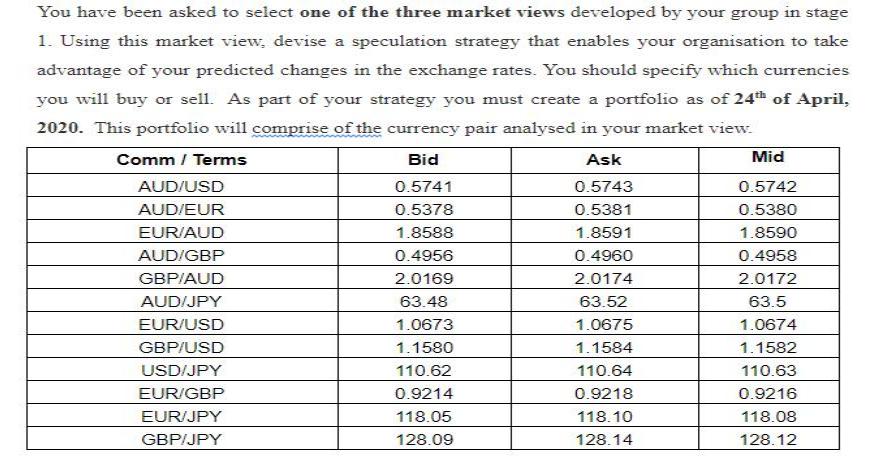

You have been asked to select one of the three market views developed by your group...

Fantastic news! We've Found the answer you've been seeking!

Question:

![Question 2 [7 marks] The senior management is concerned about the recent developments in the financial markets. There is a ge](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2021/05/60954f279ad38_1620397862664.jpg)

Transcribed Image Text:

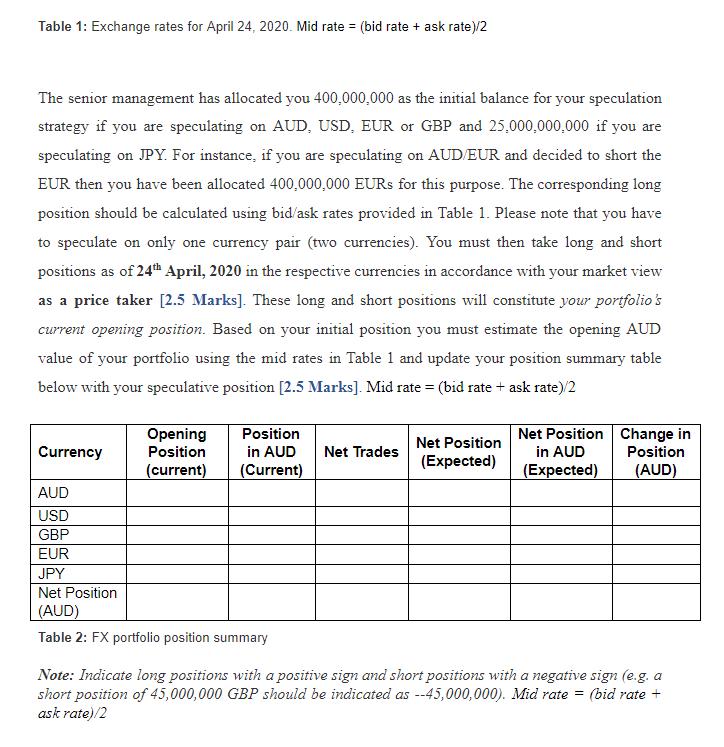

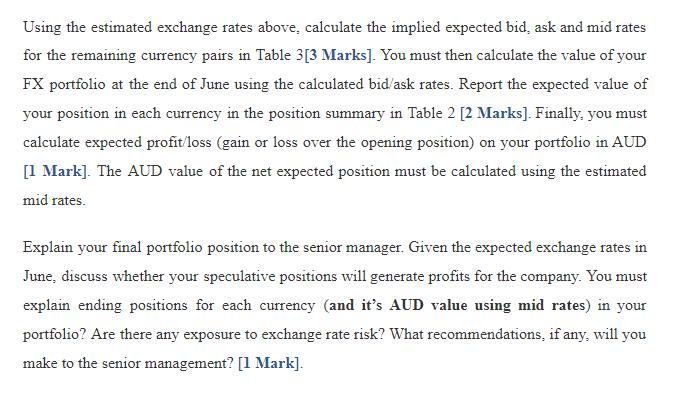

You have been asked to select one of the three market views developed by your group in stage 1. Using this market view, devise a speculation strategy that enables your organisation to take advantage of your predicted changes in the exchange rates. You should specify which currencies you will buy or sell. As part of your strategy you must create a portfolio as of 24th of April, 2020. This portfolio will comprise of the currency pair analysed in your market view. Comm / Terms Bid Ask Mid AUD/USD 0.5741 0.5743 0.5742 AUD/EUR 0.5378 0.5381 0.5380 EUR/AUD 1.8588 1.8591 1.8590 AUD/GBP 0.4956 0.4960 0.4958 GBP/AUD 2.0169 2.0174 2.0172 AUD/JPY 63.48 63.52 63.5 EUR/USD 1.0673 1.0675 1.0674 GBP/USD 1.1580 1.1584 1.1582 USD/JPY 110.62 110.64 110.63 EUR/GBP 0.9214 0.9218 0.9216 EUR/JPY 118.05 118.10 118.08 GBP/JPY 128.09 128.14 128.12 Table 1: Exchange rates for April 24, 2020. Mid rate = (bid rate + ask rate)/2 The senior management has allocated you 400,000,000 as the initial balance for your speculation strategy if you are speculating on AUD, USD, EUR or GBP and 25,000,000,000 if you are speculating on JPY. For instance, if you are speculating on AUD/EUR and decided to short the EUR then you have been allocated 400,000,000 EURS for this purpose. The corresponding long position should be calculated using bid/ask rates provided in Table 1. Please note that you have to speculate on only one currency pair (two currencies). You must then take long and short positions as of 24h April, 2020 in the respective currencies in accordance with your market view as a price taker [2.5 Marks]. These long and short positions will constitute your portfolio's current opening position. Based on your initial position you must estimate the opening AUD value of your portfolio using the mid rates in Table 1 and update your position summary table below with your speculative position [2.5 Marks]. Mid rate = (bid rate + ask rate)/2 Position in AUD (Current) Net Position Change in in AUD (Expected) Opening Net Position Currency Position Net Trades Position (Expected) (current) (AUD) AUD USD GBP EUR JPY Net Position (AUD) Table 2: FX portfolio position summary Note: Indicate long positions with a positive sign and short positions with a negative sign (e.g. a short position of 45,000,000 GBP should be indicated as --45,000,000). Mid rate = (bid rate + ask rate)/2 Question 2 [7 marks] The senior management is concerned about the recent developments in the financial markets. There is a general belief that market volatility was relatively high, yet it might climb even higher than expected in the near future due to the current global health crisis. You have been asked to conduct a thorough risk assessment of your speculative positions undertaken in question 1. For BAFI1002 Financial Markets – Group FX Assignment (Stage 2) this purpose, the firm's foreign currency analyst has provided you with the following forecast for US dollar exchange rates as at the end of June 2020: Comm / Terms Bid Ask Mid AUD/USD 0.6135 0.614 0.6138 AUD/EUR EUR/AUD 1.8022 1.8035 1.8029 AUD/GBP GBP/AUD 2.0291 2.0298 2.0295 AUDIJPY EUR/USD 1.1063 1.1064 1.1064 GBP/USD 1.2437 1.2441 1.2439 USD/JPY 107.9 107.93 107.9150 EUR/GBP EURIJPY GBP/JPY Table 3: Expected exchange rates for June, 2020. Mid rate = (bid rate + ask rate)/2 Using the estimated exchange rates above, calculate the implied expected bid, ask and mid rates for the remaining currency pairs in Table 3[3 Marks]. You must then calculate the value of your FX portfolio at the end of June using the calculated bid/ask rates. Report the expected value of your position in each currency in the position summary in Table 2 [2 Marks]. Finally, you must calculate expected profit'loss (gain or loss over the opening position) on your portfolio in AUD [1 Mark]. The AUD value of the net expected position must be calculated using the estimated mid rates. Explain your final portfolio position to the senior manager. Given the expected exchange rates in June, discuss whether your speculative positions will generate profits for the company. You must explain ending positions for each currency (and it's AUD value using mid rates) in your portfolio? Are there any exposure to exchange rate risk? What recommendations, if any, will you make to the senior management? [1 Mark]. You have been asked to select one of the three market views developed by your group in stage 1. Using this market view, devise a speculation strategy that enables your organisation to take advantage of your predicted changes in the exchange rates. You should specify which currencies you will buy or sell. As part of your strategy you must create a portfolio as of 24th of April, 2020. This portfolio will comprise of the currency pair analysed in your market view. Comm / Terms Bid Ask Mid AUD/USD 0.5741 0.5743 0.5742 AUD/EUR 0.5378 0.5381 0.5380 EUR/AUD 1.8588 1.8591 1.8590 AUD/GBP 0.4956 0.4960 0.4958 GBP/AUD 2.0169 2.0174 2.0172 AUD/JPY 63.48 63.52 63.5 EUR/USD 1.0673 1.0675 1.0674 GBP/USD 1.1580 1.1584 1.1582 USD/JPY 110.62 110.64 110.63 EUR/GBP 0.9214 0.9218 0.9216 EUR/JPY 118.05 118.10 118.08 GBP/JPY 128.09 128.14 128.12 Table 1: Exchange rates for April 24, 2020. Mid rate = (bid rate + ask rate)/2 The senior management has allocated you 400,000,000 as the initial balance for your speculation strategy if you are speculating on AUD, USD, EUR or GBP and 25,000,000,000 if you are speculating on JPY. For instance, if you are speculating on AUD/EUR and decided to short the EUR then you have been allocated 400,000,000 EURS for this purpose. The corresponding long position should be calculated using bid/ask rates provided in Table 1. Please note that you have to speculate on only one currency pair (two currencies). You must then take long and short positions as of 24h April, 2020 in the respective currencies in accordance with your market view as a price taker [2.5 Marks]. These long and short positions will constitute your portfolio's current opening position. Based on your initial position you must estimate the opening AUD value of your portfolio using the mid rates in Table 1 and update your position summary table below with your speculative position [2.5 Marks]. Mid rate = (bid rate + ask rate)/2 Position in AUD (Current) Net Position Change in in AUD (Expected) Opening Net Position Currency Position Net Trades Position (Expected) (current) (AUD) AUD USD GBP EUR JPY Net Position (AUD) Table 2: FX portfolio position summary Note: Indicate long positions with a positive sign and short positions with a negative sign (e.g. a short position of 45,000,000 GBP should be indicated as --45,000,000). Mid rate = (bid rate + ask rate)/2 Question 2 [7 marks] The senior management is concerned about the recent developments in the financial markets. There is a general belief that market volatility was relatively high, yet it might climb even higher than expected in the near future due to the current global health crisis. You have been asked to conduct a thorough risk assessment of your speculative positions undertaken in question 1. For BAFI1002 Financial Markets – Group FX Assignment (Stage 2) this purpose, the firm's foreign currency analyst has provided you with the following forecast for US dollar exchange rates as at the end of June 2020: Comm / Terms Bid Ask Mid AUD/USD 0.6135 0.614 0.6138 AUD/EUR EUR/AUD 1.8022 1.8035 1.8029 AUD/GBP GBP/AUD 2.0291 2.0298 2.0295 AUDIJPY EUR/USD 1.1063 1.1064 1.1064 GBP/USD 1.2437 1.2441 1.2439 USD/JPY 107.9 107.93 107.9150 EUR/GBP EURIJPY GBP/JPY Table 3: Expected exchange rates for June, 2020. Mid rate = (bid rate + ask rate)/2 Using the estimated exchange rates above, calculate the implied expected bid, ask and mid rates for the remaining currency pairs in Table 3[3 Marks]. You must then calculate the value of your FX portfolio at the end of June using the calculated bid/ask rates. Report the expected value of your position in each currency in the position summary in Table 2 [2 Marks]. Finally, you must calculate expected profit'loss (gain or loss over the opening position) on your portfolio in AUD [1 Mark]. The AUD value of the net expected position must be calculated using the estimated mid rates. Explain your final portfolio position to the senior manager. Given the expected exchange rates in June, discuss whether your speculative positions will generate profits for the company. You must explain ending positions for each currency (and it's AUD value using mid rates) in your portfolio? Are there any exposure to exchange rate risk? What recommendations, if any, will you make to the senior management? [1 Mark].

Expert Answer:

Related Book For

Organizational Behavior

ISBN: 978-0077862589

7th edition

Authors: Steven McShane, Mary Ann Von Glinow

Posted Date:

Students also viewed these accounting questions

-

As a junior congressperson you have been asked to help promote a bill to allow casino gambling in your state. There is much opposition to this bill. Using distributive bargaining, discuss the pros...

-

You have been asked to evaluate possible sites for an Asian production facility that will manufacture your firms products and sell them to the Asian market. What real exchange rate considerations...

-

As a securities analyst you have been asked to review a valuation of a closely held business, Wigwam Autoparts Heaven, Inc. (WAH), prepared by the Red Rocks Group (RRG). You are to give an opinion on...

-

Consider two industries in which firms hold the following market shares: Industry A: 25%, 20%, 18%, 15%, 8%, 7%, 4%, 2%, 1% Industry B: 30%, 10%, 9%, 8%, 8%, 8%, 8%, 6%, 6%, 5%, 2% What are the...

-

Would you prefer to own a single-family detached home or a condominium? What are your perceptions of the advantages and disadvantages of each?

-

A cricket specialty wholesaler operates 50 weeks per year. Management is trying to determine an inventory policy for its bats, which have the following characteristics: Demand (D) = 350,000...

-

Cruz Manufacturing Ltds sales slumped badly in 2025. For the first time in its history, it operated at a loss. The companys income statement showed the following results from selling 600 000 units of...

-

Vanadium Audio Inc. is a small manufacturer of electronic musical instruments. The plant manager received the following variable factory overhead report for the period: The plant manager is not...

-

Managers have to be prepared to lead their organizations through varying economic conditions. Explain why it is important to understand GDP data, and how changes inunemployment and inflation impact...

-

Write a letter to the Smith's discussing the results of their tax return, remind them of any deduction substantiation rules they need to follow (receipts, mileage log, etc.), offer suggestions for...

-

On January 1, 2019, Bank Dhofar issued CD in Muscat Securities Market which will mature on October 30, 2019. The CD pays a 7 % interest rate. Calculate the interest earned on this CD with a face...

-

PAIBOC Questions and analysis Scenario: Seneca has decided to hold a health promotion day for students and faculty next month. In preparation for this event, Seneca students are invited to share...

-

What role does agency play in the Hypodermic Model of Communication? Long after the model has been abandoned by experts in persuasion and mass media, why does this model live on as common sense?

-

What is Clinical Psychology? Answers I specifically have are: What does this specialty work on specifically? How do the different types of psychologies relate to the study Clinical Psychologists do?...

-

A particle executes simple harmonic motion with an amplitude of 1.69 cm. At what positive displacement from the midpoint of its motion does its speed equal one half of its maximum speed? Answer in...

-

Using your understanding of effective and ethical leadership as well as 6 principles that underpin such leadership, how would you go about assessing Steinhoffs leadership (i.e., what would you...

-

If a customer bought $200,000 worth of goods and paid the firm cash eight days after the sale, how much cash would Tun Ash Inc. get from the customer? (Note: Round your answer to the nearest whole...

-

Swifty company is a publicly held corporation whose $1 par value stock is actively traded at $30 per share. The company issued 3400 shares of stock to acquire land recently advertised at $93000. When...

-

The organization for which you have been working for five years is suffering from a global recession. In response, it changes your compensation structure. Discuss the role of moral intensity, moral...

-

A federal government department has high levels of absenteeism among the office staff. The head of office administration argues that employees are misusing the company's sick leave benefits. However,...

-

How have the division and coordination of labor evolved at Merritt's Bakery from its beginnings to today?

-

If unexpected increases in the growth rate of the money supply can increase real GDP, why doesnt the Fed follow a policy of unexpectedly increasing the money supply to increase the growth of real GDP?

-

Draw an aggregate demand and supply diagram for each theory of macroeconomics. Use the diagrams to explain how the government can influence equilibrium real GDP and prices.

-

What, if any, similarities are there among the theories of economics discussed in this chapter regarding the use of fiscal and monetary policies to stimulate real GDP?

Study smarter with the SolutionInn App