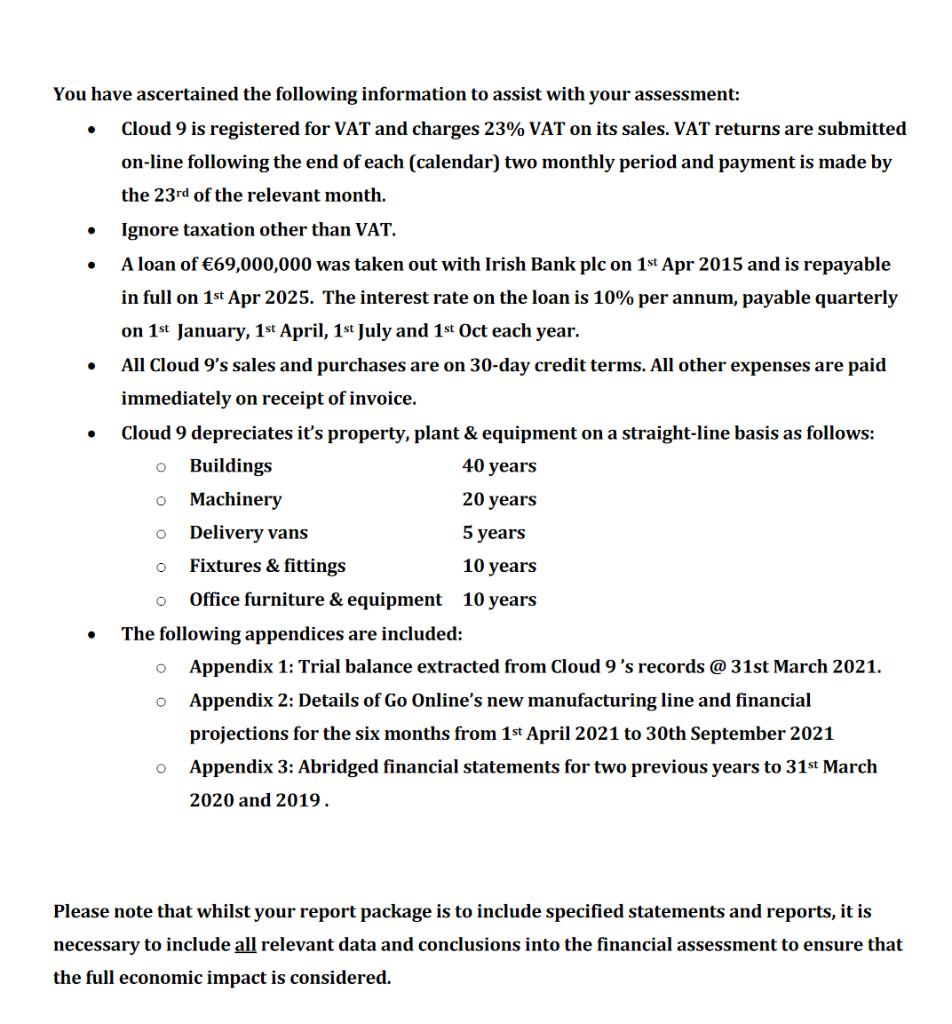

You have ascertained the following information to assist with your assessment: Cloud 9 is registered for...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

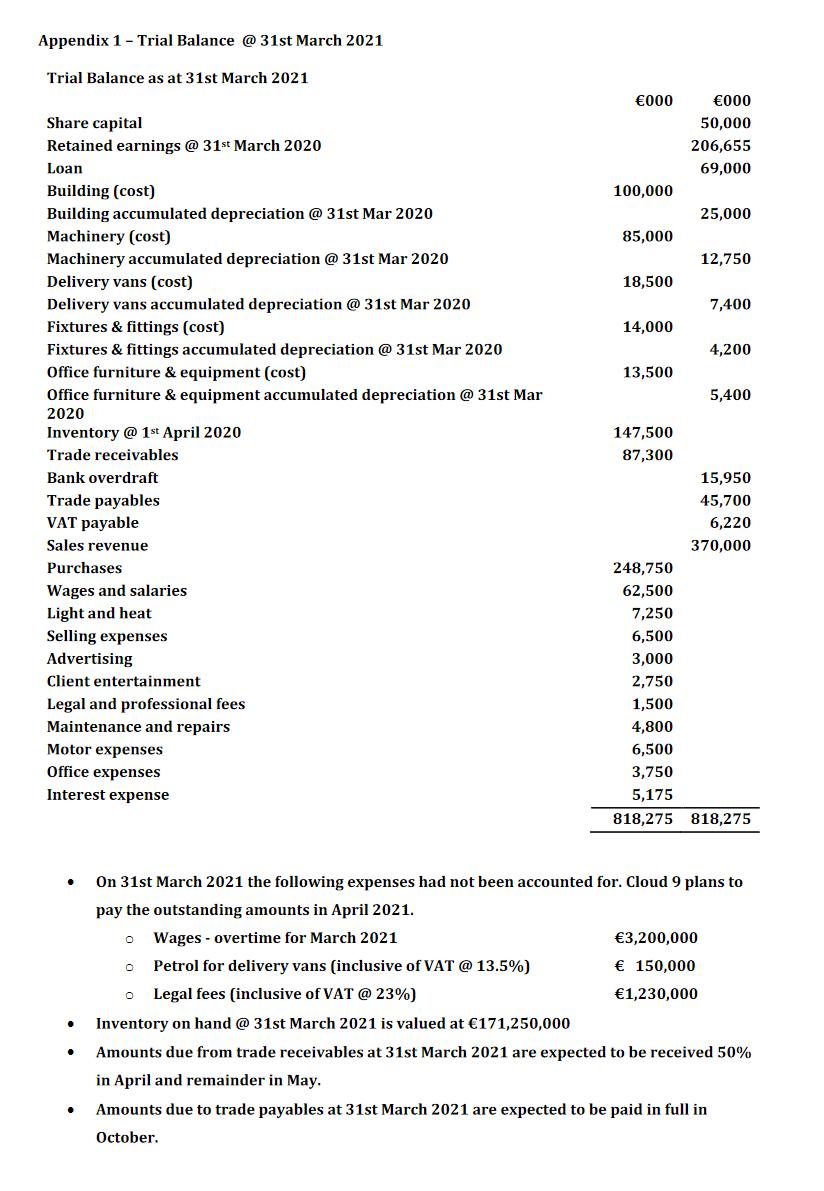

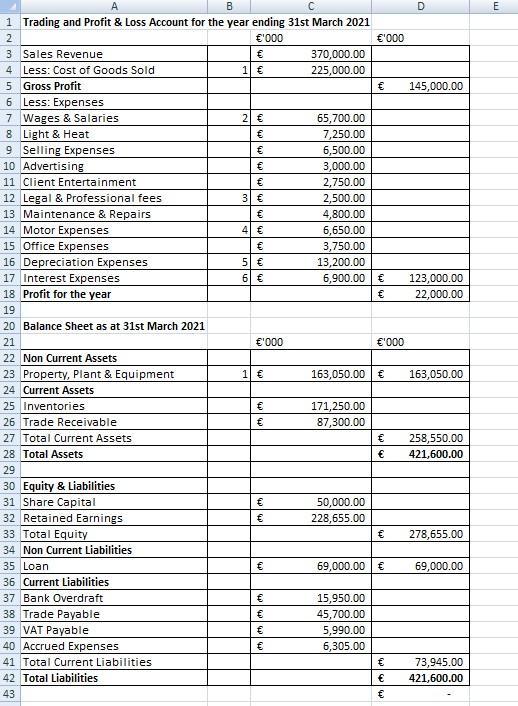

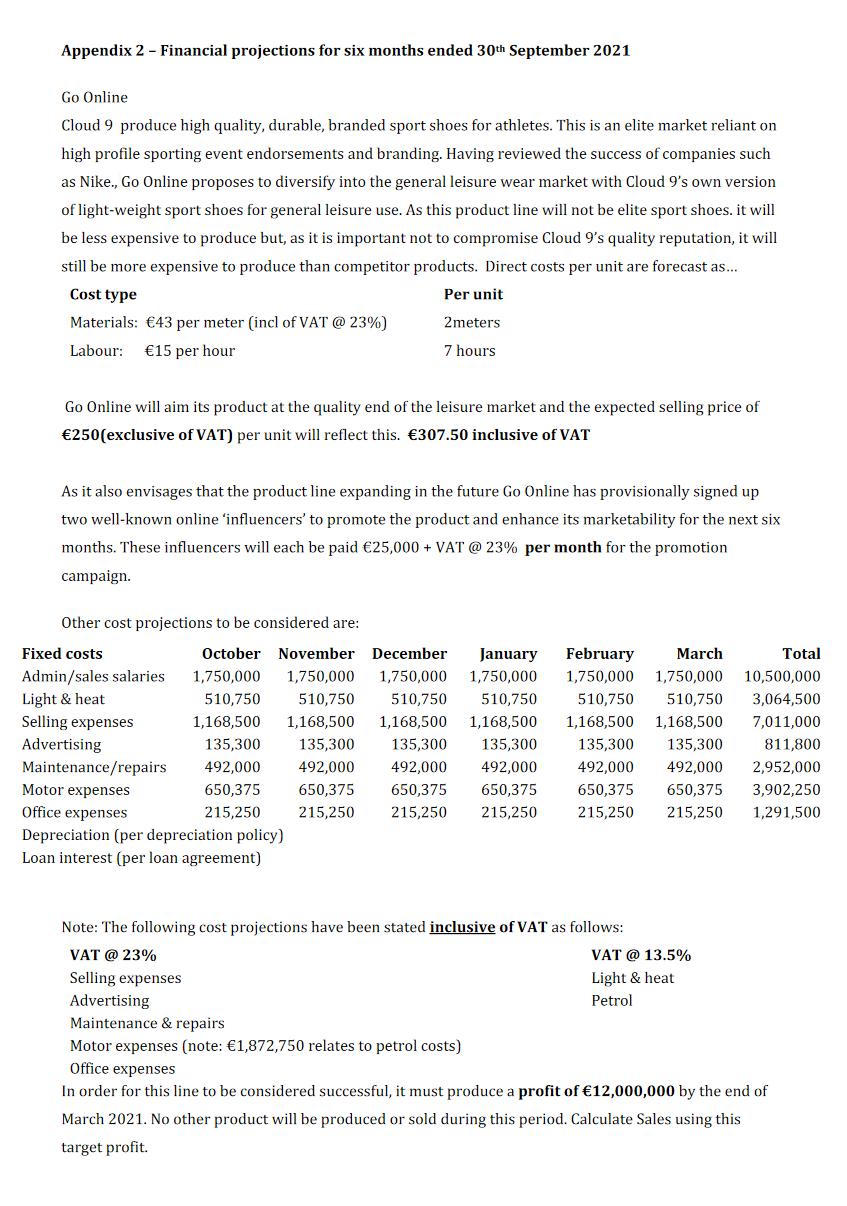

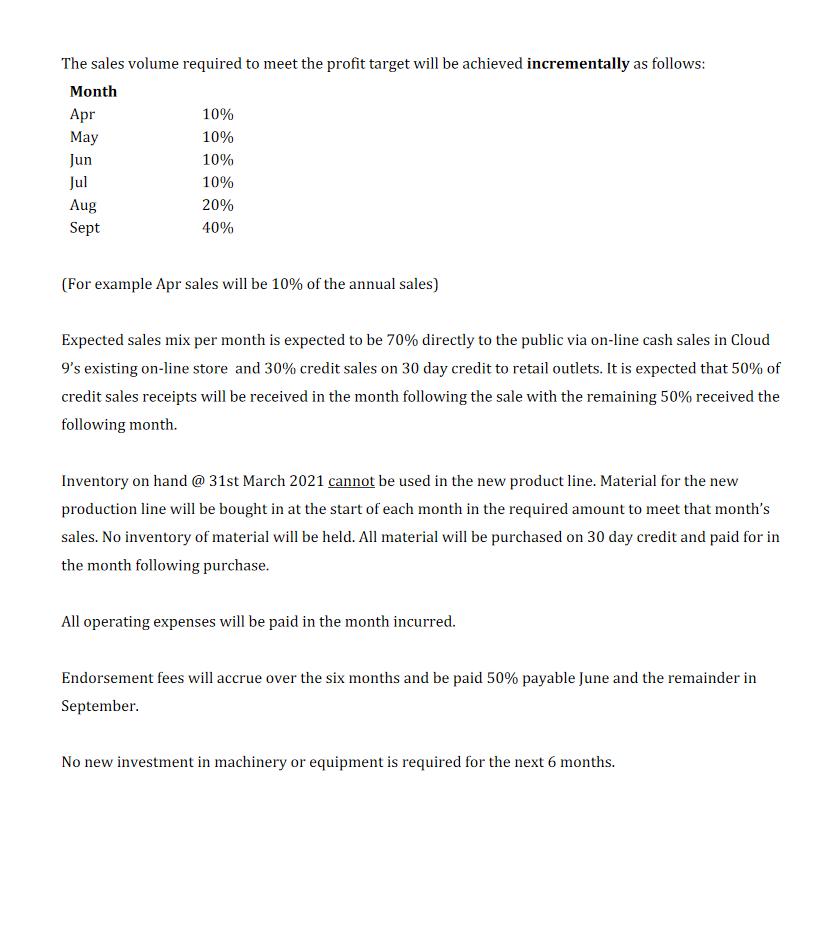

You have ascertained the following information to assist with your assessment: Cloud 9 is registered for VAT and charges 23% VAT on its sales. VAT returns are submitted on-line following the end of each (calendar) two monthly period and payment is made by the 23rd of the relevant month. Ignore taxation other than VAT. A loan of €69,000,000 was taken out with Irish Bank plc on 1st Apr 2015 and is repayable in full on 1st Apr 2025. The interest rate on the loan is 10% per annum, payable quarterly on 1st January, 1st April, 1st July and 1st Oct each year. All Cloud 9's sales and purchases are on 30-day credit terms. All other expenses are paid immediately on receipt of invoice. Cloud 9 depreciates it's property, plant & equipment on a straight-line basis as follows: Buildings 40 years Machinery 20 years Delivery vans 5 years Fixtures & fittings 10 years Office furniture & equipment 10 years The following appendices are included: Appendix 1: Trial balance extracted from Cloud 9's records @ 31st March 2021. Appendix 2: Details of Go Online's new manufacturing line and financial projections for the six months from 1st April 2021 to 30th September 2021 Appendix 3: Abridged financial statements for two previous years to 31st March 2020 and 2019. Please note that whilst your report package is to include specified statements and reports, it is necessary to include all relevant data and conclusions into the financial assessment to ensure that the full economic impact is considered. Appendix 1- Trial Balance @ 31st March 2021 Trial Balance as at 31st March 2021 €000 €000 Share capital 50,000 Retained earnings @ 31st March 2020 206,655 Loan 69,000 Building (cost) 100,000 Building accumulated depreciation @ 31st Mar 2020 25,000 Machinery (cost) 85,000 Machinery accumulated depreciation @ 31st Mar 2020 12,750 Delivery vans (cost) 18,500 Delivery vans accumulated depreciation @ 31st Mar 2020 Fixtures & fittings (cost) 7,400 14,000 Fixtures & fittings accumulated depreciation @ 31st Mar 2020 Office furniture & equipment (cost) 4,200 13,500 Office furniture & equipment accumulated depreciation @ 31st Mar 2020 5,400 Inventory @ 1st April 2020 147,500 Trade receivables 87,300 Bank overdraft 15,950 Trade payables VAT payable 45,700 6,220 Sales revenue 370,000 Purchases 248,750 Wages and salaries 62,500 Light and heat Selling expenses 7,250 6,500 Advertising 3,000 Client entertainment 2,750 Legal and professional fees 1,500 Maintenance and repairs Motor expenses 4,800 6,500 Office expenses 3,750 Interest expense 5,175 818,275 818,275 On 31st March 2021 the following expenses had not been accounted for. Cloud 9 plans to pay the outstanding amounts in April 2021. o Wages - overtime for March 2021 €3,200,000 Petrol for delivery vans (inclusive of VAT @ 13.5%) € 150,000 Legal fees (inclusive of VAT @ 23%) €1,230,000 Inventory on hand @ 31st March 2021 is valued at €171,250,000 Amounts due from trade receivables at 31st March 2021 are expected to be received 50% in April and remainder in May. Amounts due to trade payables at 31st March 2021 are expected to be paid in full in October. A B D E 1 Trading and Profit & Loss Account for the year ending 31st March 2021 2 €'000 €'000 3 Sales Revenue 370,000.00 4 Less: Cost of Goods Sold 1 € 225,000.00 5 Gross Profit 6 Less: Expenses 7 Wages & Salaries 8 Light & Heat 9 Selling Expenses 10 Advertising € 145,000.00 65,700.00 7,250.00 2 € 6,500.00 3,000.00 2,750.00 € 11 Client Entertainment € 12 Legal & Professional fees 13 Maintenance & Repairs 3 € 2,500.00 4,800.00 6,650.00 4 € 14 Motor Expenses 15 Office Expenses 16 Depreciation Expenses 17 Interest Expenses 3,750.00 5 € 6 € 13,200.00 6,900.00 € 123,000.00 18 Profit for the year 22,000.00 19 20 Balance Sheet as at 31st March 2021 21 €'000 €'000 22 Non Current Assets 23 Property, Plant & Equipment 1 € 163,050.00 € 163,050.00 24 Current Assets 25 Inventories 171,250.00 26 Trade Receivable 87,300.00 27 Total Current Assets 258,550.00 28 Total Assets 421,600.00 29 30 Equity & Liabilities 31 Share Capital 32 Retained Earnings 33 Total Equity 34 Non Current Liabilities 50,000.00 228,655.00 278,655.00 35 Loan 69,000.00 € 69,000.00 36 Current Liabilities 37 Bank Overdraft 15,950.00 38 Trade Payable 45,700.00 39 VAT Payable 5,990.00 40 Accrued Expenses 6,305.00 41 Total Current Liabilities 73,945.00 42 Total Liabilities € 421,600.00 43 Appendix 2 - Financial projections for six months ended 30th September 2021 Go Online Cloud 9 produce high quality, durable, branded sport shoes for athletes. This is an elite market reliant on high profile sporting event endorsements and branding. Having reviewed the success of companies such as Nike., Go Online proposes to diversify into the general leisure wear market with Cloud 9's own version of light-weight sport shoes for general leisure use. As this product line will not be elite sport shoes. it will be less expensive to produce but, as it is important not to compromise Cloud 9's quality reputation, it will still be more expensive to produce than competitor products. Direct costs per unit are forecast as... Cost type Per unit Materials: €43 per meter (incl of VAT @ 23%) 2meters Labour: €15 per hour 7 hours Go Online will aim its product at the quality end of the leisure market and the expected selling price of €250(exclusive of VAT) per unit will reflect this. €307.50 inclusive of VAT As it also envisages that the product line expanding in the future Go Online has provisionally signed up two well-known online 'influencers' to promote the product and enhance its marketability for the next six months. These influencers will each be paid €25,000 + VAT @ 23% per month for the promotion campaign. Other cost projections to be considered are: Fixed costs October November December January February March Total Admin/sales salaries 1,750,000 1,750,000 1,750,000 1,750,000 1,750,000 1,750,000 10,500,000 Light & heat Selling expenses 510,750 510,750 510,750 510,750 510,750 510,750 3,064,500 1,168,500 1,168,500 1,168,500 1,168,500 1,168,500 1,168,500 7,011,000 Advertising 135,300 135,300 135,300 135,300 135,300 135,300 811,800 Maintenance/repairs 492,000 492,000 492,000 492,000 492,000 492,000 2,952,000 Motor expenses 650,375 650,375 650,375 650,375 650,375 650,375 3,902,250 Office expenses 215,250 215,250 215,250 215,250 215,250 215,250 1,291,500 Depreciation (per depreciation policy) Loan interest (per loan agreement) Note: The following cost projections have been stated inclusive of VAT as follows: VAT @ 23% VAT @ 13.5% Selling expenses Light & heat Advertising Maintenance & repairs Petrol Motor expenses (note: €1,872,750 relates to petrol costs) Office expenses In order for this line to be considered successful, it must produce a profit of €12,000,000 by the end of March 2021. No other product will be produced or sold during this period. Calculate Sales using this target profit. The sales volume required to meet the profit target will be achieved incrementally as follows: Month Apr 10% May 10% Jun 10% Jul 10% Aug 20% Sept 40% (For example Apr sales will be 10% of the annual sales) Expected sales mix per month is expected to be 70% directly to the public via on-line cash sales in Cloud 9's existing on-line store and 30% credit sales on 30 day credit to retail outlets. It is expected that 50% of credit sales receipts will be received in the month following the sale with the remaining 50% received the following month. Inventory on hand @ 31st March 2021 cannot be used in the new product line. Material for the new production line will be bought in at the start of each month in the required amount to meet that month's sales. No inventory of material will be held. All material will be purchased on 30 day credit and paid for in the month following purchase. All operating expenses will be paid in the month incurred. Endorsement fees will accrue over the six months and be paid 50% payable June and the remainder in September. No new investment in machinery or equipment is required for the next 6 months. Forecast trading, profit and loss account by month for 6 months ended 30th September 2021, contribution format Oct Nov Dec Jan Feb Mar Total Sales units Selling price per unit Sales revenue € Less Direct variable costs Materials per unit Materials cost € Labour per unit Labour cost € Total variable cost Contribution Less fixed costs Admin/sales salaries Light & heat Selling expenses Advertising Maintenance/repairs Motor/petrol exps Office expenses Depreciation Loan interest Endorsement fees Total fixed costs Profit/(loss) Workings for forecast trading, profit and loss account You have ascertained the following information to assist with your assessment: Cloud 9 is registered for VAT and charges 23% VAT on its sales. VAT returns are submitted on-line following the end of each (calendar) two monthly period and payment is made by the 23rd of the relevant month. Ignore taxation other than VAT. A loan of €69,000,000 was taken out with Irish Bank plc on 1st Apr 2015 and is repayable in full on 1st Apr 2025. The interest rate on the loan is 10% per annum, payable quarterly on 1st January, 1st April, 1st July and 1st Oct each year. All Cloud 9's sales and purchases are on 30-day credit terms. All other expenses are paid immediately on receipt of invoice. Cloud 9 depreciates it's property, plant & equipment on a straight-line basis as follows: Buildings 40 years Machinery 20 years Delivery vans 5 years Fixtures & fittings 10 years Office furniture & equipment 10 years The following appendices are included: Appendix 1: Trial balance extracted from Cloud 9's records @ 31st March 2021. Appendix 2: Details of Go Online's new manufacturing line and financial projections for the six months from 1st April 2021 to 30th September 2021 Appendix 3: Abridged financial statements for two previous years to 31st March 2020 and 2019. Please note that whilst your report package is to include specified statements and reports, it is necessary to include all relevant data and conclusions into the financial assessment to ensure that the full economic impact is considered. Appendix 1- Trial Balance @ 31st March 2021 Trial Balance as at 31st March 2021 €000 €000 Share capital 50,000 Retained earnings @ 31st March 2020 206,655 Loan 69,000 Building (cost) 100,000 Building accumulated depreciation @ 31st Mar 2020 25,000 Machinery (cost) 85,000 Machinery accumulated depreciation @ 31st Mar 2020 12,750 Delivery vans (cost) 18,500 Delivery vans accumulated depreciation @ 31st Mar 2020 Fixtures & fittings (cost) 7,400 14,000 Fixtures & fittings accumulated depreciation @ 31st Mar 2020 Office furniture & equipment (cost) 4,200 13,500 Office furniture & equipment accumulated depreciation @ 31st Mar 2020 5,400 Inventory @ 1st April 2020 147,500 Trade receivables 87,300 Bank overdraft 15,950 Trade payables VAT payable 45,700 6,220 Sales revenue 370,000 Purchases 248,750 Wages and salaries 62,500 Light and heat Selling expenses 7,250 6,500 Advertising 3,000 Client entertainment 2,750 Legal and professional fees 1,500 Maintenance and repairs Motor expenses 4,800 6,500 Office expenses 3,750 Interest expense 5,175 818,275 818,275 On 31st March 2021 the following expenses had not been accounted for. Cloud 9 plans to pay the outstanding amounts in April 2021. o Wages - overtime for March 2021 €3,200,000 Petrol for delivery vans (inclusive of VAT @ 13.5%) € 150,000 Legal fees (inclusive of VAT @ 23%) €1,230,000 Inventory on hand @ 31st March 2021 is valued at €171,250,000 Amounts due from trade receivables at 31st March 2021 are expected to be received 50% in April and remainder in May. Amounts due to trade payables at 31st March 2021 are expected to be paid in full in October. A B D E 1 Trading and Profit & Loss Account for the year ending 31st March 2021 2 €'000 €'000 3 Sales Revenue 370,000.00 4 Less: Cost of Goods Sold 1 € 225,000.00 5 Gross Profit 6 Less: Expenses 7 Wages & Salaries 8 Light & Heat 9 Selling Expenses 10 Advertising € 145,000.00 65,700.00 7,250.00 2 € 6,500.00 3,000.00 2,750.00 € 11 Client Entertainment € 12 Legal & Professional fees 13 Maintenance & Repairs 3 € 2,500.00 4,800.00 6,650.00 4 € 14 Motor Expenses 15 Office Expenses 16 Depreciation Expenses 17 Interest Expenses 3,750.00 5 € 6 € 13,200.00 6,900.00 € 123,000.00 18 Profit for the year 22,000.00 19 20 Balance Sheet as at 31st March 2021 21 €'000 €'000 22 Non Current Assets 23 Property, Plant & Equipment 1 € 163,050.00 € 163,050.00 24 Current Assets 25 Inventories 171,250.00 26 Trade Receivable 87,300.00 27 Total Current Assets 258,550.00 28 Total Assets 421,600.00 29 30 Equity & Liabilities 31 Share Capital 32 Retained Earnings 33 Total Equity 34 Non Current Liabilities 50,000.00 228,655.00 278,655.00 35 Loan 69,000.00 € 69,000.00 36 Current Liabilities 37 Bank Overdraft 15,950.00 38 Trade Payable 45,700.00 39 VAT Payable 5,990.00 40 Accrued Expenses 6,305.00 41 Total Current Liabilities 73,945.00 42 Total Liabilities € 421,600.00 43 Appendix 2 - Financial projections for six months ended 30th September 2021 Go Online Cloud 9 produce high quality, durable, branded sport shoes for athletes. This is an elite market reliant on high profile sporting event endorsements and branding. Having reviewed the success of companies such as Nike., Go Online proposes to diversify into the general leisure wear market with Cloud 9's own version of light-weight sport shoes for general leisure use. As this product line will not be elite sport shoes. it will be less expensive to produce but, as it is important not to compromise Cloud 9's quality reputation, it will still be more expensive to produce than competitor products. Direct costs per unit are forecast as... Cost type Per unit Materials: €43 per meter (incl of VAT @ 23%) 2meters Labour: €15 per hour 7 hours Go Online will aim its product at the quality end of the leisure market and the expected selling price of €250(exclusive of VAT) per unit will reflect this. €307.50 inclusive of VAT As it also envisages that the product line expanding in the future Go Online has provisionally signed up two well-known online 'influencers' to promote the product and enhance its marketability for the next six months. These influencers will each be paid €25,000 + VAT @ 23% per month for the promotion campaign. Other cost projections to be considered are: Fixed costs October November December January February March Total Admin/sales salaries 1,750,000 1,750,000 1,750,000 1,750,000 1,750,000 1,750,000 10,500,000 Light & heat Selling expenses 510,750 510,750 510,750 510,750 510,750 510,750 3,064,500 1,168,500 1,168,500 1,168,500 1,168,500 1,168,500 1,168,500 7,011,000 Advertising 135,300 135,300 135,300 135,300 135,300 135,300 811,800 Maintenance/repairs 492,000 492,000 492,000 492,000 492,000 492,000 2,952,000 Motor expenses 650,375 650,375 650,375 650,375 650,375 650,375 3,902,250 Office expenses 215,250 215,250 215,250 215,250 215,250 215,250 1,291,500 Depreciation (per depreciation policy) Loan interest (per loan agreement) Note: The following cost projections have been stated inclusive of VAT as follows: VAT @ 23% VAT @ 13.5% Selling expenses Light & heat Advertising Maintenance & repairs Petrol Motor expenses (note: €1,872,750 relates to petrol costs) Office expenses In order for this line to be considered successful, it must produce a profit of €12,000,000 by the end of March 2021. No other product will be produced or sold during this period. Calculate Sales using this target profit. The sales volume required to meet the profit target will be achieved incrementally as follows: Month Apr 10% May 10% Jun 10% Jul 10% Aug 20% Sept 40% (For example Apr sales will be 10% of the annual sales) Expected sales mix per month is expected to be 70% directly to the public via on-line cash sales in Cloud 9's existing on-line store and 30% credit sales on 30 day credit to retail outlets. It is expected that 50% of credit sales receipts will be received in the month following the sale with the remaining 50% received the following month. Inventory on hand @ 31st March 2021 cannot be used in the new product line. Material for the new production line will be bought in at the start of each month in the required amount to meet that month's sales. No inventory of material will be held. All material will be purchased on 30 day credit and paid for in the month following purchase. All operating expenses will be paid in the month incurred. Endorsement fees will accrue over the six months and be paid 50% payable June and the remainder in September. No new investment in machinery or equipment is required for the next 6 months. Forecast trading, profit and loss account by month for 6 months ended 30th September 2021, contribution format Oct Nov Dec Jan Feb Mar Total Sales units Selling price per unit Sales revenue € Less Direct variable costs Materials per unit Materials cost € Labour per unit Labour cost € Total variable cost Contribution Less fixed costs Admin/sales salaries Light & heat Selling expenses Advertising Maintenance/repairs Motor/petrol exps Office expenses Depreciation Loan interest Endorsement fees Total fixed costs Profit/(loss) Workings for forecast trading, profit and loss account

Expert Answer:

Answer rating: 100% (QA)

Ratio Analysis 2019 2020 2021 1 Current Ratio A B Formula Current Assets Current Liabilities 237 284 350 A Current Assets 252630 230800 258550 B Curre... View the full answer

Related Book For

Intermediate Accounting

ISBN: 978-0324592375

17th Edition

Authors: James D. Stice, Earl K. Stice, Fred Skousen

Posted Date:

Students also viewed these accounting questions

-

Preparing a classified balance sheet Required Use the following information to prepare a classified balance sheet for Steller Co. at the end of 2012. Accounts receivable .... $42,500 Accounts payable...

-

Multiple Choice Questions Use the following information to answer questions 1 and 2. Melody Logos manufactures key chains for college bookstores. During the year, the company produced 35,000 key...

-

Use the following information to answer parts (a) through (f). Describe what the results of each calculation mean to you as a project manager. What do you propose to do? PV = $500,000 EV = $350,000...

-

This short exercise demonstrates the similarity and the difference between two ways to acquire plant assets. i (Click the icon to view the cases.) Compare the balances in all the accounts after...

-

In a study by Peter D. Hart Research Associates for the Nasdaq Stock Market, it was determined that 20% of all stock investors are retired people. In addition, 40% of all U.S. adults invest in mutual...

-

What is the implied assumption about how people behave in the tragedy of the commons? Do you think this is always the way people behave? How might different institutions and incentives work into your...

-

Clickety Ltd is preparing a master budget for the first quarter of the financial year ending 31 March 2025, and has compiled the following data. 1. The firm sells a single product at a price of $26...

-

(Deferred Tax Liability, Change in Tax Rate, Prepare Section of Income Statement) Sharer Inc.s only temporary difference at the beginning and end of 2010 is caused by a $2 million deferred gain for...

-

What were some of the socioeconomic conditions in 19th-century America that led the majority of state courts to adopt the legal principle of employment-at-will? How do advocates of the...

-

Q4. Review the accounts receivable lead sheet memo and related workpapers (AR.3.1 to AR.3.4). Evaluate the auditors' tickmarks, comments, and explanations in the memo and on the lead sheet. Identify...

-

answered Marked out of 35.00 Steinhoff Accounting Irregularities JOHANNESBURG (Reuters) - Steinhoff SNHJ.JSNHG.DE will have to restate its 2015 accounts and maybe earlier figures, the South African...

-

Find min in the sorted rotated list. //Sorts a given list by selection sort //Input: An array A[0..n-1] of orderable elements. //Output: List A[ 0..n-1] sorted in ascending order Algorithm...

-

Describe the nature and purpose of a surrogacy agreement.

-

Identify some of the ethical issues that arise in the context of assisted reproductive technology.

-

Identify the primary purposes of cryopreserving embryos.

-

Identify and describe the four tests most often applied by the courts to resolve disputes arising out of surrogacy arrangements.

-

What is the type of Consensus in blockchain? a . . Proof of Work ( ( PoW ) ) b . . Proof of Agreement ( ( PoA ) ) c . . Proof of Truth ( ( PoT ) ) d . . Proof of Evidence ( ( PoE ) )

-

For Problem estimate the change in y for the given change in x. y = f(x), f'(12) = 30, x increases from 12 to 12.2

-

What is the most common event that causes the inventory account to increase? decrease?

-

The company miscounted its inventory at the end of the year. The correct amount of inventory was $100,000. The error was not discovered until the following May when the books for the preceding year...

-

A review of the books of Lakeshore Electric Co. disclosed that there were five transactions involving gains and losses on the exchange of fixed assets. The transactions were recorded as indicated in...

-

In Figure 27.41, do \(\vec{F}_{\mathrm{p}}^{B}\) and \(\vec{F}_{\mathrm{p}}^{E}\) still cancel if the charged particle (a) carries a negative charge, (b) travels in the opposite direction, (c)...

-

A proton and an electron travel through a region of uniform magnetic field \(\vec{B}\). If their speeds are the same, what is the ratio \(R_{\mathrm{p}} / R_{\mathrm{e}}\) of the radii of their...

-

(a) Express the magnitude of the electric field inside the strip in Figure 27.43 in terms of the width \(w\) of the strip and the potential difference \(V_{\mathrm{RL}}\). (b) Given the magnitude...

Study smarter with the SolutionInn App