Question: Simulation is helpful in learning vector time series. Define the matrices Use the command to generate 300 observations from the VAR(1) model [ z_{t}=C z_{t-1}+a_{t}

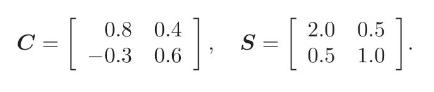

Simulation is helpful in learning vector time series. Define the matrices

Use the command

to generate 300 observations from the VAR(1) model

\[

z_{t}=C z_{t-1}+a_{t}

\]

where \(a_{t}\) are iid bivariate normal random variates with mean zero and \(\operatorname{Cov}\left(\boldsymbol{a}_{t}\right)=\boldsymbol{S}\).

- Plot the time series \(z_{t}\).

- Obtain the first five lags of sample CCMs of \(z_{t}\).

- Test \(H_{0}: ho_{1}=\cdots=ho_{10}=\mathbf{0}\) versus \(H_{a}: \boldsymbol{ho}_{i} eq \mathbf{0}\) for some \(i\), where \(i \in\{1, \ldots, 10\}\). Draw the conclusion using the \(5 \%\) significance level.

C = 0.8 0.4 -0.3 0.6 S = [ 2.0 0.5 0.5 1.0

Step by Step Solution

3.51 Rating (168 Votes )

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts