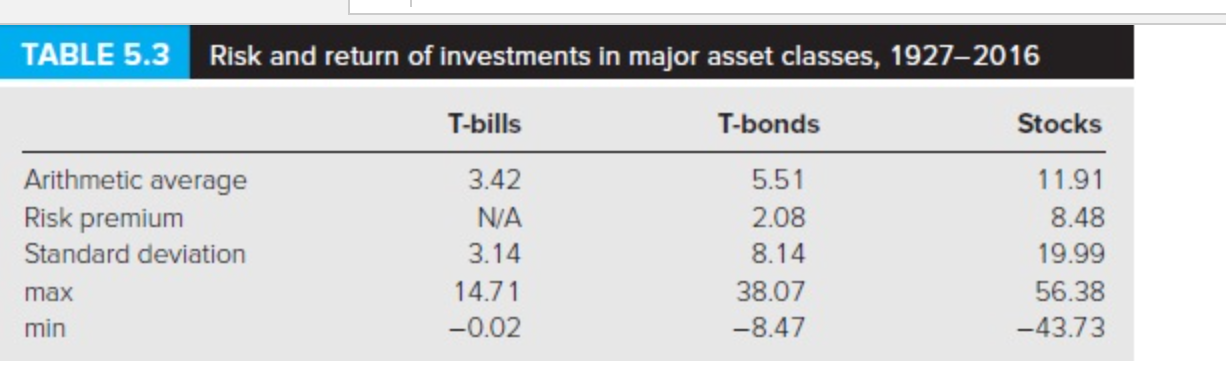

Question: Using Table 5.3 as your guide. (All returns in this problem are in annual term.) Estimate the Sharpe Ratio of the stock market portfolio and

Using Table 5.3 as your guide. (All returns in this problem are in annual term.) Estimate the Sharpe Ratio of the stock market portfolio and the Sharpe Ratio of the T-Bonds. Hints: Assume that market risk premium and market volatility are constant over time. The same for T-Bonds.

Market Sharpe Ratio =

T-Bond Sharpe Ratio =

TABLE 5.3 Risk and return of investments in major asset classes, 19272016 T-bills T-bonds Stocks Arithmetic average Risk premium Standard deviation max min 3.42 N/A 3.14 14.71 -0.02 5.51 2.08 8.14 38.07 -8.47 11.91 8.48 19.99 56.38 -43.73

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock