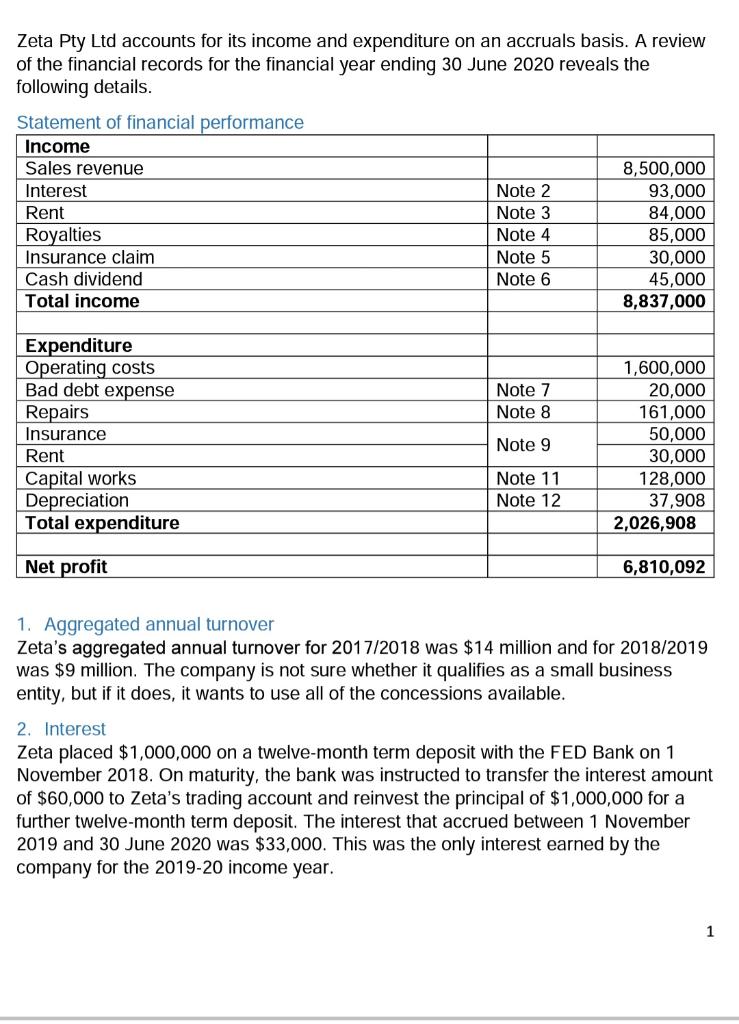

Zeta Pty Ltd accounts for its income and expenditure on an accruals basis. A review of...

Fantastic news! We've Found the answer you've been seeking!

Transcribed Image Text:

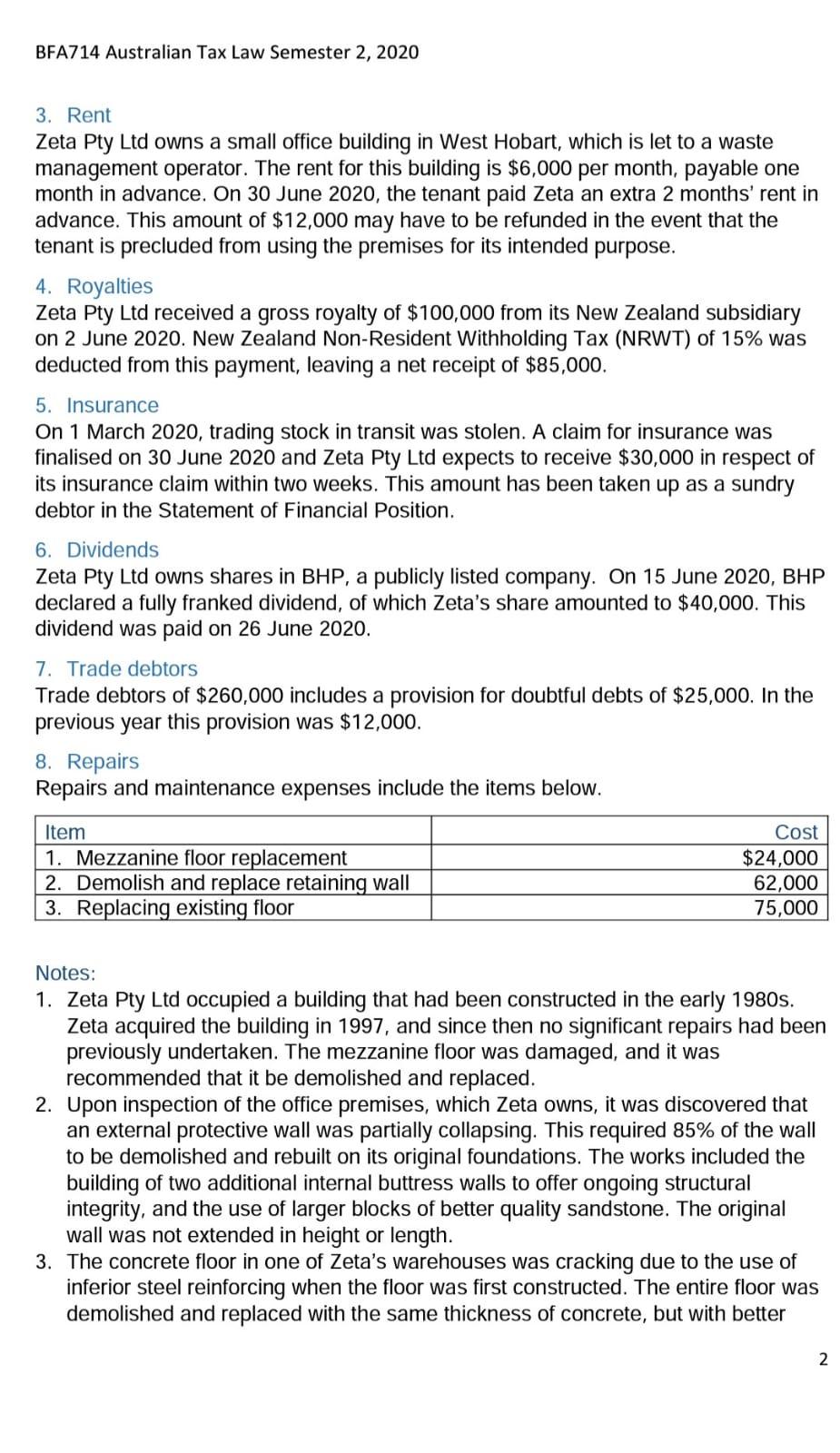

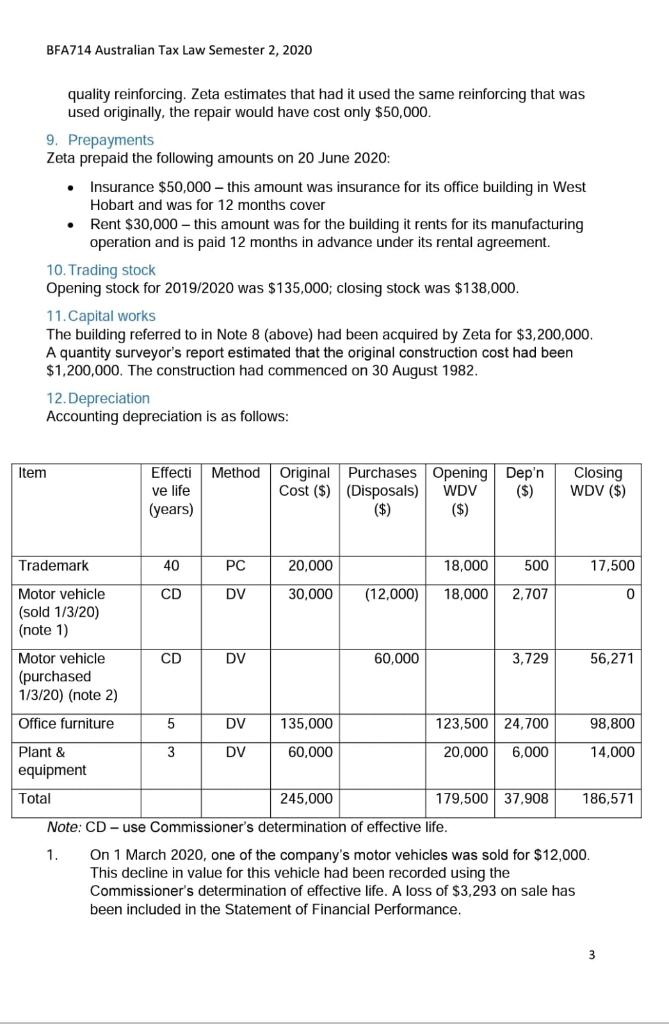

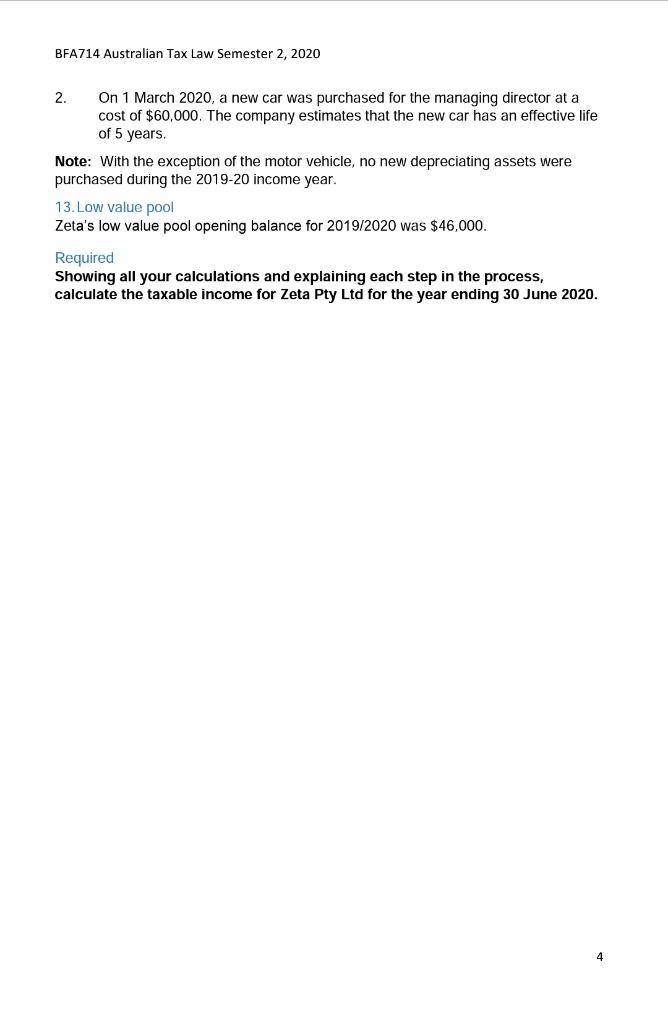

Zeta Pty Ltd accounts for its income and expenditure on an accruals basis. A review of the financial records for the financial year ending 30 June 2020 reveals the following details. Statement of financial performance Income Sales revenue Interest Rent Royalties Insurance claim Cash dividend Total income Expenditure Operating costs Bad debt expense Repairs Insurance Rent Capital works Depreciation Total expenditure Net profit Note 2 Note 3 Note 4 Note 5 Note 6 Note 7 Note 8 Note 9 Note 11 Note 12 8,500,000 93,000 84,000 85,000 30,000 45,000 8,837,000 1,600,000 20,000 161,000 50,000 30,000 128,000 37,908 2,026,908 6,810,092 1. Aggregated annual turnover Zeta's aggregated annual turnover for 2017/2018 was $14 million and for 2018/2019 was $9 million. The company is not sure whether it qualifies as a small business entity, but if it does, it wants to use all of the concessions available. 2. Interest Zeta placed $1,000,000 on a twelve-month term deposit with the FED Bank on 1 November 2018. On maturity, the bank was instructed to transfer the interest amount of $60,000 to Zeta's trading account and reinvest the principal of $1,000,000 for a further twelve-month term deposit. The interest that accrued between 1 November 2019 and 30 June 2020 was $33,000. This was the only interest earned by the company for the 2019-20 income year. 1 BFA714 Australian Tax Law Semester 2, 2020 3. Rent Zeta Pty Ltd owns a small office building in West Hobart, which is let to a waste management operator. The rent for this building is $6,000 per month, payable one month in advance. On 30 June 2020, the tenant paid Zeta an extra 2 months' rent in advance. This amount of $12,000 may have to be refunded in the event that the tenant is precluded from using the premises for its intended purpose. 4. Royalties Zeta Pty Ltd received a gross royalty of $100,000 from its New Zealand subsidiary on 2 June 2020. New Zealand Non-Resident Withholding Tax (NRWT) of 15% was deducted from this payment, leaving a net receipt of $85,000. 5. Insurance On 1 March 2020, trading stock in transit was stolen. A claim for insurance was finalised on 30 June 2020 and Zeta Pty Ltd expects to receive $30,000 in respect of its insurance claim within two weeks. This amount has been taken up as a sundry debtor in the Statement of Financial Position. 6. Dividends Zeta Pty Ltd owns shares in BHP, a publicly listed company. On 15 June 2020, BHP declared a fully franked dividend, of which Zeta's share amounted to $40,000. This dividend was paid on 26 June 2020. 7. Trade debtors Trade debtors of $260,000 includes a provision for doubtful debts of $25,000. In the previous year this provision was $12,000. 8. Repairs Repairs and maintenance expenses include the items below. Item 1. Mezzanine floor replacement 2. Demolish and replace retaining wall 3. Replacing existing floor Cost $24,000 62,000 75,000 Notes: 1. Zeta Pty Ltd occupied a building that had been constructed in the early 1980s. Zeta acquired the building in 1997, and since then no significant repairs had been previously undertaken. The mezzanine floor was damaged, and it was recommended that it be demolished and replaced. 2. Upon inspection of the office premises, which Zeta owns, it was discovered that an external protective wall was partially collapsing. This required 85% of the wall to be demolished and rebuilt on its original foundations. The works included the building of two additional internal buttress walls to offer ongoing structural integrity, and the use of larger blocks of better quality sandstone. The original wall was not extended in height or length. 3. The concrete floor in one of Zeta's warehouses was cracking due to the use of inferior steel reinforcing when the floor was first constructed. The entire floor was demolished and replaced with the same thickness of concrete, but with better 2 BFA714 Australian Tax Law Semester 2, 2020 quality reinforcing. Zeta estimates that had it used the same reinforcing that was used originally, the repair would have cost only $50,000. 9. Prepayments Zeta prepaid the following amounts on 20 June 2020: . Item Insurance $50,000 - this amount was insurance for its office building in West Hobart and was for 12 months cover 10. Trading stock Opening stock for 2019/2020 was $135,000; closing stock was $138,000. Rent $30,000 - this amount was for the building it rents for its manufacturing operation and is paid 12 months in advance under its rental agreement. 11. Capital works The building referred to in Note 8 (above) had been acquired by Zeta for $3,200,000. A quantity surveyor's report estimated that the original construction cost had been $1,200,000. The construction had commenced on 30 August 1982. 12. Depreciation Accounting depreciation is as follows: Trademark Motor vehicle (sold 1/3/20) (note 1) Motor vehicle (purchased 1/3/20) (note 2) Office furniture Plant & equipment Total Effecti Method Original Purchases Opening Dep'n ve life Cost ($) (Disposals) WDV ($) (years) ($) ($) 40 CD CD 5 3 PC DV DV DV DV 20,000 18,000 500 30,000 (12,000) 18,000 2,707 135,000 60,000 60,000 3,729 123,500 24,700 20,000 6,000 Closing WDV ($) 179,500 37,908 17,500 56,271 245,000 Note: CD-use Commissioner's determination of effective life. 1. On 1 March 2020, one of the company's motor vehicles was sold for $12,000. This decline in value for this vehicle had been recorded using the Commissioner's determination of effective life. A loss of $3,293 on sale has been included in the Statement of Financial Performance. 0 98,800 14,000 186,571 3 BFA714 Australian Tax Law Semester 2, 2020 2. On 1 March 2020, a new car was purchased for the managing director at a cost of $60,000. The company estimates that the new car has an effective life of 5 years. Note: With the exception of the motor vehicle, no new depreciating assets were purchased during the 2019-20 income year. 13. Low value pool Zeta's low value pool opening balance for 2019/2020 was $46,000. Required Showing all your calculations and explaining each step in the process, calculate the taxable income for Zeta Pty Ltd for the year ending 30 June 2020. 4 Zeta Pty Ltd accounts for its income and expenditure on an accruals basis. A review of the financial records for the financial year ending 30 June 2020 reveals the following details. Statement of financial performance Income Sales revenue Interest Rent Royalties Insurance claim Cash dividend Total income Expenditure Operating costs Bad debt expense Repairs Insurance Rent Capital works Depreciation Total expenditure Net profit Note 2 Note 3 Note 4 Note 5 Note 6 Note 7 Note 8 Note 9 Note 11 Note 12 8,500,000 93,000 84,000 85,000 30,000 45,000 8,837,000 1,600,000 20,000 161,000 50,000 30,000 128,000 37,908 2,026,908 6,810,092 1. Aggregated annual turnover Zeta's aggregated annual turnover for 2017/2018 was $14 million and for 2018/2019 was $9 million. The company is not sure whether it qualifies as a small business entity, but if it does, it wants to use all of the concessions available. 2. Interest Zeta placed $1,000,000 on a twelve-month term deposit with the FED Bank on 1 November 2018. On maturity, the bank was instructed to transfer the interest amount of $60,000 to Zeta's trading account and reinvest the principal of $1,000,000 for a further twelve-month term deposit. The interest that accrued between 1 November 2019 and 30 June 2020 was $33,000. This was the only interest earned by the company for the 2019-20 income year. 1 BFA714 Australian Tax Law Semester 2, 2020 3. Rent Zeta Pty Ltd owns a small office building in West Hobart, which is let to a waste management operator. The rent for this building is $6,000 per month, payable one month in advance. On 30 June 2020, the tenant paid Zeta an extra 2 months' rent in advance. This amount of $12,000 may have to be refunded in the event that the tenant is precluded from using the premises for its intended purpose. 4. Royalties Zeta Pty Ltd received a gross royalty of $100,000 from its New Zealand subsidiary on 2 June 2020. New Zealand Non-Resident Withholding Tax (NRWT) of 15% was deducted from this payment, leaving a net receipt of $85,000. 5. Insurance On 1 March 2020, trading stock in transit was stolen. A claim for insurance was finalised on 30 June 2020 and Zeta Pty Ltd expects to receive $30,000 in respect of its insurance claim within two weeks. This amount has been taken up as a sundry debtor in the Statement of Financial Position. 6. Dividends Zeta Pty Ltd owns shares in BHP, a publicly listed company. On 15 June 2020, BHP declared a fully franked dividend, of which Zeta's share amounted to $40,000. This dividend was paid on 26 June 2020. 7. Trade debtors Trade debtors of $260,000 includes a provision for doubtful debts of $25,000. In the previous year this provision was $12,000. 8. Repairs Repairs and maintenance expenses include the items below. Item 1. Mezzanine floor replacement 2. Demolish and replace retaining wall 3. Replacing existing floor Cost $24,000 62,000 75,000 Notes: 1. Zeta Pty Ltd occupied a building that had been constructed in the early 1980s. Zeta acquired the building in 1997, and since then no significant repairs had been previously undertaken. The mezzanine floor was damaged, and it was recommended that it be demolished and replaced. 2. Upon inspection of the office premises, which Zeta owns, it was discovered that an external protective wall was partially collapsing. This required 85% of the wall to be demolished and rebuilt on its original foundations. The works included the building of two additional internal buttress walls to offer ongoing structural integrity, and the use of larger blocks of better quality sandstone. The original wall was not extended in height or length. 3. The concrete floor in one of Zeta's warehouses was cracking due to the use of inferior steel reinforcing when the floor was first constructed. The entire floor was demolished and replaced with the same thickness of concrete, but with better 2 BFA714 Australian Tax Law Semester 2, 2020 quality reinforcing. Zeta estimates that had it used the same reinforcing that was used originally, the repair would have cost only $50,000. 9. Prepayments Zeta prepaid the following amounts on 20 June 2020: . Item Insurance $50,000 - this amount was insurance for its office building in West Hobart and was for 12 months cover 10. Trading stock Opening stock for 2019/2020 was $135,000; closing stock was $138,000. Rent $30,000 - this amount was for the building it rents for its manufacturing operation and is paid 12 months in advance under its rental agreement. 11. Capital works The building referred to in Note 8 (above) had been acquired by Zeta for $3,200,000. A quantity surveyor's report estimated that the original construction cost had been $1,200,000. The construction had commenced on 30 August 1982. 12. Depreciation Accounting depreciation is as follows: Trademark Motor vehicle (sold 1/3/20) (note 1) Motor vehicle (purchased 1/3/20) (note 2) Office furniture Plant & equipment Total Effecti Method Original Purchases Opening Dep'n ve life Cost ($) (Disposals) WDV ($) (years) ($) ($) 40 CD CD 5 3 PC DV DV DV DV 20,000 18,000 500 30,000 (12,000) 18,000 2,707 135,000 60,000 60,000 3,729 123,500 24,700 20,000 6,000 Closing WDV ($) 179,500 37,908 17,500 56,271 245,000 Note: CD-use Commissioner's determination of effective life. 1. On 1 March 2020, one of the company's motor vehicles was sold for $12,000. This decline in value for this vehicle had been recorded using the Commissioner's determination of effective life. A loss of $3,293 on sale has been included in the Statement of Financial Performance. 0 98,800 14,000 186,571 3 BFA714 Australian Tax Law Semester 2, 2020 2. On 1 March 2020, a new car was purchased for the managing director at a cost of $60,000. The company estimates that the new car has an effective life of 5 years. Note: With the exception of the motor vehicle, no new depreciating assets were purchased during the 2019-20 income year. 13. Low value pool Zeta's low value pool opening balance for 2019/2020 was $46,000. Required Showing all your calculations and explaining each step in the process, calculate the taxable income for Zeta Pty Ltd for the year ending 30 June 2020. 4

Expert Answer:

Answer rating: 100% (QA)

ANS WER Yes Z eta P ty Ltd qualifies as a small business entity for the 2... View the full answer

Related Book For

Cornerstones of Financial and Managerial Accounting

ISBN: 978-1111879044

2nd edition

Authors: Rich, Jeff Jones, Dan Heitger, Maryanne Mowen, Don Hansen

Posted Date:

Students also viewed these accounting questions

-

Full Question 1: 1. Consider a consumer with the utility function u(x, x) = ln(x) + x and the budget constraint px + Px = m. Suppose good 1 represents coffee and good 2 represents everything else...

-

A review of the financial records for Rogers Inc. uncovered the following items: a. Collected accounts receivable b. Paid cash to purchase equipment c. Received cash from the issuance of bonds d....

-

A review of the financial records for Rogers, Inc., uncovered the following items: a. Received cash from the issuance of bonds b. Collected accounts receivable c. Paid cash to purchase equipment d....

-

On 13 May 2014, Ruben acquired 400 shares in Xantan Ltd at a cost of 1,800. On 17 July 2020, the company made a 1 for 8 bonus issue and (on the same day) Ruben sold his bonus shares for 7 each....

-

When calculating days inventory, the average inventory level is compared with the cost of sales. When calculating days debtors, the average accounts receivable balance is compared with the sales...

-

Samuel & Sons is a fixed-income specialty firm that offers advisory services to investment management companies. On 1 October 20X0, Steele Ferguson, a senior analyst at Samuel, is reviewing three...

-

Explain the working of constant volume combustion gas turbine.

-

At the beginning of June, Rhone Company had two jobs in process, Job 44 and Job 45, with the following accumulated cost information: During June, two more jobs (46 and 47) were started. The following...

-

Appendix V Current Job Information Smoke Damage Comm. Water Damage Other Total Total Res. Comm. Res. Comm. Res. Comm. Res. 2,542.00 120,000.00 394.00 270,000.00 Revenue Overhead cost allocated Direct...

-

Your client, Leona Ledford, was personally served with a summons and complaint on October 23 in the case of Masters v Ledford Her answer is due in 30 days. You will mail the answer to the court. What...

-

A large diffused surface is insulated at the bottom. It is subjected to solar radiation flux of 1200 W/m^2. The surface has alpha of 0.732 to solar irradiation while its alpha to room temperature...

-

Answer questions 1 -8 for a $250,000 home purchase using a conventional fixed rate mortgage from a private lender. Reminder: mortgage payments are monthly so use monthly compounding for all mortgage...

-

Emily owns a flower shop. Their monthly revenue is usually constant, except in the month of May, they made arrangements for a large wedding. In the month of February, there was a major snowstorm that...

-

What are the intricate mechanisms underlying microbial quorum sensing, and how do they influence microbial community dynamics?

-

ASB Corp. is considering the following two project proposals X and Y. The projected cash flows for project X and Y are as follows: End of Period: Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Project X...

-

What are the sex-specific differences in hormonal regulation of reproductive function, metabolism, and behavior, and how do these differences contribute to sexual dimorphism in health and disease?

-

Kroger Co. is one of the largest retail food companies in the United States as measured by total annual sales. The Kroger Co. operates supermarkets, convenience stores, and manufactures and processes...

-

Draw and label the E and Z isomers for each of the following compounds: 1. CH3CH2CH==CHCH3 2. 3. 4. CH,CH2C CHCH2CH Cl CH3CH2CH2CH2 CH CH2CCCH2CI CHCH3 CH3 HOCH CH CCC CH O-CH C(CH

-

Refer to the information for Fly High Airlines above. During the past year, the high and low use of three different resources for Fly High Airlines occurred in July and April. The resources are...

-

The controller for Summit Sales Inc. provides the following information on transactions that occurred during the year: a. Purchased supplies on credit, $28,400 b. Paid $24,600 cash toward the...

-

What are value- added activities? Value- added costs?

-

Give a comprehensive definition of auditing.

-

State the major changes which have occurred in auditing techniques during the last 160 years. Explain briefly how changes in technology have impacted on the changes in auditing techniques.

-

Under the provisions of the Companies Act 1985 an auditor's report must be attached to a company's financial statements. Is this true for all companies? Explain.

Study smarter with the SolutionInn App