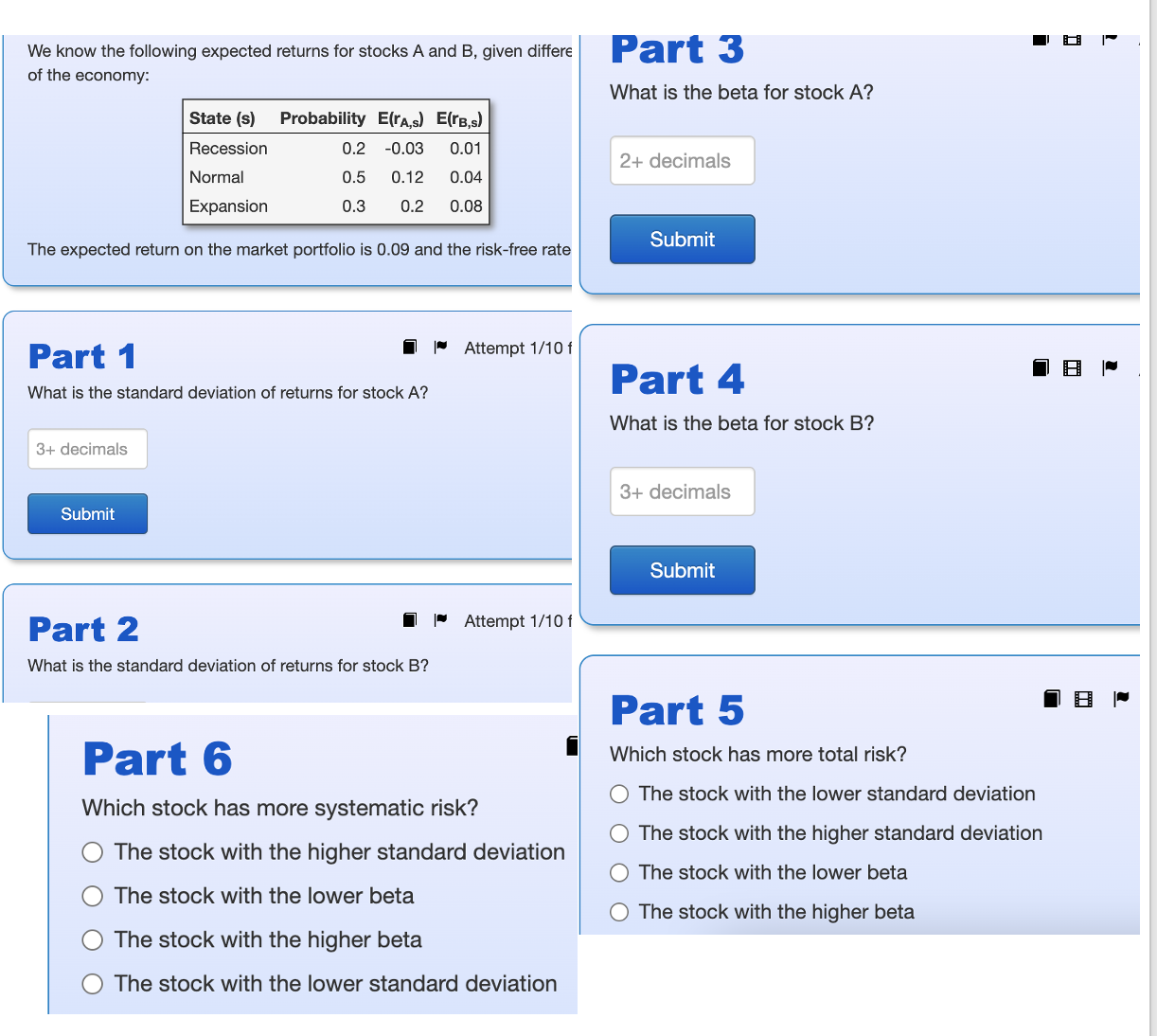

Question: We know the following expected returns for stocks A and B, given differ epsilon of the economy: State (s) Probability E(r_(A,s)) E(r_(B,s)) Recession 0.2 -0.03

We know the following expected returns for stocks A and B, given differ epsilon of the economy: State (s) Probability E(r_(A,s)) E(r_(B,s)) Recession 0.2 -0.03 0.01 Normal 0.5 0.12 0.04 Expansion 0.3 0.2 0.08 The expected return on the market portfolio is 0.09 and the risk-free rate Part 1 What is the standard deviation of returns for stock A ? Part 2 What is the standard deviation of returns for stock B? Part 6 Which stock has more systematic risk? The stock with the higher standard deviation The stock with the lower beta The stock with the higher beta The stock with the lower standard deviation Part 3 What is the beta for stock A ? Attempt 1//10 f Part

We know the following expected returns for stocks A and B, given differ of the economy: The expected return on the market portfolio is 0.09 and the risk-free rate Part 1 Attempt 1/10 f What is the standard deviation of returns for stock A? Part 2 Attempt 1/10 f What is the standard deviation of returns for stock B? Part 6 Which stock has more systematic risk? The stock with the higher standard deviation The stock with the lower beta The stock with the higher beta The stock with the lower standard deviation Part 3 What is the beta for stock A? Part 4 What is the beta for stock B ? Part 5 Which stock has more total risk? The stock with the lower standard deviation The stock with the higher standard deviation The stock with the lower beta The stock with the higher beta

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts