Question: You want to evaluate two mutual funds using the information ratio measure for performance evaluation. The risk-free return during the sample period is 4.00%,

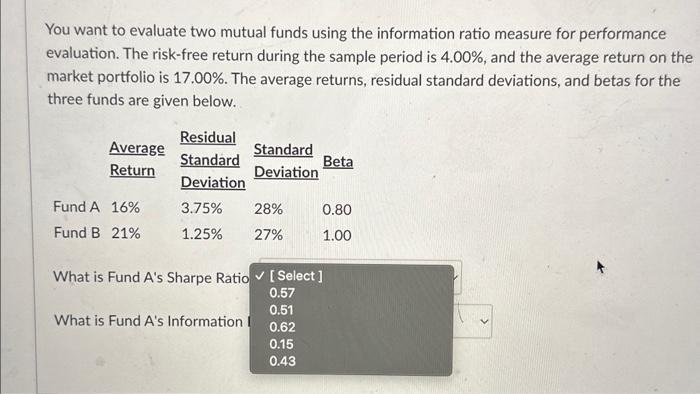

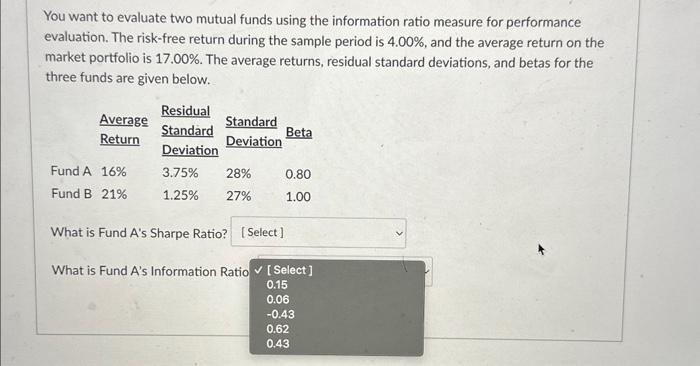

You want to evaluate two mutual funds using the information ratio measure for performance evaluation. The risk-free return during the sample period is 4.00%, and the average return on the market portfolio is 17.00%. The average returns, residual standard deviations, and betas for the three funds are given below. Average Return Fund A 16% Fund B 21% Residual Standard Deviation 3.75% 28% 1.25% 27% Standard Deviation What is Fund A's Information I Beta 0.80 1.00 What is Fund A's Sharpe Ratio [Select] 0.57 0.51 0.62 0.15 0.43 You want to evaluate two mutual funds using the information ratio measure for performance evaluation. The risk-free return during the sample period is 4.00 %, and the average return on the market portfolio is 17.00%. The average returns, residual standard deviations, and betas for the three funds are given below. Average Return Fund A 16% Fund B 21% Residual Standard Deviation Standard Deviation 3.75% 28% 1.25% 27% Beta 0.80 1.00 What is Fund A's Sharpe Ratio? [Select] What is Fund A's Information Ratio [Select] 0.15 0.06 -0.43 0.62 0.43

Step by Step Solution

There are 3 Steps involved in it

The Sharpe Ratio is calculated as For Fund A Average Return of Fund A ... View full answer

Get step-by-step solutions from verified subject matter experts