You are the auditor-in-charge of the Spidey Ltd group of companies, a JSE Ltd listed South...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

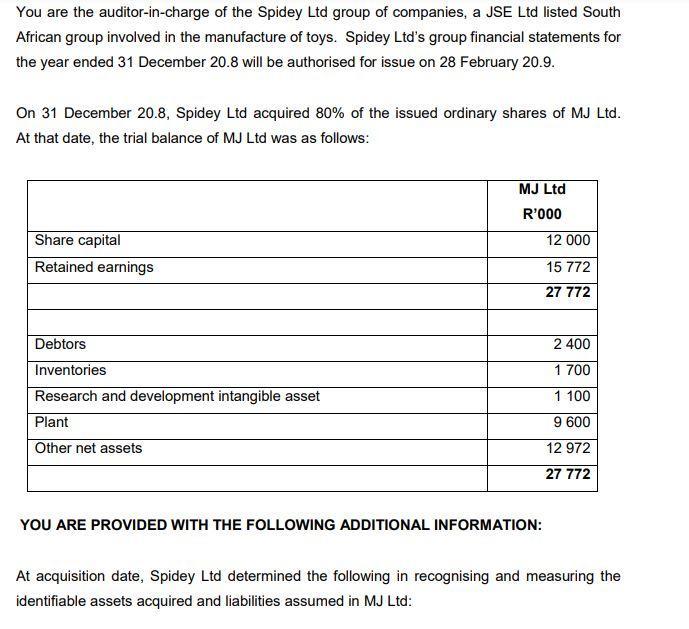

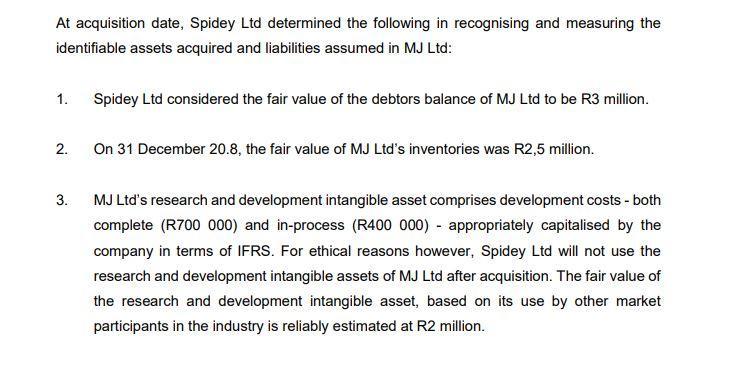

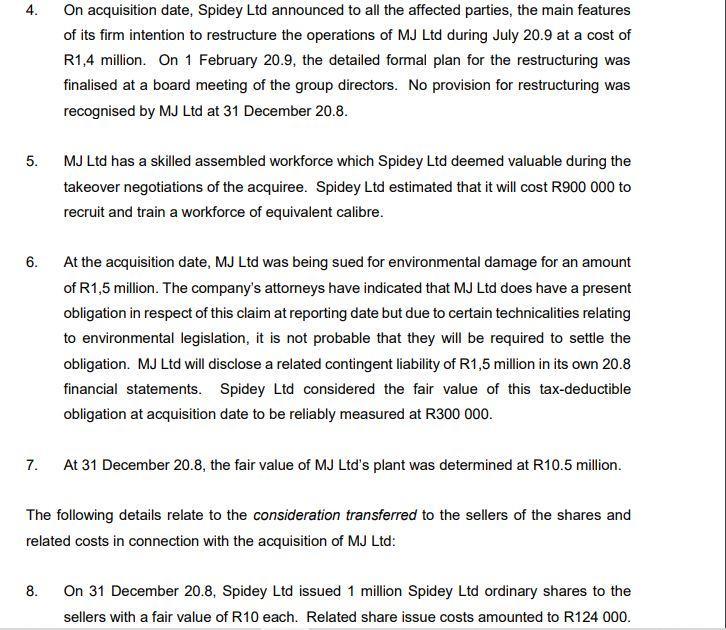

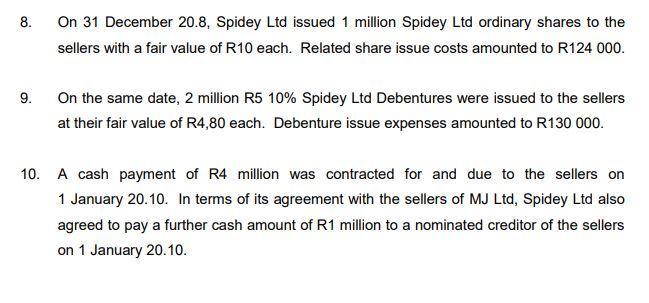

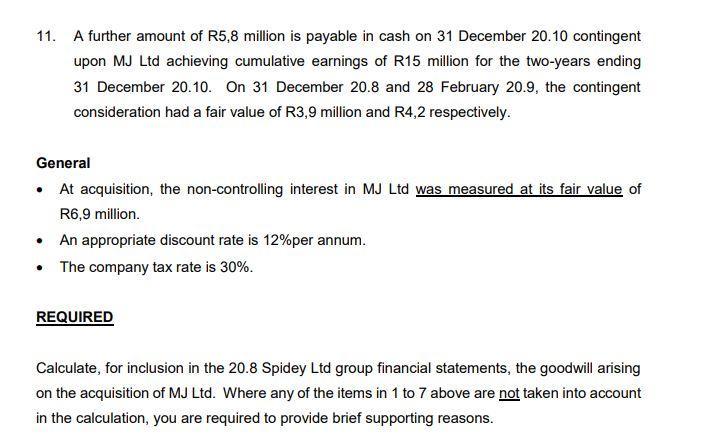

You are the auditor-in-charge of the Spidey Ltd group of companies, a JSE Ltd listed South African group involved in the manufacture of toys. Spidey Ltd's group financial statements for the year ended 31 December 20.8 will be authorised for issue on 28 February 20.9. On 31 December 20.8, Spidey Ltd acquired 80% of the issued ordinary shares of MJ Ltd. At that date, the trial balance of MJ Ltd was as follows: Share capital Retained earnings Debtors Inventories Research and development intangible asset Plant Other net assets MJ Ltd R'000 YOU ARE PROVIDED WITH THE FOLLOWING ADDITIONAL INFORMATION: 12 000 15 772 27 772 2 400 1 700 1 100 9 600 12 972 27 772 At acquisition date, Spidey Ltd determined the following in recognising and measuring the identifiable assets acquired and liabilities assumed in MJ Ltd: At acquisition date, Spidey Ltd determined the following in recognising and measuring the identifiable assets acquired and liabilities assumed in MJ Ltd: 1. 2. 3. Spidey Ltd considered the fair value of the debtors balance of MJ Ltd to be R3 million. On 31 December 20.8, the fair value of MJ Ltd's inventories was R2,5 million. MJ Ltd's research and development intangible asset comprises development costs - both complete (R700 000) and in-process (R400 000) appropriately capitalised by the company in terms of IFRS. For ethical reasons however, Spidey Ltd will not use the research and development intangible assets of MJ Ltd after acquisition. The fair value of the research and development intangible asset, based on its use by other market participants in the industry is reliably estimated at R2 million. 4. 5. 6. On acquisition date, Spidey Ltd announced to all the affected parties, the main features of its firm intention to restructure the operations of MJ Ltd during July 20.9 at a cost of R1,4 million. On 1 February 20.9, the detailed formal plan for the restructuring was finalised at a board meeting of the group directors. No provision for restructuring was recognised by MJ Ltd at 31 December 20.8. MJ Ltd has a skilled assembled workforce which Spidey Ltd deemed valuable during the takeover negotiations of the acquiree. Spidey Ltd estimated that it will cost R900 000 to recruit and train a workforce of equivalent calibre. 8. At the acquisition date, MJ Ltd was being sued for environmental damage for an amount of R1,5 million. The company's attorneys have indicated that MJ Ltd does have a present obligation in respect of this claim at reporting date but due to certain technicalities relating to environmental legislation, it is not probable that they will be required to settle the obligation. MJ Ltd will disclose a related contingent liability of R1,5 million in its own 20.8 financial statements. Spidey Ltd considered the fair value of this tax-deductible obligation at acquisition date to be reliably measured at R300 000. 7. At 31 December 20.8, the fair value of MJ Ltd's plant was determined at R10.5 million. The following details relate to the consideration transferred to the sellers of the shares and related costs in connection with the acquisition of MJ Ltd: On 31 December 20.8, Spidey Ltd issued 1 million Spidey Ltd ordinary shares to the sellers with a fair value of R10 each. Related share issue costs amounted to R124 000. 8. 9. On 31 December 20.8, Spidey Ltd issued 1 million Spidey Ltd ordinary shares to the sellers with a fair value of R10 each. Related share issue costs amounted to R124 000. On the same date, 2 million R5 10% Spidey Ltd Debentures were issued to the sellers at their fair value of R4,80 each. Debenture issue expenses amounted to R130 000. 10. A cash payment of R4 million was contracted for and due to the sellers on 1 January 20.10. In terms of its agreement with the sellers of MJ Ltd, Spidey Ltd also agreed to pay a further cash amount of R1 million to a nominated creditor of the sellers on 1 January 20.10. 11. A further amount of R5,8 million is payable in cash on 31 December 20.10 contingent upon MJ Ltd achieving cumulative earnings of R15 million for the two-years ending 31 December 20.10. On 31 December 20.8 and 28 February 20.9, the contingent consideration had a fair value of R3,9 million and R4,2 respectively. General • At acquisition, the non-controlling interest in MJ Ltd was measured at its fair value of R6,9 million. • An appropriate discount rate is 12% per annum. The company tax rate is 30%. REQUIRED Calculate, for inclusion in the 20.8 Spidey Ltd group financial statements, the goodwill arising on the acquisition of MJ Ltd. Where any of the items in 1 to 7 above are not taken into account in the calculation, you are required to provide brief supporting reasons. You are the auditor-in-charge of the Spidey Ltd group of companies, a JSE Ltd listed South African group involved in the manufacture of toys. Spidey Ltd's group financial statements for the year ended 31 December 20.8 will be authorised for issue on 28 February 20.9. On 31 December 20.8, Spidey Ltd acquired 80% of the issued ordinary shares of MJ Ltd. At that date, the trial balance of MJ Ltd was as follows: Share capital Retained earnings Debtors Inventories Research and development intangible asset Plant Other net assets MJ Ltd R'000 YOU ARE PROVIDED WITH THE FOLLOWING ADDITIONAL INFORMATION: 12 000 15 772 27 772 2 400 1 700 1 100 9 600 12 972 27 772 At acquisition date, Spidey Ltd determined the following in recognising and measuring the identifiable assets acquired and liabilities assumed in MJ Ltd: At acquisition date, Spidey Ltd determined the following in recognising and measuring the identifiable assets acquired and liabilities assumed in MJ Ltd: 1. 2. 3. Spidey Ltd considered the fair value of the debtors balance of MJ Ltd to be R3 million. On 31 December 20.8, the fair value of MJ Ltd's inventories was R2,5 million. MJ Ltd's research and development intangible asset comprises development costs - both complete (R700 000) and in-process (R400 000) appropriately capitalised by the company in terms of IFRS. For ethical reasons however, Spidey Ltd will not use the research and development intangible assets of MJ Ltd after acquisition. The fair value of the research and development intangible asset, based on its use by other market participants in the industry is reliably estimated at R2 million. 4. 5. 6. On acquisition date, Spidey Ltd announced to all the affected parties, the main features of its firm intention to restructure the operations of MJ Ltd during July 20.9 at a cost of R1,4 million. On 1 February 20.9, the detailed formal plan for the restructuring was finalised at a board meeting of the group directors. No provision for restructuring was recognised by MJ Ltd at 31 December 20.8. MJ Ltd has a skilled assembled workforce which Spidey Ltd deemed valuable during the takeover negotiations of the acquiree. Spidey Ltd estimated that it will cost R900 000 to recruit and train a workforce of equivalent calibre. 8. At the acquisition date, MJ Ltd was being sued for environmental damage for an amount of R1,5 million. The company's attorneys have indicated that MJ Ltd does have a present obligation in respect of this claim at reporting date but due to certain technicalities relating to environmental legislation, it is not probable that they will be required to settle the obligation. MJ Ltd will disclose a related contingent liability of R1,5 million in its own 20.8 financial statements. Spidey Ltd considered the fair value of this tax-deductible obligation at acquisition date to be reliably measured at R300 000. 7. At 31 December 20.8, the fair value of MJ Ltd's plant was determined at R10.5 million. The following details relate to the consideration transferred to the sellers of the shares and related costs in connection with the acquisition of MJ Ltd: On 31 December 20.8, Spidey Ltd issued 1 million Spidey Ltd ordinary shares to the sellers with a fair value of R10 each. Related share issue costs amounted to R124 000. 8. 9. On 31 December 20.8, Spidey Ltd issued 1 million Spidey Ltd ordinary shares to the sellers with a fair value of R10 each. Related share issue costs amounted to R124 000. On the same date, 2 million R5 10% Spidey Ltd Debentures were issued to the sellers at their fair value of R4,80 each. Debenture issue expenses amounted to R130 000. 10. A cash payment of R4 million was contracted for and due to the sellers on 1 January 20.10. In terms of its agreement with the sellers of MJ Ltd, Spidey Ltd also agreed to pay a further cash amount of R1 million to a nominated creditor of the sellers on 1 January 20.10. 11. A further amount of R5,8 million is payable in cash on 31 December 20.10 contingent upon MJ Ltd achieving cumulative earnings of R15 million for the two-years ending 31 December 20.10. On 31 December 20.8 and 28 February 20.9, the contingent consideration had a fair value of R3,9 million and R4,2 respectively. General • At acquisition, the non-controlling interest in MJ Ltd was measured at its fair value of R6,9 million. • An appropriate discount rate is 12% per annum. The company tax rate is 30%. REQUIRED Calculate, for inclusion in the 20.8 Spidey Ltd group financial statements, the goodwill arising on the acquisition of MJ Ltd. Where any of the items in 1 to 7 above are not taken into account in the calculation, you are required to provide brief supporting reasons.

Expert Answer:

Answer rating: 100% (QA)

Answer Goodwill on Acquisition of MJ Ltd Goodwill is a premium paid for an acquisition above the fair value of the net identifiable assets acquired Th... View the full answer

Posted Date:

Students also viewed these accounting questions

-

The summarized statements for the year ended 31 December 2007 for Mat, Rug and P entities are as follows: Statements of comprehensive income for the year ended 31 December 2007 The following...

-

The auditor is auditing financial statements for the year ended December 31, 2011, and is completing the audit in early March 2012. The following situations have come to the auditor's attention: 1....

-

The income statements for the year ended 31 December 2020 and the statements of financial position as at 31 December 2020 for Garden Plc, Leaf Ltd and Flower Ltd are given as follows: Statements of...

-

In Exercises 3542, describe and sketch the surface given by the function. f(x, y) = Jxy, 0, x 0, y 0 x <0 or y < 0

-

Consider the Wyndor Glass Co. problem described in Sec. 3.1 (see Table 3.1). Suppose that decisions have been made to discontinue additional products in the future and to initiate other new products....

-

Calculating OCF Consider the following income statement: Fill in the missing numbers and then calculate the OCF. What is the depreciation tax shield? Sales S876,400 Costs 547,300 128,000 Depreciation...

-

Over the course of about six years, Hanwha Corp., a Korean company, entered into 20 separate contracts to purchase petrochemicals from Cedar Petrochemicals, Inc. While negotiating for the...

-

McClain Plastics has been an audit client of Belcor, Rich, Smith & Barnes, CPAs (BRS&B), for several years. McClain Plastics was started by Evers McClain, who owns 51% of the companys stock. The...

-

1 Explain briefly about six sigma and capacity maturity models? 2 Explain about the contemporary management practices taking place in Indian business model? 3 4 What is performance management?...

-

Jackie serves as the vice president for network development for a large, midwestern healthcare system. She has worked with many rural and semirural hospitals to improve efficiency by offering shared...

-

For a step-down DC/DC converter, consider all componenets to be ideal. Assume V-5V, fs-20kHz, L=1mH, and C=450uF. If Vd=12.6V, and Io=200mA, 1) draw the step-down converter 2) calculate...

-

How did the United States shift from a nation of agrarian farmers to an industrial powerhouse during the late 19th and early 20th centuries?

-

Wayne Company is located at 99 Fifth Avenue New York City, NY, 10001. The company is a general partnership using the calendar year and accrual basis for both book and tax purposes. It engages in the...

-

What is the difference between a stack and a queue data structure?

-

Social skill is important in the service industry. As a future tourism and hospitality professional, how are you going to improve your social skills? Another key component of emotional intelligence...

-

Imperial Jewelers manufactures and sells a gold bracelet for $404.00. The company's accounting system says that the unit product cost for this bracelet is $267.00 as shown below: Direct materials...

-

Question 11 (1 point) C1 Let the sample data be: 1 WNHWN HWNY 2 3 1 2 3 1 2 3 C2 3 m anh qu nhanh - 2 1 3 2 1 3 2 1 c3 111NNN 3 3 3 2 2 2 O 1011TTTOO P (C1=1, C2 = 2, C3=3 | O = 0) = ? P(C1=1 | 0 =...

-

By referring to Figure 13.18, determine the mass of each of the following salts required to form a saturated solution in 250 g of water at 30 oC: (a) KClO3, (b) Pb(NO3)2, (c) Ce2(SO4)3.

-

Which of the following is not a characteristic of common equity? A. It represents an ownership interest in the company. B. Shareholders participate in the decision-making process. C. The company is...

-

Investing the majority of the portfolio on a passive or low active risk basis while a minority of the assets is managed aggressively in smaller portfolios is best described as: A. The coresatellite...

-

All of the following are characteristics of preference shares except: A. They are either callable or putable. B. They generally do not have voting rights. C. They do not share in the operating...

Study smarter with the SolutionInn App