New Semester

Started

Get

50% OFF

Study Help!

--h --m --s

Claim Now

Question Answers

Textbooks

Find textbooks, questions and answers

Oops, something went wrong!

Change your search query and then try again

S

Books

FREE

Study Help

Expert Questions

Accounting

General Management

Mathematics

Finance

Organizational Behaviour

Law

Physics

Operating System

Management Leadership

Sociology

Programming

Marketing

Database

Computer Network

Economics

Textbooks Solutions

Accounting

Managerial Accounting

Management Leadership

Cost Accounting

Statistics

Business Law

Corporate Finance

Finance

Economics

Auditing

Tutors

Online Tutors

Find a Tutor

Hire a Tutor

Become a Tutor

AI Tutor

AI Study Planner

NEW

Sell Books

Search

Search

Sign In

Register

study help

business

auditing

Auditing and Assurance Services 6th edition Timothy Louwers, Robert Ramsay, David Sinason, Jerry Straws - Solutions

An auditor is examining a nonpublic company’s inventory procurement system and has decided to perform tests of controls. Under which of the following conditions do GAAS require tests of controls be performed by an auditor? a. Significant weaknesses were found in the company’s internal control.

Which of the following management assertions is an auditor most likely testing if the audit objective states that all inventory on hand is reflected in the ending inventory balance? a. The entity has rights to the inventory. b. Inventory is properly valued. c. Inventory is properly presented in the

A portion of a client’s inventory is in public warehouses. Evidence of the existence of this merchandise can most efficiently be acquired through which of the following methods?a. Observation.b. Confirmation.c. Calculation.d. Inspection.

The purpose of tracing a sample of inventory tags to a client’s computerized listing of inventory items is to determine whether the inventory itemsa. Represented by tags were included on the listing.b. Included on the listing were properly counted.c. Represented by tags were reduced to the lower

Internal Control Questionnaire Items: Possible Error or Fraud Due to Weakness . Refer to the internal control questionnaire for the production cycle and assume that the answer to each question is “no.” Prepare a table matching questions to errors or frauds that could occur because of the

Tests of Controls Related to Controls and Assertions. Each of the following tests of controls could be performed during the audit of the controls in the production cycle. Required: For each procedure, identify (a) The internal control activity (strength) being tested and (b) The assertion(s) being

The diagram in Exhibit 9.47.1 describes several cost accounting tests of controls. It shows the direction of the tests, leading from samples of cost accounting analyses, management reports, and the general ledger to blank squares.Required:For each blank square in Exhibit 9.47.1, write a cost

Inventory Count Observation: Planning and Substantive Procedures. Sammy Smith is the partner in charge of the audit of Blue Distributing Corporation, a wholesaler that owns one warehouse containing 80 percent of its inventory. Smith is reviewing the audit documentation that was prepared to support

Your client took a complete physical inventory count under your observation as of December 15 and adjusted the inventory control account (perpetual inventory method) to agree with the physical inventory count. After considering the count adjustments as of December 15 and after reviewing the

When tracing using the cutoff information from the December 31 inventory count of Thermo- Tempur Mattresses, you note the following information:The purchases list shows that the following items were recorded in December.The documentation indicates that the last receiving report included in the

ACE Corporation does not conduct a complete annual physical count of purchased parts and supplies in its principal warehouse but uses statistical sampling to estimate the year- end inventory. ACE maintains a perpetual inventory record of parts and supplies. Management believes that statistical

You are conducting an audit of the financial statements of a wholesale cosmetics distributor with an inventory consisting of thousands of individual items. The distributor keeps its inventory in its own distribution center and in two public warehouses. A perpetual inventory computer database is

CAATs Application: Inventory. Your client, Boos & Becker Inc., is a medium- size manufacturer of products for the leisure- time activities market (camping equipment, scuba gear, bows and arrows, and the like). During the past year, a computer system was installed, and inventory records of finished

During the audit of Mason Company Inc., for the calendar year 2014, you noted that the company produces aluminum cans at the rate of about 40 million units annually. On the plant tour, you noticed a large stockpile of raw aluminum in storage. Your inventory observation and pricing procedures showed

You have been assigned to trace the results of the observation of Brightware China’s physical inventory count to its pricing and compilation. You note the following conditions.1. The last inventory tag documented by Mark Hulse, the auditor who observed the inventory, was 1732, but you notice a

You are auditing Martha's Prison Clothes Inc., as of December 31, 2014. The inventory for orange jumpsuits shows 1,263 suits at $ 782 for a total of $ 987,666. When you look at the invoices for the jumpsuits, you see the following:Required: a. Determine the adjusting entry, if any, for the cost of

Mattel Inc., a manufacturer of toys, failed to write off obsolete inventory, thereby overstating inventory and improperly deferred tooling costs, both of which understated cost of goods sold and overstated income.“ Excess” inventory was identified by comparing types of toys ( wheels, general

No Defense for These Charges. Follow the instructions preceding Problem 9.57. Write the audit approach section following the case in the chapter.SueCan Corporation manufactured electronic and other equipment for private customers and government defense contracts. It deferred costs under the heading

Follow the instructions preceding Problem 9.57. Write the audit approach section following the cases in the chapter.The following is an excerpt from an article, “Memory Chip Trader Gets 14 Years for Bank Fraud,” The Straits Times (Singapore), February 13, 2009:Through most of the 1990s,

For each of the following independent events, indicate the (1) effect of the error or fraud on the financial statements and (2) what auditing procedures could have detected the misstatement resulting from error or fraud.a. The physical inventory count of J. Payne Enterprises, which has a December

What functions are normally associated with the production cycle?

When auditors want to use a client’s sales forecast for general familiarity with the production cycle or for evaluation of slow- moving inventory, what kind of procedures should be performed with respect to the forecast?

If the actual sales for the year are substantially lower than the sales forecasted at the beginning of the year, what potential valuation problems could arise in the production cycle accounts?

What features of the cost accounting system would be expected to prevent the omission of recording materials used in production?

How does the production order record provide a control over the quantity of materials used in production?

Why is it important for auditors to obtain control information over inventory count sheets or tickets?

Why is it important to obtain shipping and receiving cutoff information during the inventory observation?

What procedures do auditors employ to audit inventory when the physical inventory count is taken on a cycle basis or on a statistical plan but never a complete count on a single date?

What steps should auditors take if the client has multiple locations being counted?

What is an inventory roll forward? What roll- forward tests should be performed?

What documents would auditors inspect in the audit of investment securities and what information would they obtain from these documents?

Describe the activities and documentation of a controlled count of the client’s investment securities.

What is a compensating control? Give some examples for finance and investment cycle accounts.

What are some of the specific relevant aspects of management’s control over the estimation process? What are some inquiries auditors can make?

What documentation should an auditor inspect when a client has paid off a bank note? How could an employee defraud the company if the bank note has no indication of being paid?

What are some of the important assertions found in stockholders’ equity account balances and disclosures?

What are some of the important assertions found in the long- term liability accounts?

How can confirmations be used in auditing (a) Stockholder capital accounts and (b) Notes and bonds payable?

Define and give five examples of off- balance- sheet information. Why should auditors be concerned with such items?

If a company does not monitor notes payable for due dates and interest payment dates in relation to financial statement dates, what misstatements can appear in the financial statements?

What are some of the important assertions found in investment accounts?

What are some of the typical areas of concern to auditors involving investment accounts?

What unfortunate lesson did the auditors learn from the situation in the Unregistered Sale of Securities case? What should auditors do when a violation of U. S. securities laws is suspected?

How could auditors have discovered the off- balance- sheet financing described in the Off- Balance- Sheet Inventory Financing case?

How should an audit team assess the reasonableness of a film studio’s estimate of film revenues? (Refer to the No Treasure in This Treasure Planet case.)

Which of the following approaches is most suitable for auditing the finance and investment cycle? a. Perform extensive tests of controls and limit substantive procedures to analytical procedures. b. Ignore internal controls and perform extensive substantive procedures. c. Gain an understanding of

Loan covenants are used for which of the following reasons? a. To protect the lender from the borrower’s substantially weakening of the latter’s financial position. b. To protect the borrower from the lender’s calling the loan early. c. To protect the auditors from false information by the

A related party is a person or entity that a. Has a family tie to a management member. b. Does business with the company. c. Can exert significant influence over or be influenced by the company. d. Is a member of the company’s management team or board of directors.

Jones was engaged to examine the financial statements of Gamma Corporation for the year ended June 30. Having completed an examination of the investment securities, which of the following is the best method of verifying the accuracy of recorded dividend income? a. Tracing recorded dividend income

When the client holds a large amount of negotiable securities, auditors need to plan to guard against a. Unauthorized negotiation of the securities before they are counted. b. Unrecorded sales of securities after they are counted. c. Substitution of securities already counted for other securities

In connection with the audit of an issue of long- term bonds payable, the audit team should a. Determine whether bondholders are persons other than owners, directors, or officers of the company issuing the bond. b. Calculate the effective interest rate to see whether it is substantially the same as

Which of the following is the most important audit consideration when examining the stockholders’ equity section of a client’s balance sheet? a. Changes in the capital stock account are verified by an independent stock transfer agent. b. Stock dividends and stock splits during the year under

If the auditors discover that the carrying amount of a client’s investments is overstated because of a loss in value that is other than a temporary decline in market value, they should insist thata. The approximate market value of the investments be shown in parentheses on the face of the balance

The primary reason for preparing a reconciliation between interest- bearing obligations outstanding during the year and interest expense in the financial statements is toa. Evaluate internal control over securities.b. Determine the validity of prepaid interest expense.c. Ascertain the

The auditors should insist that a representative of the client be present during the inspection and count of securities to a. Lend authority to the auditors’ directives. b. Detect forged securities. c. Coordinate the return of all securities to proper locations. d. Acknowledge the receipt of

When independent stock transfer agents are not employed and the corporation issues its own stock and maintains stock records, canceled stock certificates should a. Be defaced to prevent reissuance and attached to their corresponding stubs. b. Not be defaced but be segregated from other stock

When a client company does not maintain its own capital stock records, the auditors should obtain written confirmation from the transfer agent and registrar concerninga. Restrictions on the payment of dividends.b. The number of shares issued and outstanding.c. Guarantees of preferred stock

All corporate capital stock transactions should ultimately be traced to the a. Minutes of the meetings of the board of directors. b. Cash receipts journal. c. Cash disbursements journal. d. Numbered stock certificates.

An audit plan for the examination of the retained earnings account should include a step that requires verification of the (choose two steps) a. Market value used to charge retained earnings to account for a 2- for- 1 stock split. b. Approval of the adjustment to the beginning balance as a result

When an entity uses a trust company as custodian of its marketable securities, the possibility of concealing fraud most likely would be reduced if the a. Trust company has no direct contact with the entity employees responsible for maintaining investment accounting records. b. Securities are

An audit team would most likely verify the interest earned on bond investments bya. Vouching the receipt and deposit of interest checks.b. Confirming the bond interest rate with the issuer of the bonds.c. Re-computing the interest earned on the basis of face amount, interest rate, and period

A client has a large and active investment portfolio that is kept in a bank safe deposit box. If the auditors are unable to count securities at the balance sheet date, they most likely will a. Request the bank to confirm to the auditors the contents of the safe deposit box at the balance- sheet

An audit team testing long- term investments would ordinarily use analytical procedures to ascertain the reasonableness of the a. Existence of unrealized gains or losses. b. Completeness of recorded investment income. c. Classification as available- for- sale or trading securities. d. Valuation of

In auditing for unrecorded long- term bonds payable, an audit team most likely will a. Perform analytical procedures on the bond premium and discount accounts. b. Examine documentation of assets purchased with bond proceeds for liens. c. Compare interest expense with the bond payable amount for

An audit plan to examine long- term debt most likely would include steps that require a. Comparing the carrying amount of held- to- maturity securities with their year- end market values. b. Correlating interest expense recorded for the period with outstanding debt. c. Verifying the existence of

Which of the following questions would auditors most likely include on an internal control questionnaire for notes payable? a. Are assets that collateralize notes payable critically needed for the entity’s continued existence? b. Are two or more authorized signatures required on checks that repay

An audit team’s purpose in reviewing the documentation concerning the renewal of a note payable shortly after the balance- sheet date most likely is to obtain evidence concerning management’s assertions abouta. Existence.b. Valuation.c. Completeness.d. Classification.

Which of the following audit procedures would not likely be performed for audits of investments? a. Read board of directors’ minutes for authorization of investment strategies. b. Confirm investments with registrar. c. Confirm investments with broker or trustee. d. Compare valuation to published

Which of the following audit procedures would not likely be performed for audits of share-holders’ equity? a. Read board of directors’ minutes for authorization of equity transactions. b. Confirm outstanding common and preferred stock with stock registrar. c. Compare valuation of stock to

ABC Company has 100 shares of IBM stock that it holds as an investment. The stock was purchased three years ago and has been in the client’s safe deposit box along with other investment securities. During an inspection of securities held by the client, the auditor noted the 100 shares of IBM

Cassandra Corporation, a manufacturing company, periodically invests large sums in marketable equity securities. The investment committee of the board of directors established the investment policy. The treasurer is responsible for carrying out the investment committee’s directives. All

You are engaged in the audit of the financial statements of Bass Corporation for the year ended December 31 and you are about to begin an audit of the investment securities. Bass’s records indicate that the company owns various bearer bonds as well as 25 percent of the outstanding common stock

Union Pacific Corp. opened its new 19- story, $ 260 million headquarters in Omaha, Nebraska. The railroad operator is the owner of the city’s largest building, the Union Pacific Center. Under an initial operating lease, Union Pacific guaranteed 89.9 percent of all construction costs through the

You are in charge of the audit of the financial statements of Demot Corporation for the year ended December 31. The corporation has a policy of investing its surplus funds in marketable securities. Its stock and bond certificates are kept in a safe deposit box in a local bank. Only the president

In the audit of investment securities, auditors develop specific audit assertions related to the investments. They then design specific substantive procedures to obtain evidence about each of these assertions. Following is a selection of investment securities assertions: 1. Investments are properly

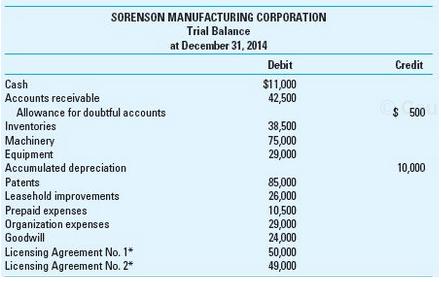

Sorenson Manufacturing Corporation was incorporated on January 3, 2013. The corporation’s financial statements for its first year’s operations were not examined by a CPA. You have been engaged to audit the financial statements for the year ended December 31, 2014, and your work is

A loan covenant is a condition requiring the borrower to comply with the terms of a loan agreement. If the borrower does not act in accordance with the covenants, the loan can be considered in default and the lender has the right to demand payment (usually in full). Required: a. Why do banks add

You have been engaged to audit the financial state-ments of Broadwall Corporation for the year ended December 31, 2014. During the year, Broadwall obtained a long- term loan from a local bank pursuant to a financing agreement, which provided the following: 1. The loan is to be secured by the

The following covenants are extracted from the indenture of a bond issue. The indenture provides that failure to comply with its terms in any respect automatically advances the due date of the loan to the date of noncompliance (the stated date is 20 years hence). Give any audit steps or reporting

Common Stock and Treasury Stock: Substantive Audit Procedures. You are the continuing auditor of Sussex Inc. and are beginning the audit of the common stock and treasury stock accounts. You have decided to design substantive procedures with reliance on internal controls. Sussex has no- par, no-

You are a CPA engaged in an audit of the financial statements of Pate Corporation for the year ended December 31. The financial statements and records of Pate Corporation have not been audited by a CPA in prior years. The stockholders’ equity section of Pate Corporation’s balance sheet at

You have been engaged to audit the financial statements of Hardy Hardware Distributors Inc., as of December 31. In your review of the corporate nonfinancial records, you have found that Hardy Hardware owns 15 percent of the outstanding voting common stock of Hardy Products Corporation. Upon

Write the audit approach section like the cases in the chapter. Hide the Loss under the Goodwill Gulwest Industries, a public company, decided to discontinue its unprofitable line of business of manufacturing sporting ammunition. Gulwest had capitalized the startup cost of the business, and with

Follow the instructions in the preceding the case in 10.59. Write the audit approach section like the cases in the chapter. In Plane View Whiz Corporation owned 160,000 shares of Wing Company stock, carried on the books as an investment in the amount of $ 6,250,000. Whiz bought a used airplane from

Follow the instructions in the preceding the case 10.59. Write the audit approach section like the cases in the chapter. Rogue Trader In February 1989, 22- year- old Nicholas Leeson joined Barings Investment Bank. In 1993, he began trading on behalf of the Barings group as a “proprietary

Who is normally responsible for the authorization of investment activities? Why is the authorization normally performed at this level?

What constitutes the authorization for notes payable? What documentary evidence could auditors examine to confirm this authorization?

What information about capital stock could be confirmed with outside parties? How could the auditors corroborate this information?

How can confirmations be used in auditing investments in stocks?

Identify four primary periods in an audit examination and the tasks and activities that occur in each.

How are analytical procedures used near the end of the audit?

What are the responsibilities of (a) Client management, (b) Auditors, and (c) The client’s attorneys with respect to obtaining evidence regarding litigation, claims, and assessments?

What is the typical content of attorney letters?

In addition to obtaining responses to attorney letters, what other procedures can be used to gather audit evidence regarding litigation, claims, and assessments?

What are the major categories of information contained in written representations?

If the entity is subject to the requirements of AS 5, what written representations should auditors obtain from the client with respect to internal control over financial reporting?

What factors may indicate that substantial doubt exists about the client’s ability to continue as a going concern?

What actions should auditors take if evidence suggests that substantial doubt exists about the client’s ability to continue as a going concern?

What is an uncorrected misstatement? What is the auditors’ responsibility for communicating misstatements detected during the audit?

Describe the audit documentation review process in a public accounting firm

Showing 4900 - 5000

of 10291

First

43

44

45

46

47

48

49

50

51

52

53

54

55

56

57

Last

Step by Step Answers

.png)

.png)

-1.png)

-2.png)

.png)

.png)