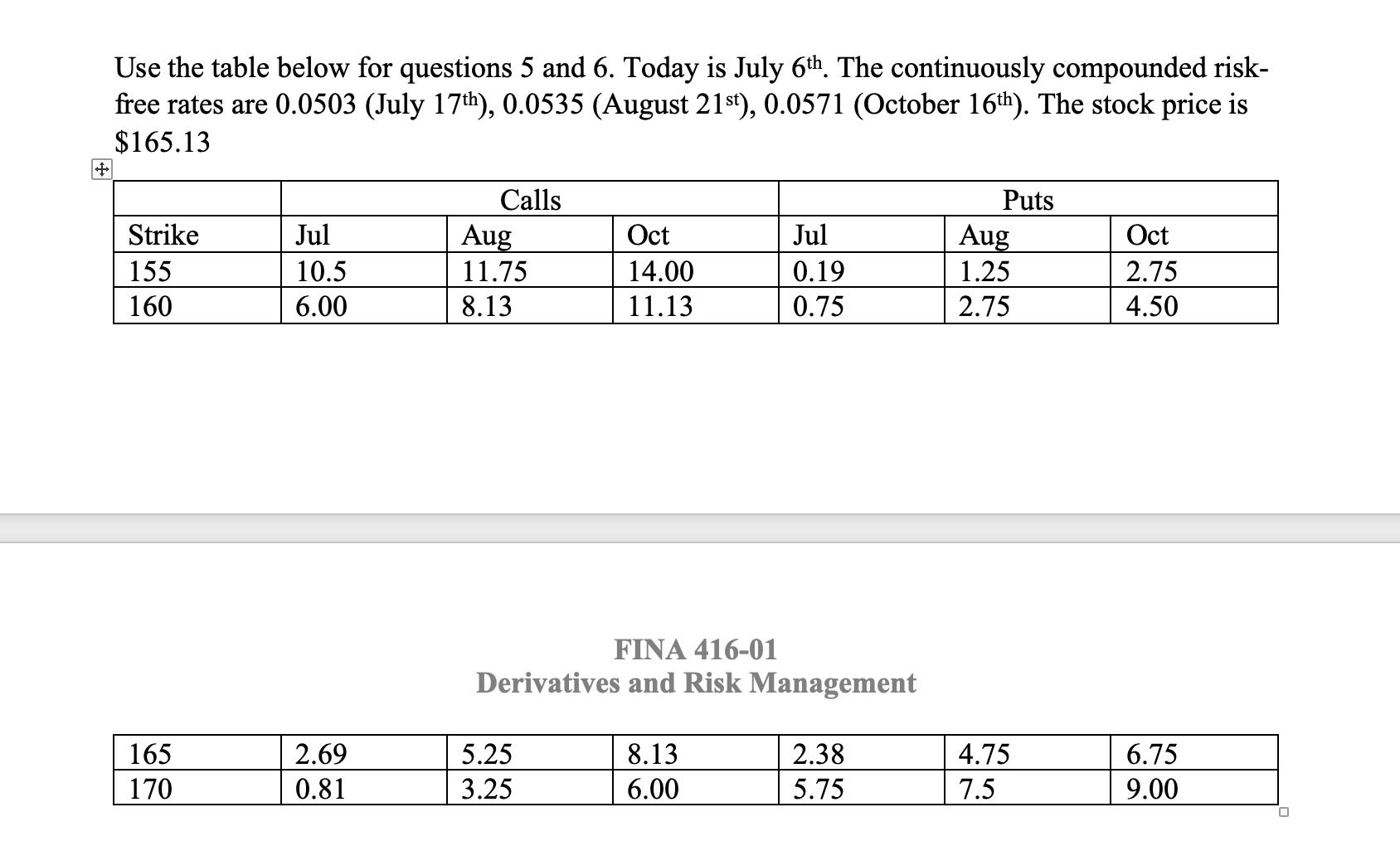

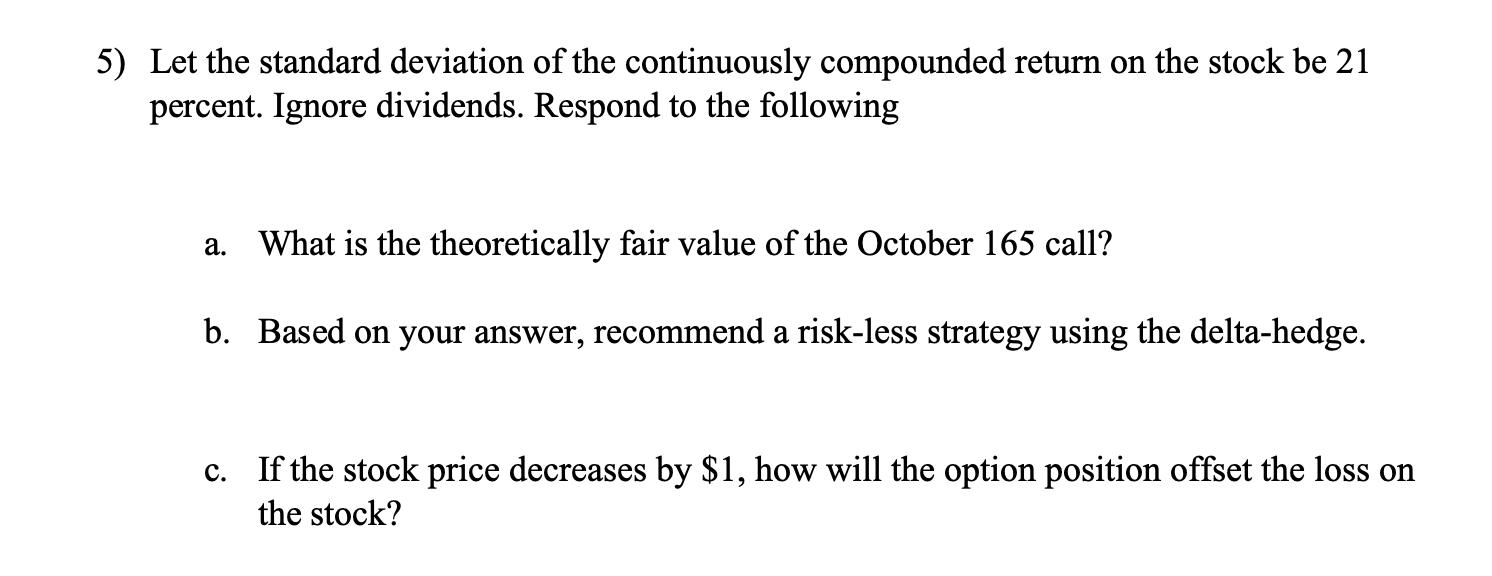

Question: + Use the table below for questions 5 and 6. Today is July 6th. The continuously compounded risk- free rates are 0.0503 (July 17th),

+ Use the table below for questions 5 and 6. Today is July 6th. The continuously compounded risk- free rates are 0.0503 (July 17th), 0.0535 (August 21st), 0.0571 (October 16th). The stock price is $165.13 Calls Puts Strike Jul Aug Oct Jul Aug Oct 155 10.5 11.75 14.00 0.19 1.25 2.75 160 6.00 8.13 11.13 0.75 2.75 4.50 FINA 416-01 Derivatives and Risk Management 165 2.69 5.25 8.13 2.38 4.75 6.75 170 0.81 3.25 6.00 5.75 7.5 9.00 5) Let the standard deviation of the continuously compounded return on the stock be 21 percent. Ignore dividends. Respond to the following a. What is the theoretically fair value of the October 165 call? b. Based on your answer, recommend a risk-less strategy using the delta-hedge. C. If the stock price decreases by $1, how will the option position offset the loss on the stock?

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts