Question: Using the Excel template, set the term structure to be flat at 5%. On the First scenario tab, set the coupon to be 4% Calculate

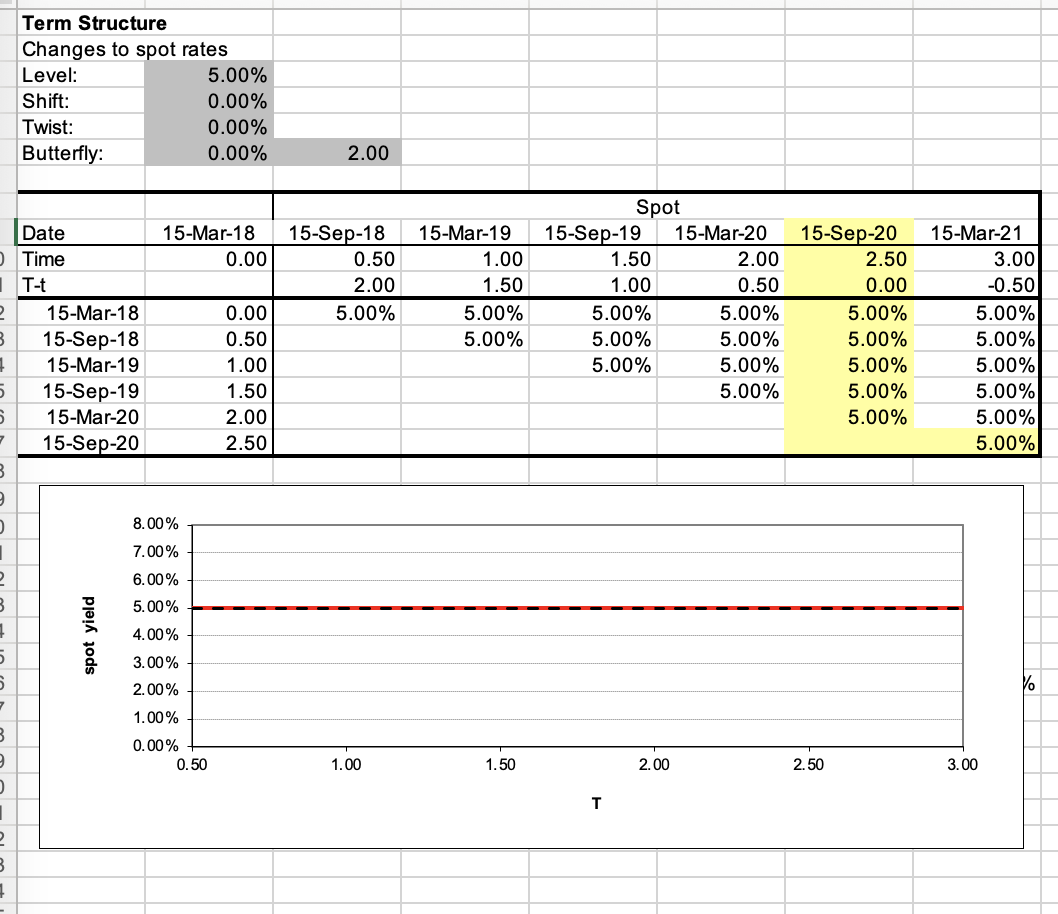

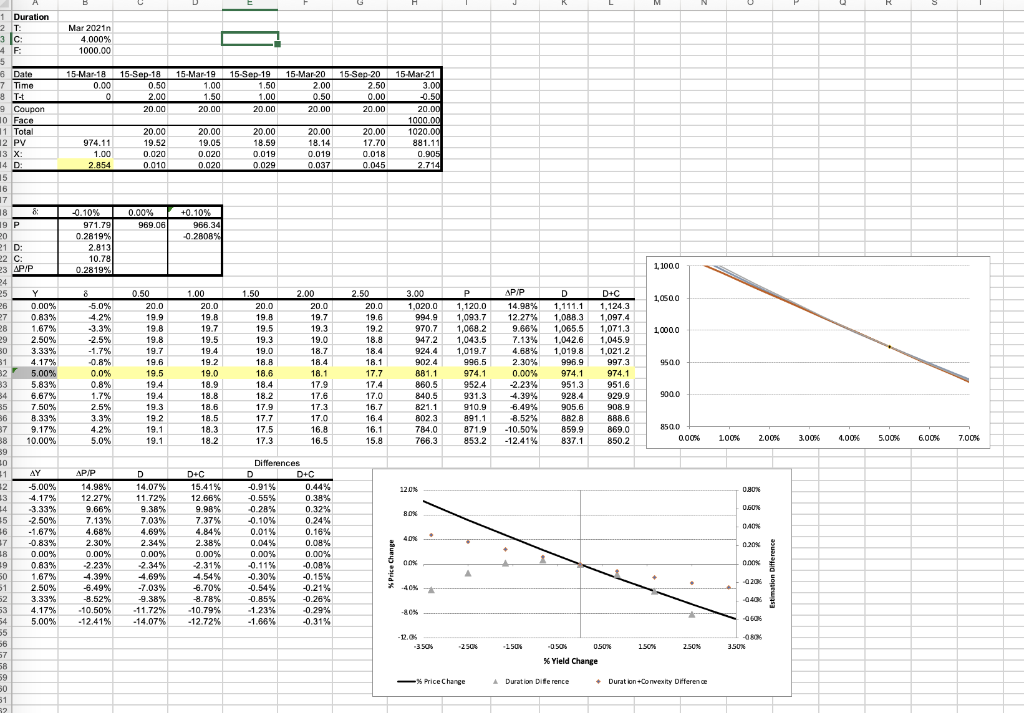

Using the Excel template, set the term structure to be flat at 5%. On the "First scenario" tab, set the coupon to be 4% Calculate and fill in the values for cells $B19:$D19. The 0.1% up and down moves are shifts of the whole term structure. What's the duration for this bond in this market environment? 2.813 Question 22 5 pt Same setup as #21. What is the convexity? 10.78 Term Structure Changes to spot rates Level: 5.00% Shift: 0.00% Twist: 0.00% Butterfly: 0.00% 2.00 15-Mar-18 0.00 15-Sep-18 0.50 2.00 5.00% 15-Mar-19 1.00 1.50 5.00% 5.00% Date Time IT-t 2 15-Mar-18 B 15-Sep-18 1 15-Mar-19 5 15-Sep-19 15-Mar-20 -7 15-Sep-20 B Spot 15-Sep-19 15-Mar-20 1.50 2.00 1.00 0.50 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 0.00 0.50 1.00 1.50 2.00 2.50 15-Sep-20 2.50 0.00 5.00% 5.00% 5.00% 5.00% 5.00% 15-Mar-21 3.00 -0.50 5.00% 5.00% 5.00% 5.00% 5.00% 5.00% 2 8.00% 7.00% 2 6.00% 5.00% B 1 5 5 spot yield 4.00% 3.00% 2.00% 1.00% VO B 9 0.00% 0.50 1.00 1.50 2.00 2.50 3.00 1 2 3 1 09 Nooo DO 1 DOWN99

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts