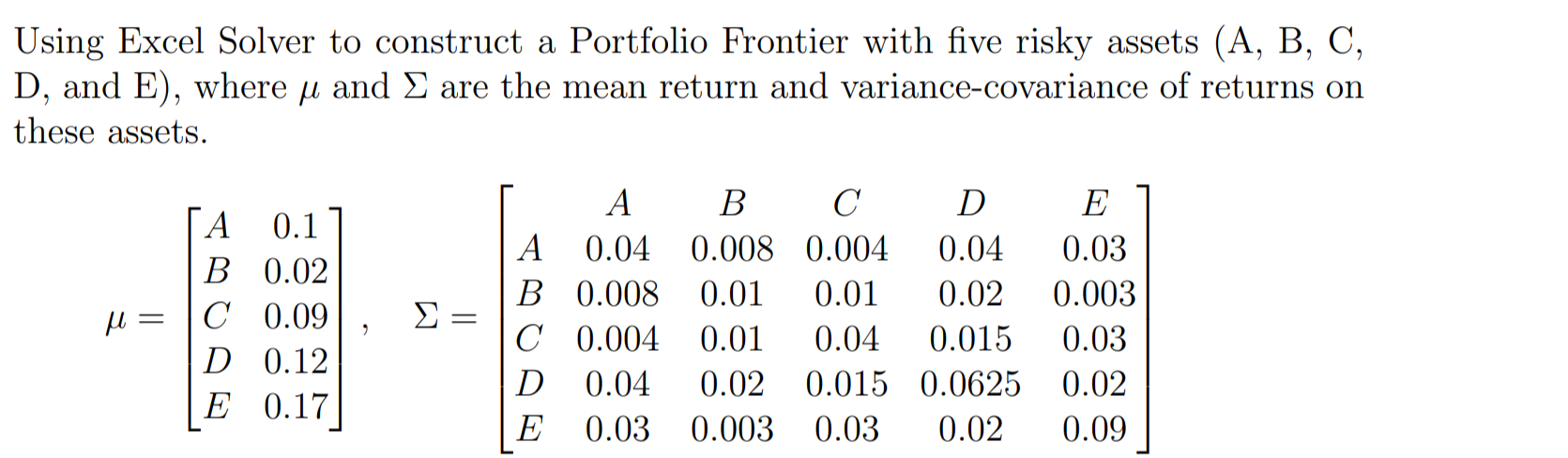

Question: Using Excel Solver to construct a Portfolio Frontier with five risky assets (A, B, C, D, and E), where u and are the mean return

Using Excel Solver to construct a Portfolio Frontier with five risky assets (A, B, C, D, and E), where u and are the mean return and variance-covariance of returns on these assets. u= CA 0.17 B 0.02 C 0.09, D 0.12 LE 0.17] A B C D E A B C D 0.04 0.008 0.004 0.04 0.008 0.01 0.01 0.02 0.004 0.01 0.04 0.015 0.04 0.02 0.015 0.0625 0.03 0.003 0.03 0.02 E 7 0.03 0.003 0.03 0.02 0.09 Using Excel Solver to construct a Portfolio Frontier with five risky assets (A, B, C, D, and E), where u and are the mean return and variance-covariance of returns on these assets. u= CA 0.17 B 0.02 C 0.09, D 0.12 LE 0.17] A B C D E A B C D 0.04 0.008 0.004 0.04 0.008 0.01 0.01 0.02 0.004 0.01 0.04 0.015 0.04 0.02 0.015 0.0625 0.03 0.003 0.03 0.02 E 7 0.03 0.003 0.03 0.02 0.09

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts