Wilson Manufacturing Company Wilson Manufacturing (the Company), an SEC registrant with a calendar year-end (December 31), is

Question:

Wilson Manufacturing Company Wilson Manufacturing (the “Company”), an SEC registrant with a calendar year-end (December 31), is a manufacturer and distributor of fitness equipment. The company was created in 1989 and is headquartered in Southern California. The Company has manufacturing operations and numerous sales and administrative locations in the United States. Wilson files a consolidated U.S. federal tax return. (This case will not consider the evaluation of the state jurisdictions; it will only consider the federal jurisdiction.)

As Wilson’s auditors, you are now performing the Company’s year-end audit for the fiscal year ended December 31, 2018, and have the following information available to you:

• The Tax Cuts and Jobs Act (the “Act”) was enacted in the United States on December 22, 2017, and was accounted for accordingly by Wilson Manufacturing.

• The Act changed the rules related to tax loss carryforwards such that tax loss carryforwards arising in years after 2017 have an unlimited carryforward period though they may only be used to offset 80% of taxable income in a given year. Further, the Act removed the carryback period that had previously been allowed.

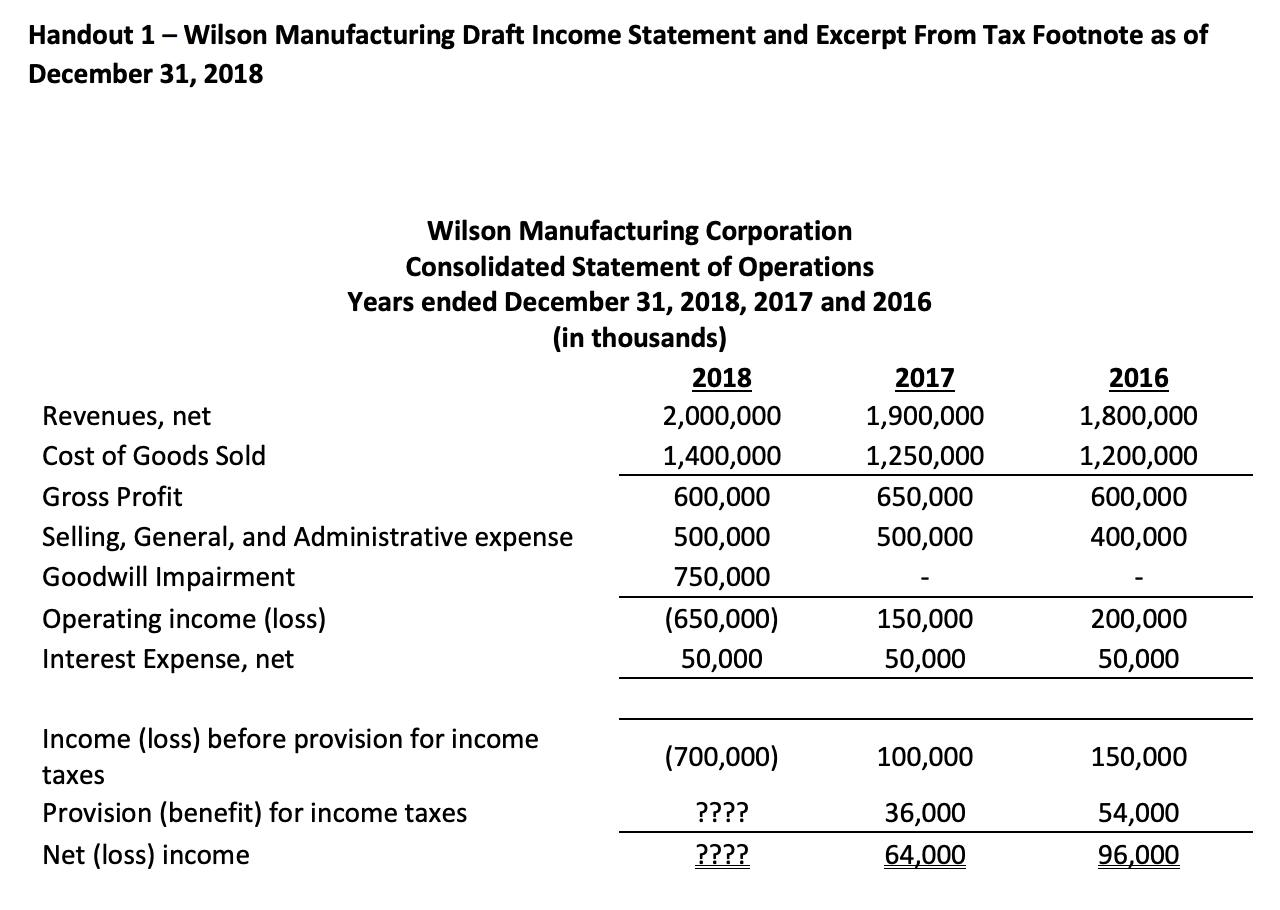

• Wilson Manufacturing draft income statement and excerpt from tax footnote as of December 31, 2018 (Handout 1).

• The tax loss carryforwards detailed in Handout 1 arose before 2018.

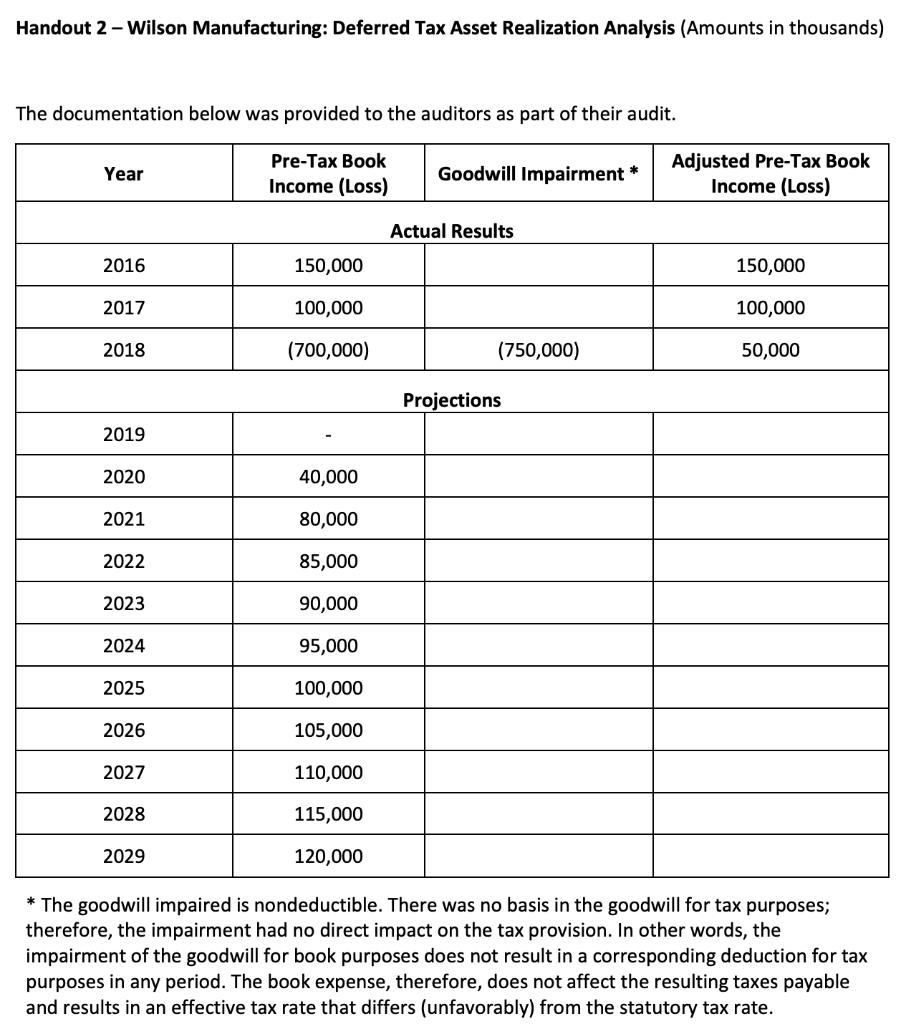

• A deferred tax asset realization analysis showing pre-tax book income projections (Handout 2).

• Management’s pre-tax income forecast considerations (Handouts 2 & 3)

• The projected income schedule (realization analysis above) projects organic growth beginning in 2020 after stemming the decrease in pre-tax book income.

• The nondeductible goodwill impairment charge is a permanent item.

• Wilson does not have the ability to carry back any losses to prior periods.

• A significant customer declared bankruptcy in 2018; therefore, the Company wrote off all accounts receivable from this customer. The Company is considering the exclusion of such expense when evaluating whether future income is objectively verifiable.

• The Company does not have a history of operating losses or tax credit carryforwards expiring unused.

• The Company has identified the following possible tax-planning strategies:

Selling and leasing back manufacturing equipment that would result in a taxable gain of $20 million.

Selling the primary manufacturing facility at a gain to offset existing capital loss carryforwards.

Required

• Question 2 — How much of the reversing taxable temporary differences may be considered in estimating future taxable income? Assume the net operating losses (NOL’s) arose in 2018.

Expert Answer:

ANSWER A yearend audit is a financial review of businesses that analyzes their books records and acc... View the full answer

Intermediate Accounting Reporting and Analysis

ISBN: 978-1285453828

2nd edition

Authors: James M. Wahlen, Jefferson P. Jones, Donald Pagach