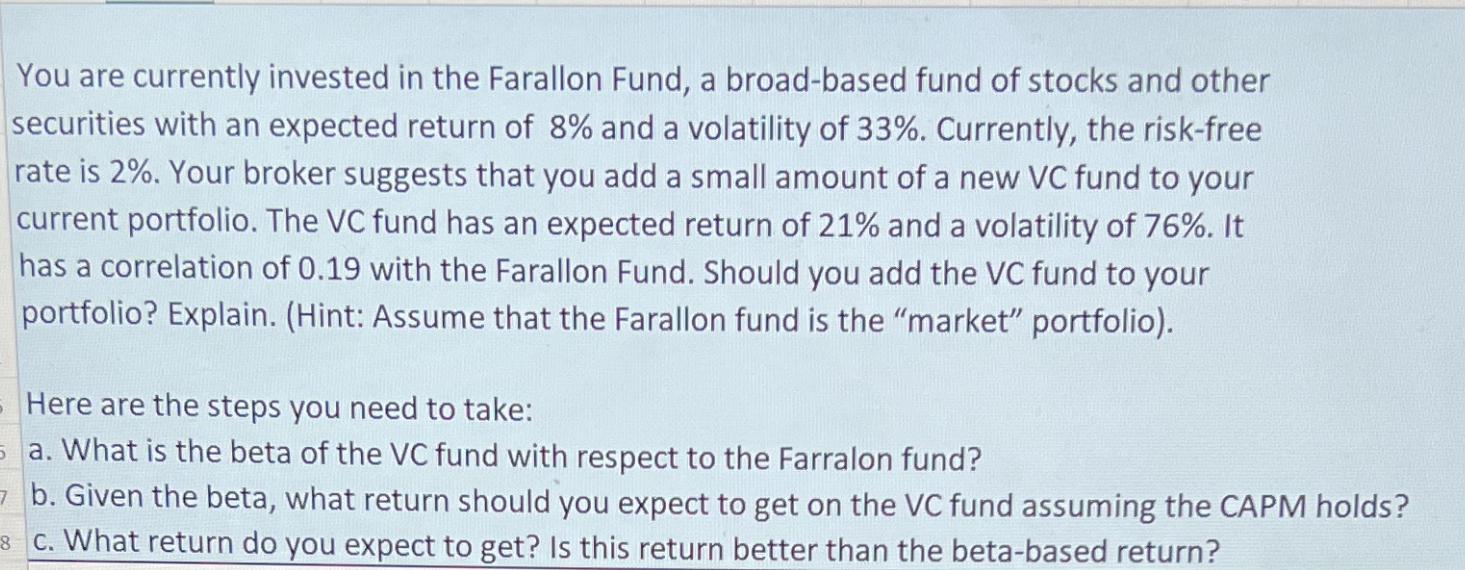

You are currently invested in the Farallon Fund, a broad-based fund of stocks and other securities...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a To find the beta of the VC fund with respect to the Farallon fund we can use the following formula BetaVC CovFarallon VC VarFarallon where CovFarallon VC is the covariance between the Farallon fund ... View the full answer

Related Book For

Posted Date: