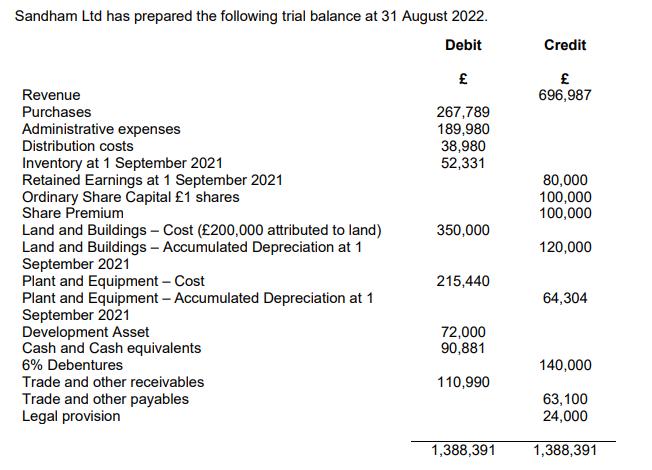

Prepare a statement of profit or loss and other comprehensive income, and a statement of changes in

Question:

- Prepare a statement of profit or loss and other comprehensive income, and a statement of changes in equity for Sandham for the year ended 31 August 2022 and a statement of financial position at 31 August 2022 in a form suitable for publication.

(Notes to the financial statements are not required, expenses should be presented analysed by function and ignore effects on tax of any adjustments.)

Additional information

1. Inventories as at 31 August 2022 had a cost of £43,770. Within this figure there are some defective items currently included at their cost of £14,000 can only be sold for £14,500 after incurring rectification costs of £2,250 and selling costs of £500.

2. On 13 February 2022 Sandham made a 1-for-2 bonus issue, using the share premium account. This has yet to be accounted for.

3. A dividend of 33p per ordinary share was paid on 30 June 2022 on the correct number of shares in issue at that date. This was incorrectly debited to purchases.

4. Sandham Ltd charges depreciation as follows: Buildings – straight line over 50 years charged to administrative expenses Plant and equipment – 20% per annum reducing balance charged to cost of sales

5. Within trade payables there is a balance in US$ of $25,000 relating to a purchase of goods that took place on 1 August 2022. This was correctly translated using a rate of $1.30/£1 on the date of purchase. The exchange rate on 31 August 2022 was $1.40/£1, no entries have been made to reflect this. Exchange differences are treated as admin expenses.

6. The provision relates to litigation from an employee claiming unfair dismissal, latest advice from company solicitors is settlement is expected to be £12,000. Expenses relating to the legal provision is expensed to Administrative expenses.

7. The current year’s interest has not been accrued for the loan note issued on a number of years ago which is repayable on 31 December 2024.

8. The Development asset relates to ongoing research and development into developing a new product. Work on this began 1 November 2021 but it wasn’t until 1 June 2022 that success of testing and intention to bring to market was confirmed. All costs accrued evenly. Any research is to be expensed to cost of sales.

9. The income tax charge for the year has been estimated as £80,450.

Expert Answer:

Financial Accounting and Reporting

ISBN: 978-1292162409

18th edition

Authors: Barry Elliott, Jamie Elliott