Tabulate and draw the investment opportunity set of the two risky funds. Use investment proportions for the

Question:

Tabulate and draw the investment opportunity set of the two risky funds. Use investment proportions for the stock fund of zero to 100% in increments of 20%.

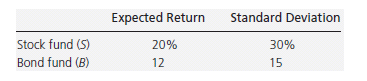

A pension fund manager is considering three mutual funds. The first is a stock fund, the second is a long-term government and corporate bond fund, and the third is a T-bill money market fund that yields a rate of 8%. The probability distribution of the risky funds is as follows:

The correlation between the fund returns is .10.

The word "distribution" has several meanings in the financial world, most of them pertaining to the payment of assets from a fund, account, or individual security to an investor or beneficiary. Retirement account distributions are among the most...

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Proportion in stock fund Proportion in bond fund Expected return Standard Deviation 000 10000 120...View the full answer

Answered By

Benard Ndini Mwendwa

I am a graduate from Kenya. I managed to score one of the highest levels in my BS. I have experience in academic writing since I have been working as a freelancer in most of my time. I am willing to help other students attain better grades in their academic portfolio. Thank you.

107+ Reviews

240+ Question Solved

Related Book For

Question Posted: