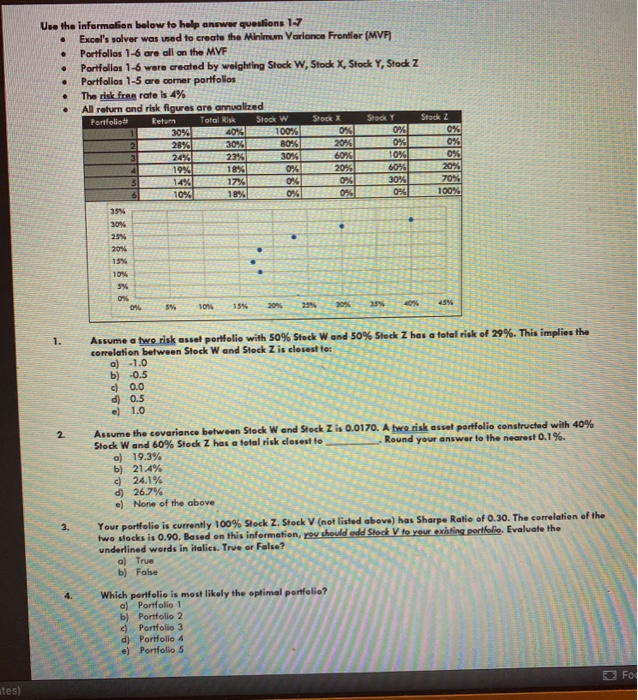

Question: Use the information below to help answer questions 1-7 Excel's solver was used to create the Minimum Variance Frontier (MVP Portfolios 1-6 ore all on

Use the information below to help answer questions 1-7 Excel's solver was used to create the Minimum Variance Frontier (MVP Portfolios 1-6 ore all on the MVF Portfolios 1-6 were created by weighting Stock W, Stock X Stock Y, Stock Portfolios 1-5 ore comer portfolios The risk free rate is 4% All return and risk figures are annualized Ponfoliots Retum Total Risk Stock W Stock X SY 11_ 30% 40% 100% 0% 2 28% 30% 80% 20%20%D0% 24% 23% 30% 60% 10% 0% 4 1 % 18% 0% 20% 60% 20% 14% 17% 0 % 20% 70% 10% 18% 0% 0% 0% 100% S88666 0% 5% 10% 15% 20% 25 Assume a two risk asset portfolio with 50% Stock Wand correlation between Stock Wand Stock Z is closest to: a) -1.0 b) -0.5 0 0.0 d) 0.5 .) 1.0 Assume the covariance between Stock Wand S Stock Wand 60% Stock Z has a total risk doses a) 19.3% b} 21.4% 24.1% d) 26.7% e) None of the above Your portfolio is currently 100% Stock Z. Stock V (not listed Sharpe Ratio of 0.30. The correlation of Iwe stocks is 0.90. Based on this information, you should odd Stock V to your exiting portfolio Evaluate the underlined words in italics. True or False? a) True b) False les Which portfolio is most likely the optimal portfolio a) Portfolio 1 b) Portfolio 2 Portfolio 3 d) Portfolio 4 e) Portfolio 5 FO Which of the following statements is(are) most likely FALSE? If shorting were allowed, the Sharpe Ratio of the optimal portfolio might not improve IL To find the minimum variance portfolio, minimize the portfolio's total risk using Excel's solver III. Portfolio 6 is on the Minimum Variance Frontier d) I & II e) None of the statements This question is worth 2 points! Your client's current portfolio is $7,500 Stock Wand $2,500 Stock Z. Using the weights in the corner portfolios, which of the following actions (Hill) would most likely be required to maintain the same expected return for your client while lowering the portfolio's total riski Buy $6,750 Stock W IL Sell $1,000 Stock X III. Sell $2,500 Stock Z a) b) d) .) 1&H I & II wak Z. The derred retirements which oft Your client's current retirement account is $500,000 Stock Z. The client does not own any other financial assets and absolutely refuses to make any new contributions to their fax sheltered retirement account from now until retirement. The client also requires $1,000,000 when they retire in exactly 7 years. Which of the following would be the best recommendation to make to your client: a) Congratulations! Based on your current portfolio holdings, I expect you will be able to retire in 7 years with at least SIM of financial capital, so my recommendation for the time being is not to make any changes by Based on your current portfolio holdings, I do not expect you will be able to retire in 7 years with at least SIM of financial capital, so I recommend making additional contributions to your retirement account c) Based on your current portfolio holdings, I do not expect you will be able to retire with at least SIM of financial capital, so I recommend you wait a little longer to retire d) By diversifying your portfolio, I believe you will be able to retire in 7 years with at least SIM of financial capital without increasing your portfolio's total risk .) By diversifying your portfolio, I believe you will be able to retire in 7 years with at least SIM of financial capital, but your portfolio's total risk will have to increase

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts