Question: Using Excel. No data given Use the following information as your starting point. There are five notes and one bon Theoretical on-the-run Treasury yields for

Using Excel. No data given

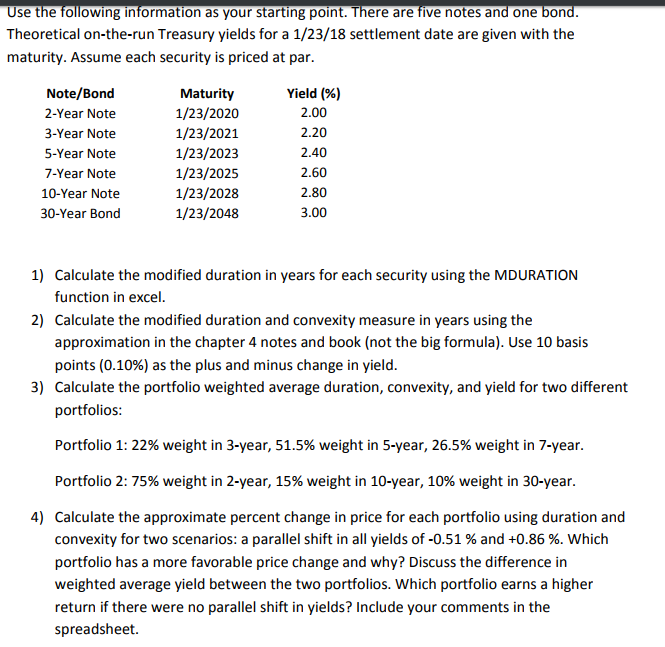

Use the following information as your starting point. There are five notes and one bon Theoretical on-the-run Treasury yields for a 1/23/18 settlement date are given with the maturity. Assume each security is priced at par Note/Bond 2-Year Note 3-Year Note 5-Year Note 7-Year Note 10-Year Note 30-Year Bond Maturity 1/23/2020 1/23/2021 1/23/2023 1/23/2025 1/23/2028 1/23/2048 Yield (%) 2.00 2.20 2.40 2.60 2.80 3.00 1) Calculate the modified duration in years for each security using the MDURATION function in excel 2) Calculate the modified duration and convexity measure in years using the approximation in the chapter 4 notes and book (not the big formula). Use 10 basis points (0.10%) as the plus and minus change in yield portfolios Portfolio 1: 22% weight in 3-year, 51.5% weight in 5-year, 26.5% weight in 7-year Portfolio 2: 75% weight in 2-year, 15% weight in 10-year, 10% weight in 30-year 3) Calculate the portfolio weighted average duration, convexity, and yield for two different 4) Calculate the approximate percent change in price for each portfolio using duration and convexity for two scenarios: a parallel shift in all yields of-0.51 % and +0.86 %. which portfolio has a more favorable price change and why? Discuss the difference in weighted average yield between the two portfolios. Which portfolio earns a higher return if there were no parallel shift in yields? Include your comments in the spreadsheet. Use the following information as your starting point. There are five notes and one bon Theoretical on-the-run Treasury yields for a 1/23/18 settlement date are given with the maturity. Assume each security is priced at par Note/Bond 2-Year Note 3-Year Note 5-Year Note 7-Year Note 10-Year Note 30-Year Bond Maturity 1/23/2020 1/23/2021 1/23/2023 1/23/2025 1/23/2028 1/23/2048 Yield (%) 2.00 2.20 2.40 2.60 2.80 3.00 1) Calculate the modified duration in years for each security using the MDURATION function in excel 2) Calculate the modified duration and convexity measure in years using the approximation in the chapter 4 notes and book (not the big formula). Use 10 basis points (0.10%) as the plus and minus change in yield portfolios Portfolio 1: 22% weight in 3-year, 51.5% weight in 5-year, 26.5% weight in 7-year Portfolio 2: 75% weight in 2-year, 15% weight in 10-year, 10% weight in 30-year 3) Calculate the portfolio weighted average duration, convexity, and yield for two different 4) Calculate the approximate percent change in price for each portfolio using duration and convexity for two scenarios: a parallel shift in all yields of-0.51 % and +0.86 %. which portfolio has a more favorable price change and why? Discuss the difference in weighted average yield between the two portfolios. Which portfolio earns a higher return if there were no parallel shift in yields? Include your comments in the spreadsheet

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts