Question: You have data for the return on a weighted portfolio of all the stocks in the market. The retum series is denoted MKT and the

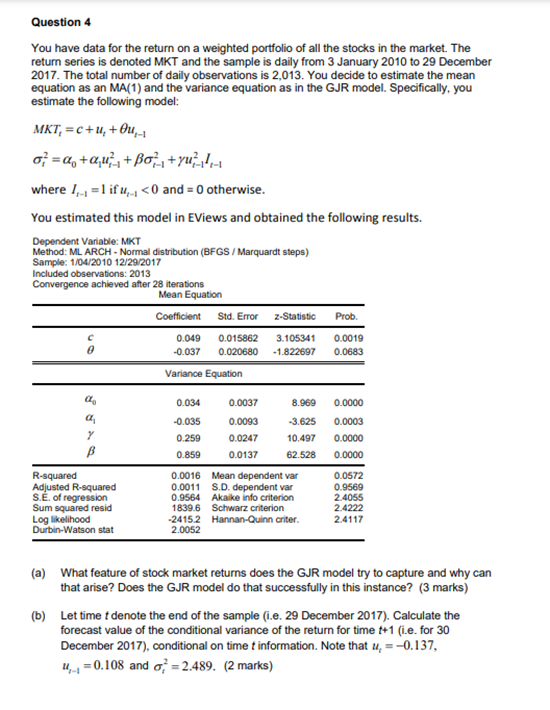

You have data for the return on a weighted portfolio of all the stocks in the market. The retum series is denoted MKT and the sample is daily from 3 January 2010 to 29 December 2017. The total number of daily observations is 2,013 . You decide to estimate the mean equation as an MA(1) and the variance equation as in the GJR model. Specifically, you estimate the following model: MKTt=c+ut+ut1t2=0+1ut=12+t12+ut=12It=1 where It1=1 if ut1

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock