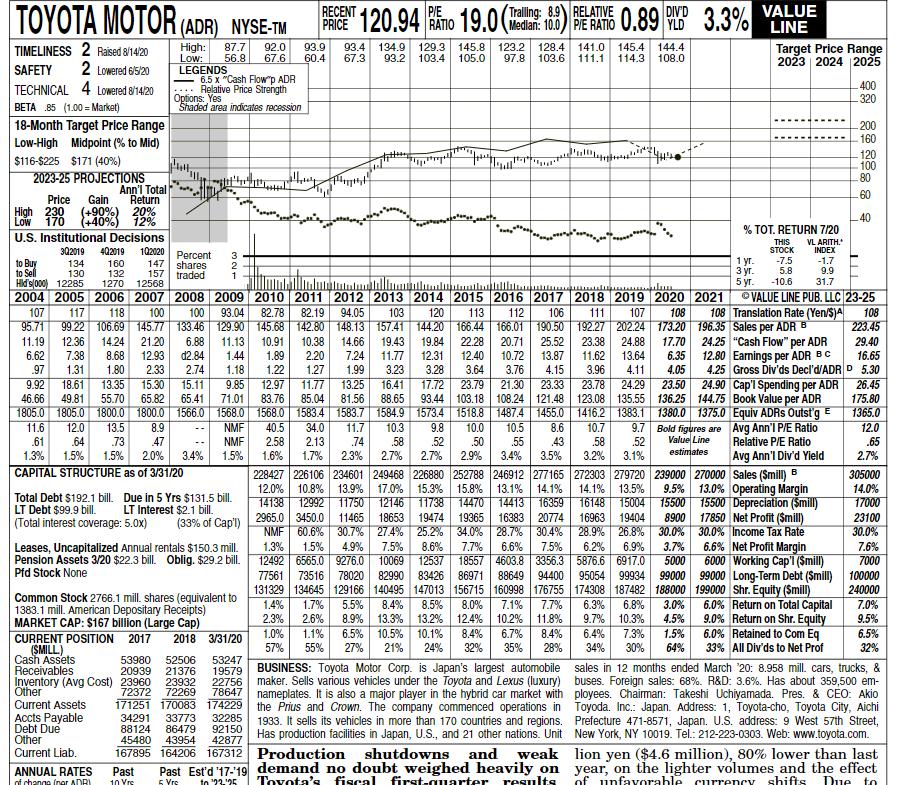

Use the dividend discount model to value a share of Toyota’s stock (ticker symbol: TM) as of December 31, 2021. In your application of this model, use the data provided on the most recent Toyota Value Line report (history of their annual dividend payments, forecasts of future annual dividend payments, past and forecasted growth rates in dividends, and Value Line’s estimate of Toyota’s equity beta). Given all the dividend data (historic and forecasted) presented in the Value Line report, explain, in one sentence, the logic you used to estimate the expected future constant growth rate in dividends in perpetuity (g). Since Toyota is a non-US firm, dividends per share on Value Line are referred to as Gross Dividends Declared per ADR. On direction on how to access Value line report, explain in one sentence, the logic you to estimate the expected future constant growth rate in dividend in perpetuity(g)

Expert Answer:

Corporate Finance

ISBN: 978-0077861759

10th edition

Authors: Stephen Ross, Randolph Westerfield, Jeffrey Jaffe