New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing

Auditing and Assurance Services 6th edition Timothy Louwers, Robert Ramsay, David Sinason, Jerry Straws - Solutions

Is there anything wrong with the bank statement? What are some ways to tell whether any of the amounts have been altered?

What is check kiting? How might auditors detect kiting?

How does a schedule of interbank transfers show improper cash transfer transactions?

Give some examples of control omissions that would make it easy to “think like a crook” and see opportunities for fraud.

What can an auditor find using net worth analysis? Expenditure analysis?

When auditing with “fraud awareness,” auditors should especially notice and follow up employee activities under which of these conditions? a. The company always estimates the inventory but never takes a complete physical count. b. The petty cash box is always locked in the desk of the

The best way to enact a broad fraud prevention program is to a. Install airtight control systems of checks and supervision. b. Name an “ethics officer” who is responsible for receiving and acting on fraud tips. c. Place dedicated hotline telephones on walls around the workplace with direct

A good fraud prevention program should address employees’ motivation to steal from the company. The best method for doing this is toa. Establish employee assistance programs.b. Require a fidelity bond on all employees.c. Require reconciliations of all accounts to be reviewed by a supervisor.d.

A code of ethics is an important element of a fraud prevention program. Which of the following would diminish the effectiveness of a company’s code of conduct? a. The establishment of a chief ethics officer. b. The establishment of a hotline for reporting unethical behavior. c. The violation of

Which of the following is least indicative of fraudulent activity? a. Numerous cash refunds have been made to different people at the same post office box address. b. Internal auditors cannot locate several credit memos to support reductions of customers’ balances. c. Bank reconciliation has no

Which of the following combinations is a good way to conceal employee fraud but an ineffective means of perpetrating management (financial reporting) fraud? a. Overstating sales revenue and overstating customer accounts receivable balances. b. Overstating sales revenue and overstating bad debt

Allison Everhart, an employee in accounts payable, believes she can run a fictitious invoice through the accounts payable system and collect the money. She knows payments are subject to an audit. Which account would be the best place to hide the fraud?a. Inventory.b. Wage expense.c. Consulting

Which of these arrangements of duties could most likely lead to an embezzlement or theft? a. The inventory warehouse manager has responsibility for making the physical inventory observation and reconciling discrepancies to the perpetual inventory records. b. The cashier prepared the bank deposit,

Which of the following would the auditor consider to be an incompatible operation if the cashier receives remittances? a. The cashier prepares the daily deposit. b. The cashier makes the daily deposit at a local bank. c. The cashier posts the receipts to the accounts receivable subsidiary ledger

Which of the following is an effective audit procedure that an auditor might use to detect kiting between intercompany banks? a. Review the composition of authenticated deposit slips. b. Review subsequent bank statements. c. Prepare a schedule of the bank transfers. d. Prepare a year-end bank

Immediately upon receipt of cash, a responsible employee should a. Record the amount in the cash receipts journal. b. Prepare a remittance listing. c. Update the subsidiary accounts receivable records. d. Prepare a deposit slip in triplicate.

Each morning the controller gets the prior day’s list of remittances, a copy of the payment report, and a copy of the deposit slip returned from the bank. When comparing these items, the controller would be able to determine that a. No checks were returned for insufficient funds. b. The cash

Upon receipt of customers’ checks in the mail room, a responsible employee should prepare a remittance list that is forwarded to the cashier. A copy of the list should be sent to the a. Internal auditor to investigate the list for unusual transactions. b. Treasurer to compare the list with the

Cash receipts from sales on account have been misappropriated. Which of the following acts would conceal this defalcation and be least likely to be detected by an auditor? a. Understating the sales journal. b. Overstating the accounts receivable control account. c. Overstating the accounts

Embezzlement is a type of fraud that involves a. An employee’s misappropriating an employer’s money or property not entrusted to him or her. b. A manager’s falsification of financial statements for the purpose of misleading investors and creditors. c. An employee’s mistaken representation

Which of the following control activities would best protect against the preparation of improper or inaccurate cash disbursements? a. All checks must be signed by an officer designated by the board of directors. b. All signed checks must be reviewed and compared with supporting documentation by the

During an audit of cash, the auditor is most concerned with the management assertion of a. Existence. b. Rights and obligations. c. Valuation or allocation. d. Occurrence.

In preparing for the audit of cash, the auditors perform analytical procedures concerning cash balances. Which of the following would be the best source of information for use in the estimate of cash? a. Prior- years’ balances. b. Management inquiry. c. Cash budgets. d. Aged accounts receivable

Which of the following control activities could prevent a paid disbursement voucher from being presented for payment a second time? a. Vouchers should be prepared by individuals who are responsible for signing disbursement checks. b. Disbursement vouchers should be approved by at least two

Fraud risk factors are events or conditions that indicate which of the following: a. An opportunity to carry out a fraud. b. An attitude or rationalization that justifies a fraudulent action. c. An incentive or pressure to perpetrate fraud. d. All of these are correct.

If the auditor believes that a misstatement is or might be intentional and the effect on the financial statements could be material or cannot be readily determined, the auditor should do which of the following? a. Inquire of management as to the possibility of fraud. b. Discuss with the audit

In what way can audit procedures be modified to address assessed fraud risks?a. Obtain more reliable information.b. Perform procedures close to year- end.c. Apply computer- assisted techniques to all items.d. All of these are valid modifications.

Incorporating elements of unpredictability in the selection of audit procedures to be per-formed by auditors include all of the following except a. Varying the timing of the audit procedures. b. Selecting items for testing that have lower amounts or are otherwise outside customary selection

Fraud risk factors are events or conditions that indicate I. An incentive or pressure to perpetrate fraud. II. An opportunity to carry out the fraud. III. An attitude or rationalization that justifies the fraudulent action. Which of the following statements is true? a. I is a fraud risk factor. b.

The Runge Controls Corporation manufactures and markets electrical control systems: temperature controls, machine controls, burglar alarms, and the like. The company acquires electrical and semiconductor parts from outside vendors and assembles systems in its own plant. The company incurs other

Taylor, a CPA, has been engaged to audit the financial statements of University Books, Incorporated. University Books maintains a large cash fund exclusively for the purpose of buying used books from students for cash. The cash fund is active all year because the nearby university offers a large

You are the in charge auditor examining the financial statements of the Gutzler Company for the year ended December 31. During late October, with the help of Gutzler’s controller, you completed an internal control questionnaire and prepared the appropriate memoranda describing Gutzler’s

You are the auditor for Konerko’s Office supply store, which is opening for business next week. The store owner has established all the controls you have recommended for ensuring that sales are recorded properly and cash is accounted for. The owner has heard from other small business owners that

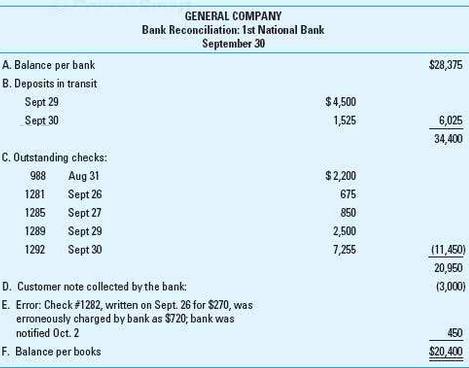

Auditors typically will find the items lettered A–F in a client-prepared bank reconciliation.Required:Assume these facts: On October 11, the auditor received a cutoff bank statement dated October 7. The September 30 deposit in transit; the outstanding checks 1281, 1285, 1289, and 1292; and the

You can use the computer- based Electronic Audit Documentation on the textbook’s website to prepare the proof of cash required in this problem. The auditors of Steffey Ltd., decided to study the cash receipts and disbursements for the month of July of the current year under audit. They obtained

You can use the computer based Electronic Workpapers on the textbook website to prepare the schedule of interbank transfers required in this problem. EverReady Corporation is in the home building and repair business. Construction business has been in a slump and the company has experienced

Suppose you are auditing cash disbursements and discover several payments to a company you are unfamiliar with and cannot find information about this company on the Internet or in the local telephone directory. The invoices from this company have numbers very close to each other in the sequence,

Consider the following scenario: Adam worked for the local hardware store as an outside sales representative. His job was to visit local companies and contractors in an attempt to identify their needs for tools and materials and provide a bid to supply those items. When a local contractor accepted

The Perfect Crime? Consider the following story of an actual embezzlement. This was the ingenious embezzler’s scheme: (a) He hired a print shop to print a private stock of Ajax Company checks in the company’s numerical sequence. (b) In his job as an accounts payable clerk at Ajax, he

The following are some “suspicions”; you have been requested to select some effective extended procedures designed to confirm or deny the suspicions. Required: Write the suggested procedures for each case in definite terms so another person can know what to do. a. The custodian of the petty

Expenditure analysis is used when fraud has been discovered or strongly suspected and the information to calculate a suspect’s income and expenditures can be obtained (. g., asset and liability records, bank accounts). Expenditure analysis consists of establishing the suspect’s known

You can use the computer- based Electronic Workpapers on the textbook website to prepare the net worth analysis required in this problem. Net worth analysis is performed when fraud has been discovered or is strongly suspected and the information to calculate a suspect€™s net worth can be

Mini- Case: Cash Confirmations. Refer to the mini- case “Something Went Sour at Parma-lat” on page C20 and respond to question 1.On page C20There was much confusion when Italian dairy food giant Parmalat defaulted on a $ 187 million bond payment in mid- November 2002. Default on a bond payment

You can use the computer- based Electronic Workpapers on the textbook website to prepare the bank reconciliation solution. Caulco Inc. is the audit client. The February bank statement is shown in Exhibit 6.6 in the text. You have obtained the client- prepared bank reconciliation as of February 28

This case is designed in a manner similar to the cases in the chapter. You can assume you have received a message from an informant regarding the following case. Your assignment is to write the “audit approach” portion of the case.a. Write a brief explanation of desirable controls, missing

What are some red flags that may indicate a cover- up or concealment of a fraud?

What is a cutoff bank statement? How do auditors use it?

How can a proof of cash reveal unrecorded cash deposit and cash payment transactions?

In Case 6.1, if the petty cash custodian were replaced and the frequency of fund reimbursement decreased from every two days to every four days, what might you suspect?

What is the difference between a normal procedure and an extended procedure?

What is the basic sequence of activities and accounting in a revenue and collection cycle?

What computer- based files might auditors examine to find evidence of unrecorded sales? Of inadequate credit checks? Of incorrect product unit prices?

Suppose that you selected a sample of customers’ accounts receivable and wanted to find supporting evidence for the entries in the accounts. Where would you go to vouch the debit entries? What would you expect to find? Where would you go to vouch the credit entries? What would you expect to find?

What account balances are included in a revenue and collection cycle?

What specific control procedures (in addition to separation of duties and responsibilities) should be in place and operating in internal controls governing revenue recognition and cash accounting?

What is a walkthrough of a sales transaction? How can the walkthrough work complement the use of an internal control questionnaire?

What assertions are made about classes of transactions and events in the revenue and collection cycle?

What is dual- direction test of controls sampling?

Which audit procedures are usually the most useful for auditing the existence assertion?

What analytical procedures might be informative regarding the existence assertion?

What are some justifications for not using confirmations of accounts receivable on a particular audit?

What special care should be taken with regard to examining the sources of accounts receivable confirmation responses?

What alternative procedures should be applied to accounts that do not return confirmations?

What procedures should be performed to determine the adequacy of the allowance for doubtful accounts?

What are the goals of dual- direction testing regarding an audit of the accounts receivable and cash collection system?

In the case of Bill Often, Bill Early, what information might have been obtained from inquiries?From tests of controls?From observations?From confirmations?

Revenues are normally considered to have been earned whena. All possibility of return has expired.b. The company has substantially accomplished what it must to be entitled to the benefits. c. The cash is collected.d. Goods have been shipped.

Sales are normally recorded on the date of the a. Customer purchase order. b. Bill of lading. c. Sales invoice. d. Payment check.

When auditing the revenue and collection cycle, auditors normally select balances to con-firm from the a. Sales journal. b. Accounts receivable listing. c. General ledger. d. Cash receipts listing.

Which of the following accounts is not normally part of the revenue and collection cycle? a. Sales b. Accounts Receivable. c. Cash. d. Purchases Returns and Allowances

The control procedure “credit sales approved by credit department” is directed toward which transaction assertion? a. Occurrence b. Completeness c. Accuracy d. Cutoff

Which of the following would be the best protection for a company that wishes to prevent the “lapping” of trade accounts receivable? a. Separate duties so that the bookkeeper in charge of the general ledger has no access to incoming mail. b. Separate duties so that no employee has access to

Which of the following internal control activities will most likely prevent the concealment of a cash shortage by improperly writing off a trade account receivable? a. Write- offs must be approved by a responsible officer after review of credit department recommendations and supporting evidence. b.

Auditors sometimes use comparisons of ratios as audit evidence. An unexplained decrease in the ratio of gross profit to sales may suggest which of the following possibilities? a. Unrecorded purchases. b. Unrecorded sales. c. Merchandise purchases being charged to selling and general expense. d.

An audit team is auditing sales transactions. One step is to vouch a sample of debit entries from the accounts receivable subsidiary ledger back to the supporting sales invoices. The purpose of this audit procedure is to establish that a. Sales invoices represent bona fide sales. b. All sales have

Based on this information, the auditor is most likely concerned about a. Unrecorded costs. b. Improper credit approvals. c. Improper sales cutoff. d. Fictitious sales.

Based on this information, the auditor interviewed the sales manager, who stated that the increase in sales without a corresponding increase in cost of goods sold was due to a price increase enacted by the company during the year. How would the auditor test the sales man-ager’s representation? a.

To conceal a theft involving receivables, a dishonest bookkeeper might charge which of the following accounts? a. Miscellaneous income. b. Petty cash. c. Miscellaneous expense. d. Sales returns.

Which of the following responses to an accounts receivable confirmation at December 31 would cause an audit team the most concern? a. “ This amount was paid on December 30.” b. “ We received this shipment on January 2.” c. “ These goods were returned for credit on November 15.” d. “

A client has a separate sales group for its largest “preferred” customers, a select group of customers who normally make purchases in excess of $ 250,000 and often have accounts receivable balances in excess of $ 1 million. Which of the following audit procedures would the auditor most likely

Audit documentation often includes a client- prepared, aged trial balance of accounts receivable as of the balance sheet date. The audit team uses this aging primarily to a. Evaluate internal control over credit sales. b. Test the accuracy of recorded charge sales. c. Estimate credit losses. d.

Which of the following might be detected by auditors’ cutoff review and examination of sales journal entries for several days prior to the balance sheet date? a. Lapping year- end accounts receivable. b. Inflating sales for the year. c. Kiting bank balances. d. Misappropriating merchandise.

Confirmation of individual accounts receivable balances directly with debtors will, of itself, normally provide the strongest evidence concerning the a. Collectability of the balances confirmed. b. Ownership of the balances confirmed. c. Existence of the balances confirmed. d. Internal control

Which of the following is the best reason for prenumbering in numerical sequence docu-ments such as sales orders, shipping documents, and sales invoices? a. Enables company personnel to determine the accuracy of each document. b. Enables personnel to determine the proper period recording of sales

When a sample of customer accounts receivable is selected for vouching debits, auditors will vouch them toa. Sales invoices with shipping documents and customer sales invoices.b. Records of accounts receivable write- offs.c. Cash remittance lists and bank deposit slips.d. Credit files and reports.

In the audit of accounts receivable, the most important emphasis should be on the a. Completeness assertion. b. Existence assertion. c. Rights and obligations assertion. d. Presentation and disclosure assertion.

When accounts receivable are confirmed at an interim date, auditors need not be concerned witha. Obtaining a summary of receivables transactions from the interim date to the year- end date.b. Obtaining a year- end trial balance of receivables, comparing it to the interim trial balance, and

The negative request form of accounts receivable confirmation is useful particularly whenthe

When an audit team traces a sample of shipping documents to the related sales invoice copies, they are trying to find relevant evidence that a. Shipments to customers were invoiced. b. Shipments to customers were recorded as sales. c. Recorded sales were shipped. d. Invoiced sales were shipped.

Write- offs of doubtful accounts should be approved by a. The salesperson. b. The credit manager. c. The treasurer. d. The cashier.

When an audit team does not receive a response on a positive accounts receivable confirmation, auditors should do all of the following except a. Send a second request. b. Do nothing for immaterial balances. c. Examine shipping documents. d. Examine client correspondence files.

Cash receipts from sales on account have been misappropriated. Which of the following acts would conceal this defalcation and be least likely to be detected by an auditor? a. Understating the sales journal. b. Overstating the accounts receivable control account. c. Overstating the accounts

Which of the following internal control activities most likely would deter lapping of collections from customers? a. Independent internal verification of dates of entry in the cash receipts journal with dates of daily cash summaries. b. Authorization of write- offs of uncollectable accounts by a

The financial records of the Movitz Company show that R. Dennis owes $ 4,100 on an account receivable. An independent audit is being carried out, and the auditors send apositive confirmation to R. Dennis. What is the most likely reason as to why a positive confirmation rather than a negative

An audit client sells 15 to 20 units of product annually. A large portion of the annual sales occur in the last month of the fiscal year. Annual sales have not materially changed over the past five years. Which of the following approaches would be most effective concerning the timing of audit

An auditor is required to confirm accounts receivable if the accounts receivable balances are a. Older than the prior year. b. Material to the financial statements. c. Smaller than expected. d. Subject to valuation estimates.

During the confirmation of accounts receivable, an auditor receives a confirmation via the client’s fax machine. Which of the following actions should the auditor take? a. Not accept the confirmation and select another customer’s balance to confirm. b. Not accept the confirmation and treat it

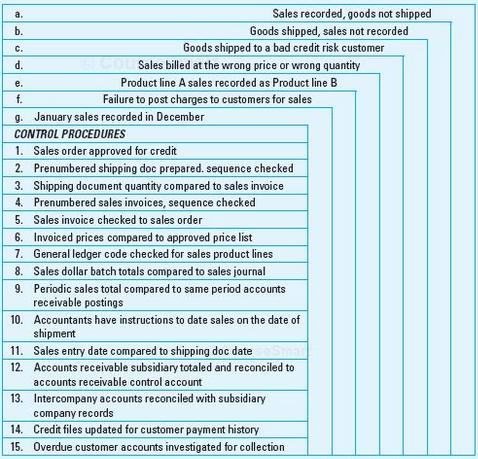

Control Objectives and Procedures Associations. Exhibit 7.60.1 contains an arrangement of examples of transaction errors (lettered a– g) and a set of client control procedures and devices (numbered 1– 15). Make a copy of the exhibit page and complete the following requirements.Exhibit

Exhibit 7.60.1 contains an arrangement of examples of transaction errors (lettered a– g) and a set of client control procedures and devices (numbered 1– 15).Required:For each error/ control objective, identify the assertion about classes of transactions and events most benefited by

Exhibit 7.60.1 contains an arrangement of examples of transaction errors (lettered a– g) and a set of client control procedures and devices (numbered 1– 15).Exhibit 7.60.1Required: For each client control procedure numbered 1– 15, write a test of controls that could produce evidence on

Showing 4700 - 4800

of 10291

First

41

42

43

44

45

46

47

48

49

50

51

52

53

54

55

Last

Step by Step Answers

-1.png)

-2.png)

.png)

.png)

.png)

.png)

.png)