Question: we need to prove this equations! When we maximize the objective function, Sp, we have to satisfy the constraint that the portfolio weights sum to

we need to prove this equations!

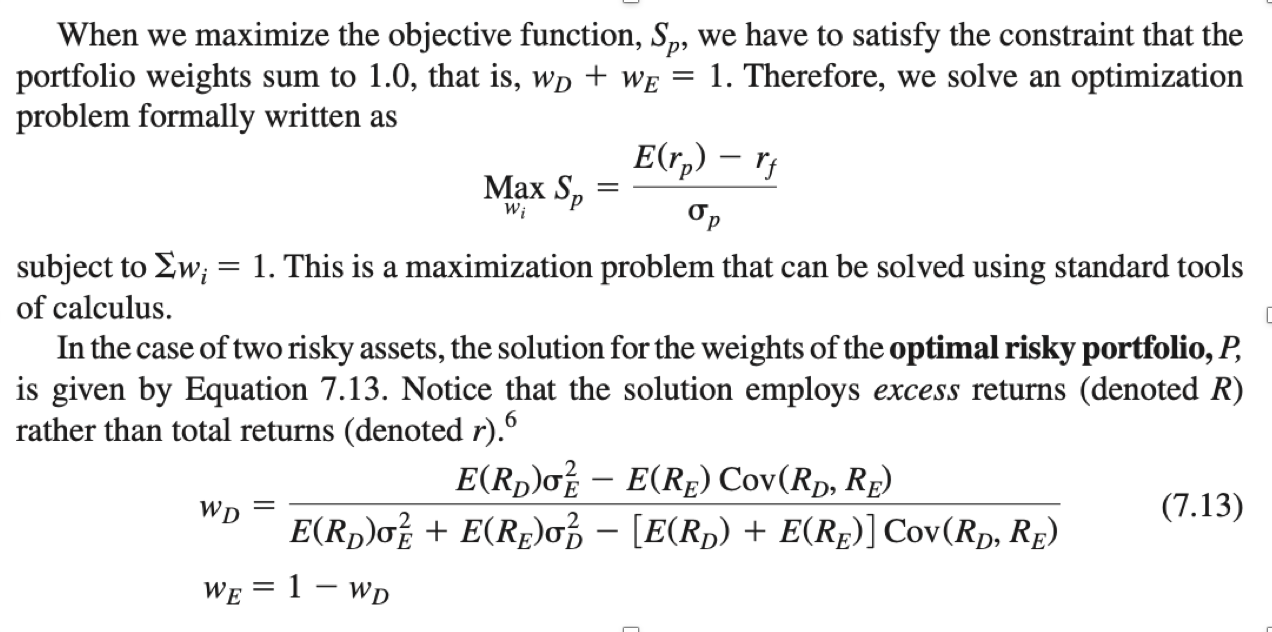

When we maximize the objective function, Sp, we have to satisfy the constraint that the portfolio weights sum to 1.0, that is, wd + We 1. Therefore, we solve an optimization problem formally written as E(rp) - 1 Max Sp Op subject to Ew; = 1. This is a maximization problem that can be solved using standard tools of calculus. In the case of two risky assets, the solution for the weights of the optimal risky portfolio, P, is given by Equation 7.13. Notice that the solution employs excess returns (denoted R) rather than total returns (denoted r). E(RD)O E(Re) Cov(Rp, Re) WD (7.13) E(Rp)o + E(Rp)o; - [E(Rp) + E(Re)] Cov(Rp, Re) We = 1 WD = When we maximize the objective function, Sp, we have to satisfy the constraint that the portfolio weights sum to 1.0, that is, wd + We 1. Therefore, we solve an optimization problem formally written as E(rp) - 1 Max Sp Op subject to Ew; = 1. This is a maximization problem that can be solved using standard tools of calculus. In the case of two risky assets, the solution for the weights of the optimal risky portfolio, P, is given by Equation 7.13. Notice that the solution employs excess returns (denoted R) rather than total returns (denoted r). E(RD)O E(Re) Cov(Rp, Re) WD (7.13) E(Rp)o + E(Rp)o; - [E(Rp) + E(Re)] Cov(Rp, Re) We = 1 WD =

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts