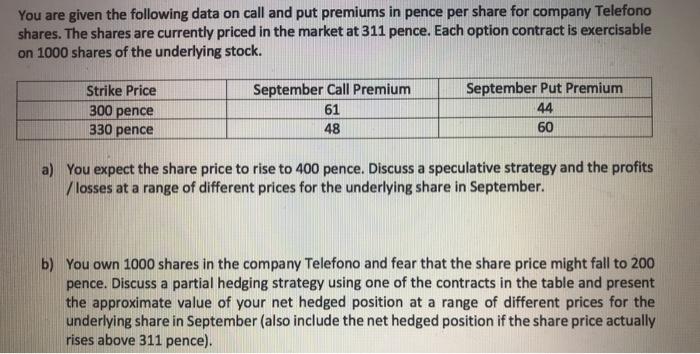

Question: You are given the following data on call and put premiums in pence per share for company Telefono shares. The shares are currently priced in

You are given the following data on call and put premiums in pence per share for company Telefono shares. The shares are currently priced in the market at 311 pence. Each option contract is exercisable on 1000 shares of the underlying stock. Strike Price 300 pence 330 pence September Call Premium 61 48 September Put Premium 44 60 a) You expect the share price to rise to 400 pence. Discuss a speculative strategy and the profits losses at a range of different prices for the underlying share in September. b) You own 1000 shares in the company Telefono and fear that the share price might fall to 200 pence. Discuss a partial hedging strategy using one of the contracts in the table and present the approximate value of your net hedged position at a range of different prices for the underlying share in September (also include the net hedged position if the share price actually rises above 311 pence)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts