Question: Using python to answer the following questions 2.3 Exercise: Two Risky Assets We form a portfolio of two risky assets A and B with return

Using python to answer the following questions

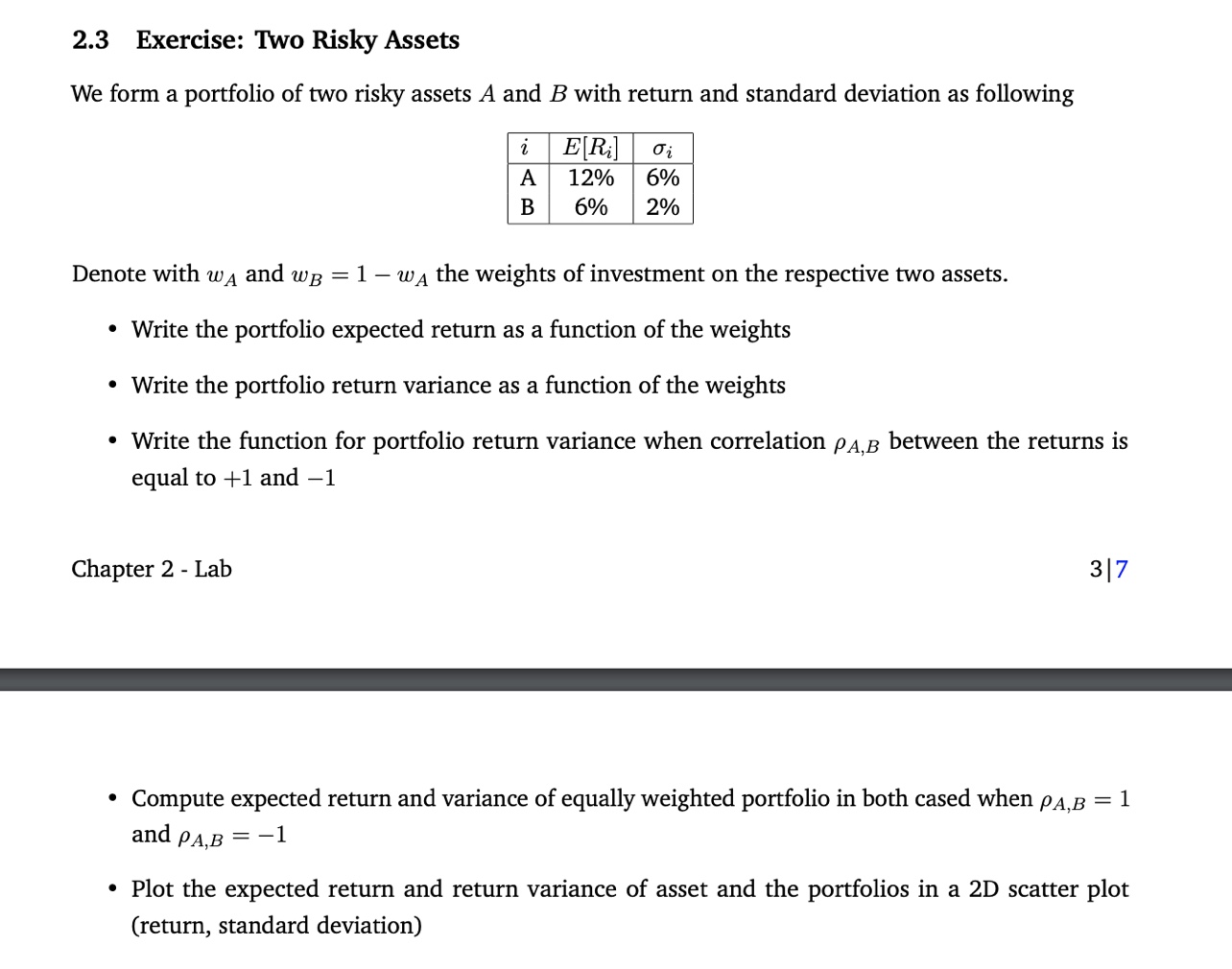

2.3 Exercise: Two Risky Assets We form a portfolio of two risky assets A and B with return and standard deviation as following Denote with wA and wB=1wA the weights of investment on the respective two assets. - Write the portfolio expected return as a function of the weights - Write the portfolio return variance as a function of the weights - Write the function for portfolio return variance when correlation A,B between the returns is equal to +1 and -1 Chapter 2 - Lab 37 - Compute expected return and variance of equally weighted portfolio in both cased when A,B=1 and A,B=1 - Plot the expected return and return variance of asset and the portfolios in a 2D scatter plot (return, standard deviation) 2.3 Exercise: Two Risky Assets We form a portfolio of two risky assets A and B with return and standard deviation as following Denote with wA and wB=1wA the weights of investment on the respective two assets. - Write the portfolio expected return as a function of the weights - Write the portfolio return variance as a function of the weights - Write the function for portfolio return variance when correlation A,B between the returns is equal to +1 and -1 Chapter 2 - Lab 37 - Compute expected return and variance of equally weighted portfolio in both cased when A,B=1 and A,B=1 - Plot the expected return and return variance of asset and the portfolios in a 2D scatter plot (return, standard deviation)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts