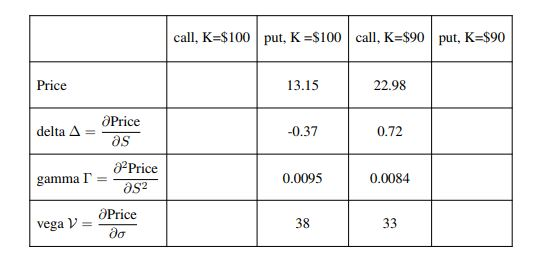

Question: You are given the data in the table below regarding the price and sensitivity of 4 European options with maturity in one year (T =

You are given the data in the table below regarding the price and sensitivity of 4 European options with maturity in one year (T = 1). For the sensitivities, S is the price of the underlying and ? is its volatility. We also know that the underlying asset for all the options is a non-dividend-paying stock whose current share price is $100. The continuously compounded risk free rate is 5% per year.

(a) Fill in the missing values in the table above, indicating any formula you use. Hint: Note that the market model is NOT necessarily the Black-Scholes market.

(b) Suppose you currently are long two puts with K = 100 and short one put with K = 90. Compute the delta, gamma and vega of your current portfolio.

(c) If you were to increase your estimate of the stock volatility by 1%, by approximately how much would you revise the call and put prices with K=100?

call, K-$100put, K-S100 call, K-S90put, K-$90 Price 13.15 22.98 Price on delta ? 0.37 0.72 Price gamma? 0.0095 0.0084 Price vega V- 38

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts